STERIS’s stock price has taken a beating over the past six months, shedding 20.4% of its value and falling to $202.39 per share. This might have investors contemplating their next move.

Is now the time to buy STERIS, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is STERIS Not Exciting?

Despite the more favorable entry price, we’re sitting this one out for now. Here are three reasons we avoid STE, plus one stock we’d rather own.

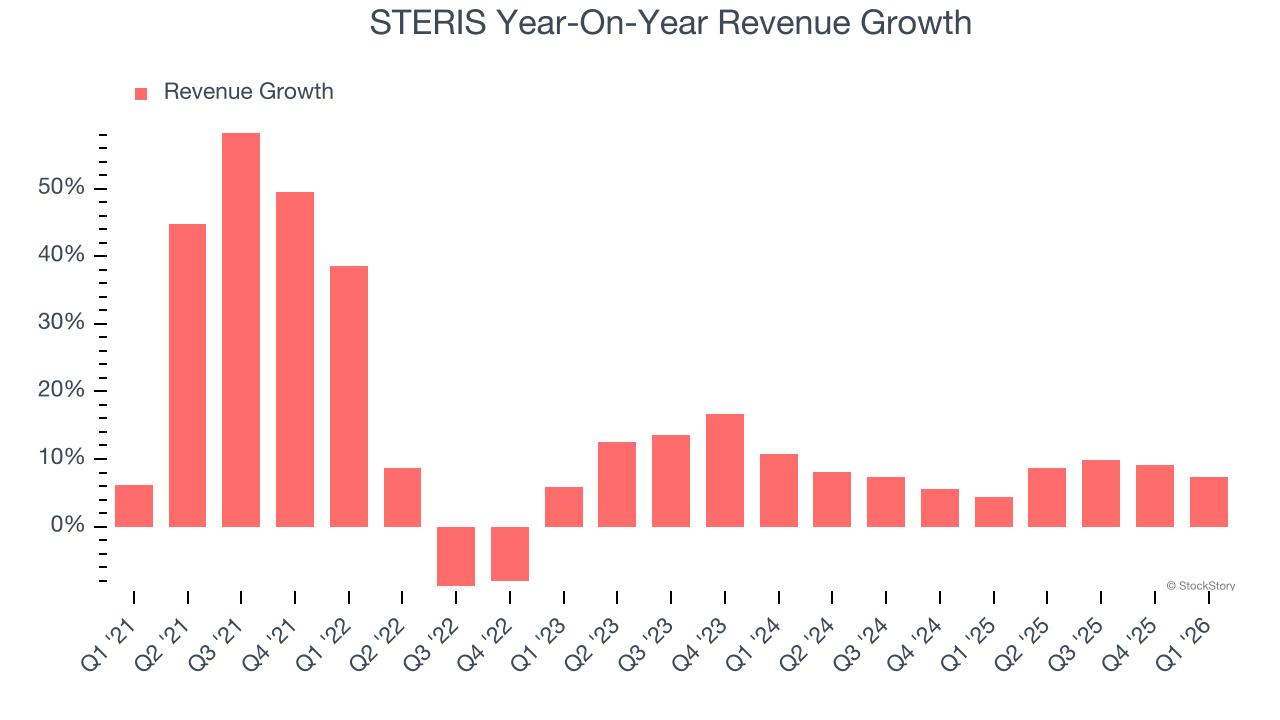

1. Lackluster Revenue Growth

We at StockStory place the most emphasis on long-term growth, but within healthcare, a stretched historical view may miss recent innovations or disruptive industry trends. STERIS’s recent performance shows its demand has slowed as its annualized revenue growth of 7.5% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

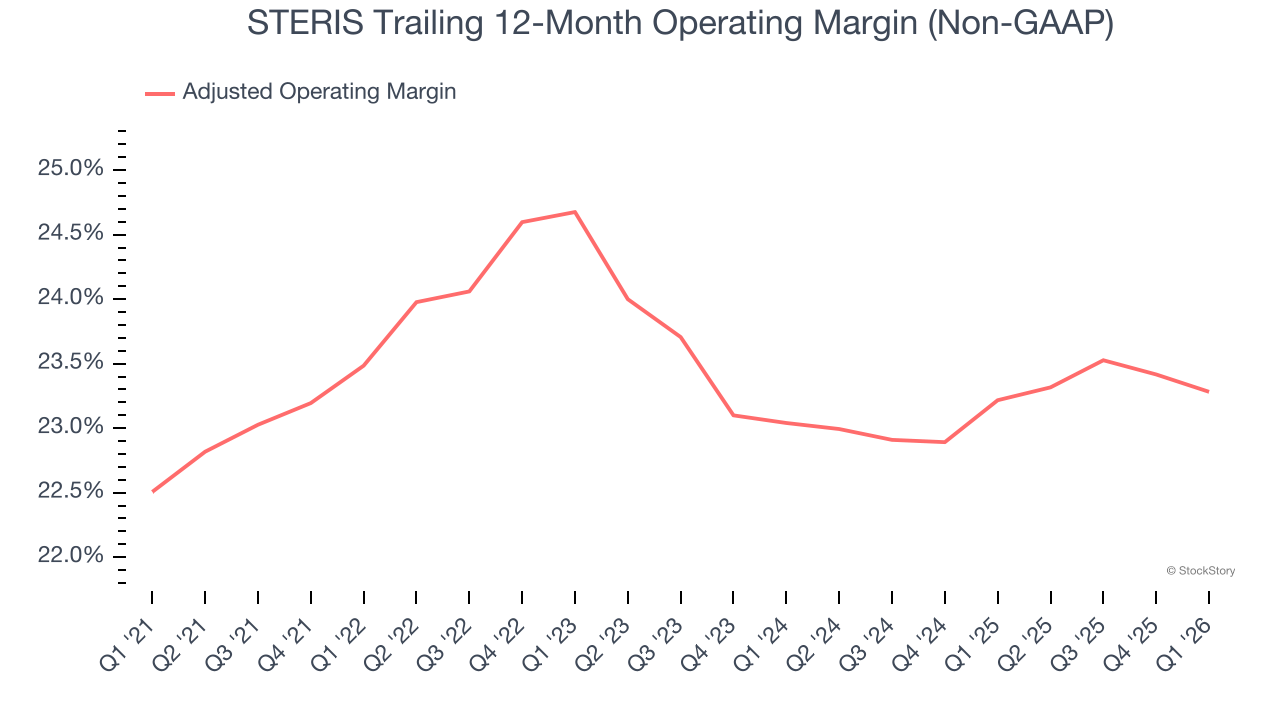

2. Adjusted Operating Margin in Limbo

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

Analyzing the trend in its profitability, STERIS’s adjusted operating margin might have fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its adjusted operating margin for the trailing 12 months was 23.3%.

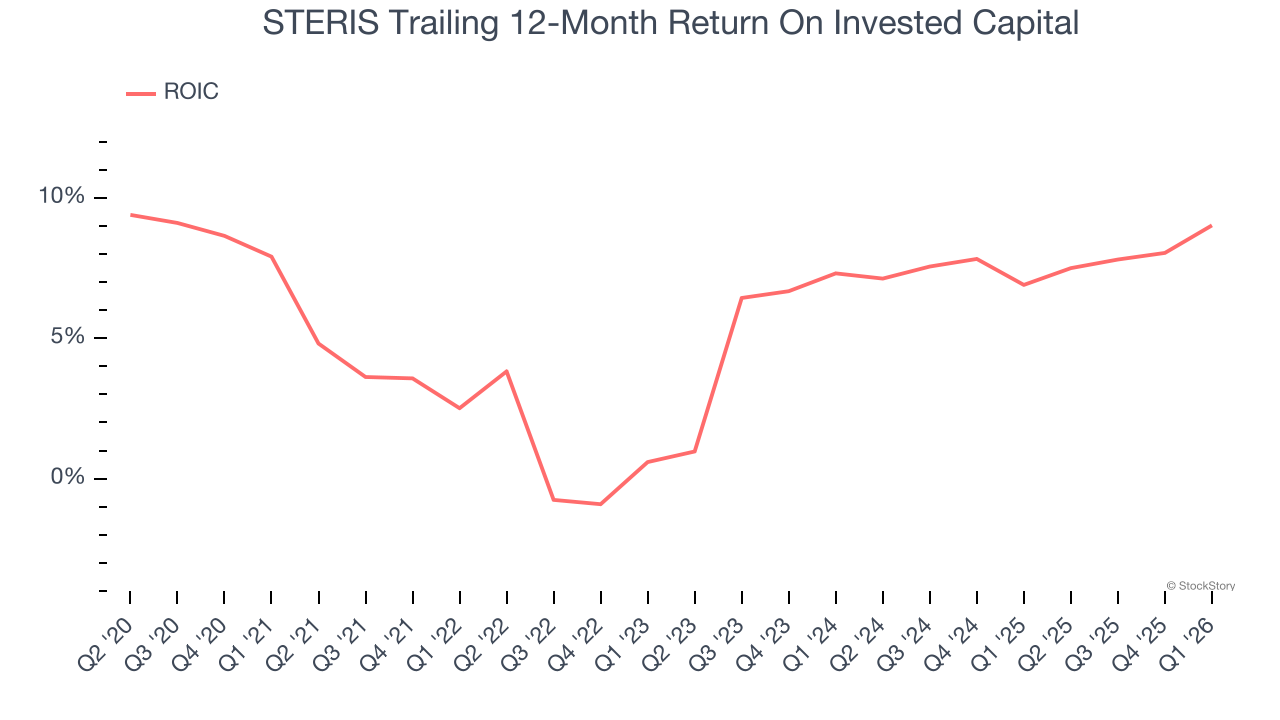

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

STERIS historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5.3%, somewhat low compared to the best healthcare companies that consistently pump out 20%+.

Final Judgment

STERIS isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 17.9× forward P/E (or $202.39 per share). This valuation multiple is fair, but we don’t have much faith in the company. We’re pretty confident there are superior stocks to buy right now. We’d suggest looking at a safe-and-steady industrials business benefiting from an upgrade cycle.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Microsoft%20headquarters%20By%20Peter.jpeg)