Chipmakers and AI stocks have been pushing the market higher this year. A big reason is Nvidia (NVDA), which keeps signing major deals around the world. That includes a long-term, multigenerational partnership with Meta Platforms (META) to deploy millions of GPUs, a $3.4 billion deal with IREN (IREN) for AI cloud capacity, and even smaller players like Digi Power X (DGXX) committing $35 million. The trend is that when Nvidia signs a deal, the companies involved tend to get immediate attention from investors.

That brings SharonAI Holdings (SHAZ) into focus. The Australian neocloud company recently announced a six-year compute deal with Nvidia, centered on building 72 megawatts of new data center capacity and scaling up to 40,000 Grace Blackwell GB300 GPUs.

The setup follows Nvidia’s AI factory model and is aimed at enterprises, startups, and research institutions. The structure is based on revenue sharing and credit support, giving SharonAI Holdings a way to scale without heavy upfront capital, while Nvidia earns from both hardware and ongoing usage.

After the announcement, SharonAI Holdings expanded its total AI factory capacity to 132 MW, with 102 MW already contracted, and is targeting more than 55,000 Nvidia GPUs by mid-2027. The stock, which was already up over 4,000% year-to-date (YTD), jumped again in pre-market trading before pulling back.

Still, a big deal and a quick rally are not the same as a long-term investment case. Is this Nvidia partnership enough to support the current valuation, or if this is just momentum driven by headlines? Let’s find out.

A Look at the Numbers

SharonAI Holdings describes itself as a neocloud company, focused on building local AI infrastructure and providing the compute and storage needed to run large AI workloads for businesses and governments.

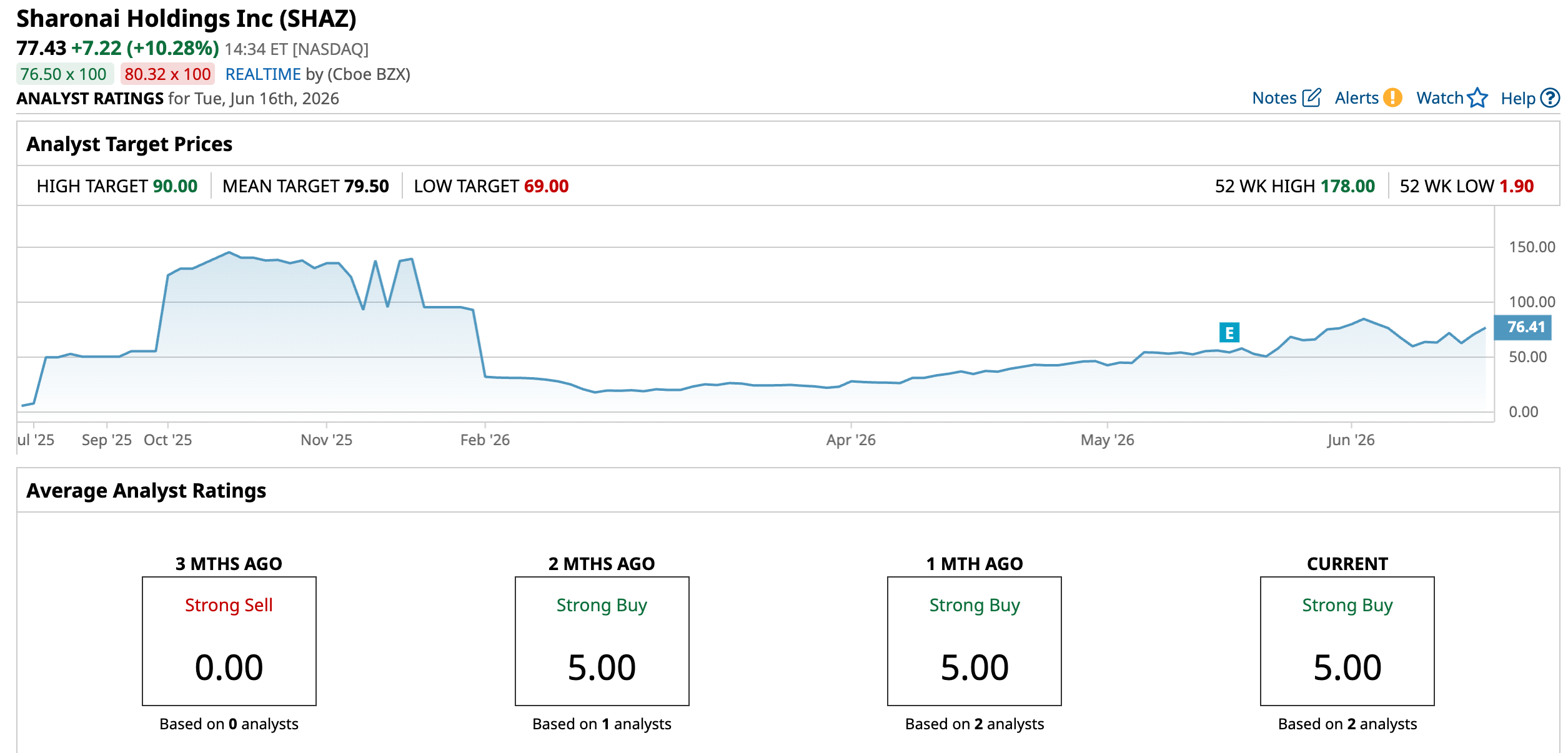

The stock has been on a massive run. Over the past 52 weeks, it is up 1,339.96%, and it has climbed another 3,901.58% so far this year alone.

In Q1 2026, revenue was just $294,000, down 9.5% year-over-year (YOY), while cost of revenue jumped 67.7% to $525,000. That flipped the company to a gross loss of $231,000, compared to a small profit last year, showing it is still heavily in the build phase. Operating loss widened to $2.8 million, and adjusted EBITDA dropped to $2.2 million as expenses ramped up.

Net loss came in at $20.0 million, up sharply from $1.4 million a year ago. A big part of that was non-cash, including about $70 million tied to convertible note valuation, partly offset by a $66 million gain from an investment sale. Even so, the core picture is clear. Spending is rising much faster than revenue. Earnings per share landed at about -$1.43, missing expectations.

What’s Driving SharonAI’s Growth

SharonAI Holdings is working with Cisco Systems (CSCO) and Nvidia to build Australia’s first Cisco Secure AI Factory. The setup combines Cisco’s servers, networking, and security tools with 1,024 NVIDIA Blackwell Ultra GPUs.

The idea is to give companies access to strong AI computing power while keeping all data inside Australia, in line with the country’s National AI Plan. VAST Data’s storage systems and Nextdc Ltd (NXT.AX) data centers help handle the scale and speed, and customers can test and run AI projects on the platform.

That push continues with its expanded deal with VAST Data, where SharonAI Holdings is rolling out 600PB of storage across its AI cloud. Based on typical requirements, that is enough to support data needs for around 100,000 GPUs. It puts the company among the larger sovereign AI setups in Australia and the wider Asia-Pacific region, targeting government, enterprise, and AI-focused clients that want data kept locally.

To actually deliver all this, SharonAI Holdings has partnered with World Wide Technology, which handles the heavy lifting on infrastructure buildout, sourcing equipment, and managing deployment. That includes rolling out Nvidia Blackwell systems at scale, helping the company turn these plans into working capacity across the region.

What Analysts See Ahead

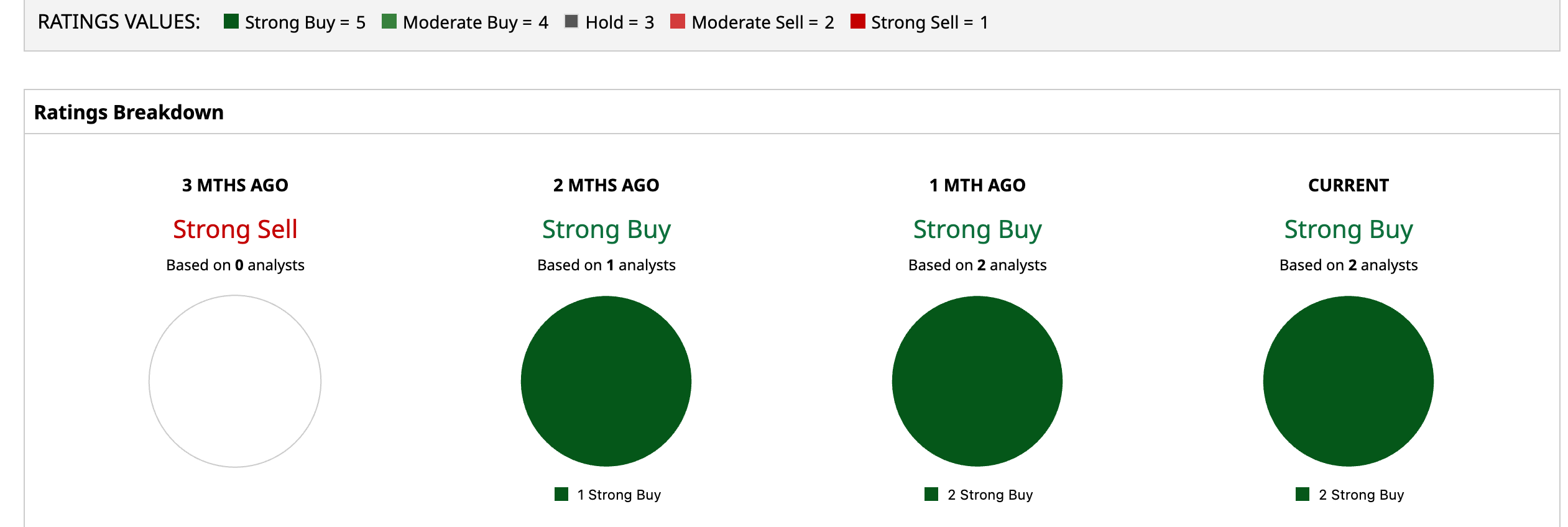

Compass Point’s Michael Donovan started coverage on SharonAI Holdings in April 2026 with a “Buy” rating and a $50 target, and has since U while keeping the same rating. The upgrade came after key developments like the Nvidia deal and new contract wins.

Cantor Fitzgerald is positive too, but more cautious. It began coverage with an “Overweight” rating and a $40 target, which has since been reflected closer to $69 in some updates. While it sees the upside from deals like the $1.25 billion ESDS contract, it also flags execution as a real risk, especially given the scale of what the company is trying to build.

Even so, both of the two analysts covering SHAZ currently rate it a “Strong Buy”, and the mean target of $79.50 implies 2.67% upside from current price levels.

Conclusion

SharonAI has clearly tapped into one of the strongest themes in the market right now, and the Nvidia deal adds real credibility to its long-term positioning. But the numbers still show a company in heavy build mode, with revenue yet to catch up to the scale of its ambitions. That gap matters, especially after such an extreme run. At this point, SHAZ looks less like a value-backed buy and more like a high-beta bet on execution. The most likely path near term is continued volatility, with upside tied to contract delivery rather than new announcements alone.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/AI%20technology%20concept%20by%20NMStudio789%20via%20Shutterstock.jpg)

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

/Sign%20of%20Intel%20at%20entrance%20%20by%20michaelmond.jpeg)