FuelCell Energy (FCEL) stock tumbled after the company reported weaker-than-expected fiscal second-quarter 2026 results, including a wider-than-anticipated loss and a 5% year-over-year (YOY) decline in revenue. However, the earnings-driven selloff did little to shake Canaccord Genuity’s confidence in the company’s long-term prospects.

In a surprising vote of confidence, the firm upgraded FuelCell Energy to “Buy” from “Hold” and raised its price target to a Street-high $30 from $12, arguing that the company is uniquely positioned to capitalize on the rapidly growing artificial intelligence (AI) data center power market. The bullish call comes as FuelCell’s commercial pipeline has surged, with the vast majority of opportunities now tied to AI and data center customers, fueling expectations that a transformative contract announcement could be on the horizon.

About FuelCell Energy Stock

FuelCell Energy is a clean-energy technology company that develops and manufactures fuel cell platforms designed to provide reliable, low-emission electricity for utilities, industrial customers, municipalities, and increasingly, AI-focused data centers. Headquartered in Danbury, Connecticut, FuelCell Energy has recently shifted its strategic focus toward addressing the growing power demands of AI infrastructure, a market management believes could become a significant growth driver. FuelCell Energy has a market cap of $1.15 billion.

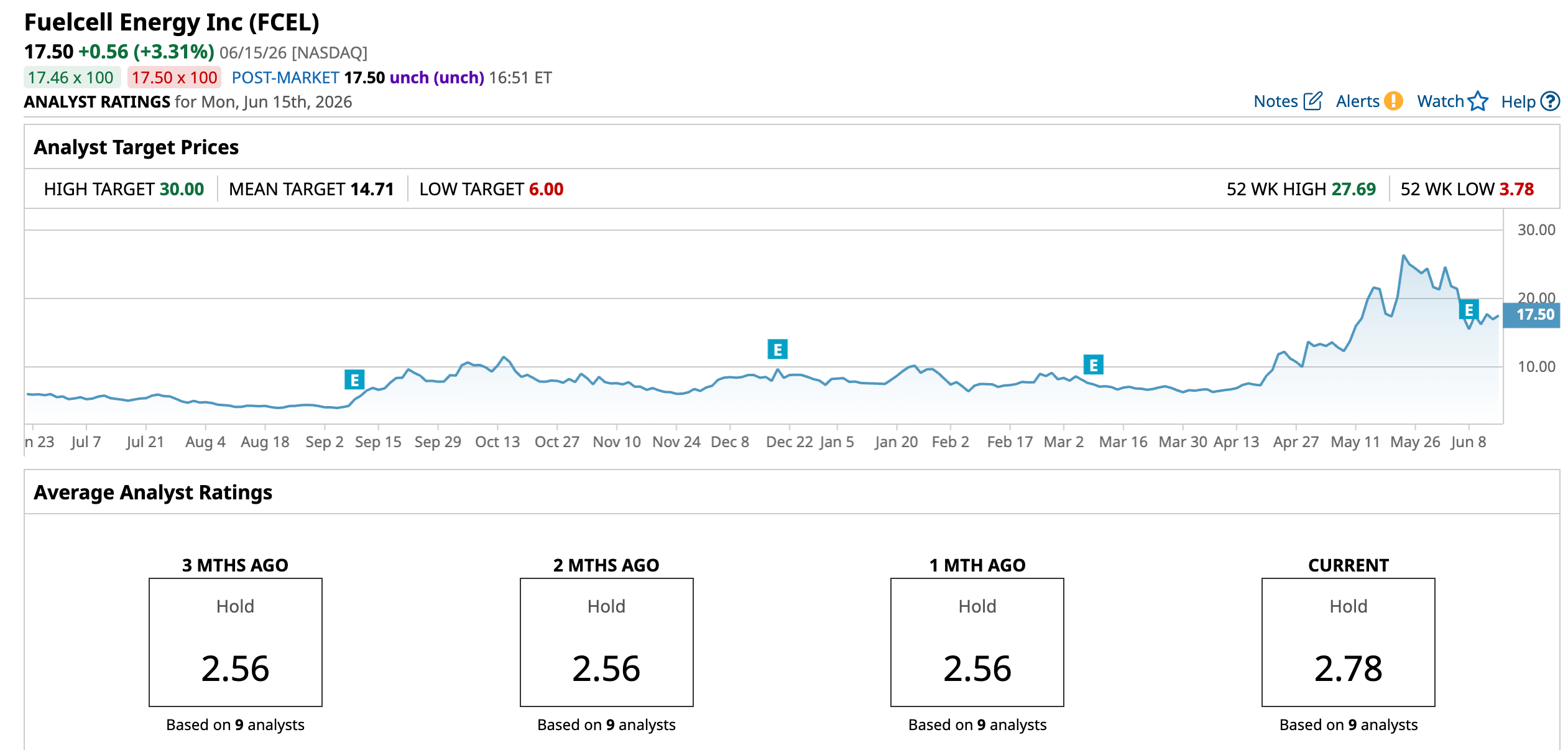

FCEL has been one of the market’s most explosive and volatile clean-energy stocks over the past year. Despite sharp pullbacks along the way, the stock has surged 190.22% over the past 52 weeks, including a remarkable 139.4% gain year-to-date (YTD) and a 163.95% rally over just the past three months. The primary driver behind this extraordinary move has been investor enthusiasm surrounding the company’s growing opportunity to provide power solutions for AI-focused data centers, a market that is experiencing unprecedented electricity demand.

FuelCell’s pipeline has expanded dramatically to 4 gigawatts, increasing speculation that the company could secure a transformative contract in the near future.

However, the stock’s recent trading action highlights significant volatility. On June 8, FCEL plunged 10.6% after reporting fiscal second-quarter 2026 results that missed Wall Street expectations. Investors initially focused on the disappointing financial performance, sending shares sharply lower.

Nevertheless, the sell-off proved short-lived. On June 9, FuelCell shares rebounded 12.8% as investors shifted their attention back to the company’s rapidly growing AI data center pipeline. Sentiment received an additional boost when Canaccord Genuity upgraded the stock and raised its price target, citing growing confidence.

Volatility continued over the following sessions. The stock retreated another 7.3% on June 10 as traders took profits following the sharp rebound. Yet bullish sentiment quickly returned on June 11, with shares climbing 9.13% as investors once again embraced the AI infrastructure narrative and Canaccord’s bullish outlook.

The stock is currently trading at a premium compared to industry peers at 7.65 times forward sales.

Q2 Results Missed Expectations

FuelCell Energy reported fiscal second-quarter 2026 results on June 8. For the quarter ended April 30, revenue declined 5% YOY to $35.6 million, below expectations. The decrease was primarily driven by lower service revenue and lower generation revenue as the company’s Groton project underwent repairs. These headwinds were partially offset by higher product revenue from module deliveries to customers in Korea and stronger Advanced Technologies revenue.

Profitability deteriorated significantly during the quarter. Net loss widened to $77.6 million, compared with a net loss of $37.7 million in the second quarter of fiscal 2025. Gross loss increased to $12.9 million from $9.4 million a year earlier, while operating loss more than doubled to $77.9 million from $35.8 million in the prior-year quarter. Adjusted EBITDA remained negative as the company continued investing in growth initiatives and project execution. Nevertheless, adjusted net loss per share improved to $0.53 from $1.53 in the prior-year period, but missed the consensus estimate.

Despite the weak earnings performance, FuelCell highlighted substantial progress in its AI-focused growth strategy. The company’s sales pipeline expanded 267% sequentially to 4 gigawatts, with the majority of opportunities tied to AI data centers and digital infrastructure customers. Management believes growing electricity demand from AI applications is creating a significant market opportunity for FuelCell’s distributed power generation solutions, particularly where grid access is constrained.

To capitalize on this opportunity, FuelCell introduced a standardized 12.5-megawatt fuel-cell power block designed specifically for large-scale data center deployments. The company is also planning up to $275 million of investments to expand its manufacturing facility in Torrington, Connecticut, increasing annual production capacity from 350 megawatts to 500 megawatts.

In addition, management reported progress on its carbon-capture partnership with ExxonMobil Technology and Engineering Company, including shipment of the first carbon-capture modules to the Netherlands.

On the other hand, one area that remains a concern is backlog. Total backlog declined 9.9% YOY to $1.1 billion as of April 30, compared with $1.3 billion a year earlier.

Analysts predict loss per share to be $1.84 for fiscal 2026, an improvement of 58.28% YOY, and increases 15.22% to a loss of $1.56 for fiscal 2027.

What Do Analysts Expect for FuelCell Stock?

While Canaccord Genuity has turned increasingly bullish on FuelCell Energy’s long-term prospects and significantly raised its price target, many analysts remain considerably more cautious and continue to adopt a wait-and-see approach.

Recently, TD Cowen raised its price target on FuelCell Energy from $9 to $16 but maintained a “Hold” rating, following the earnings release.

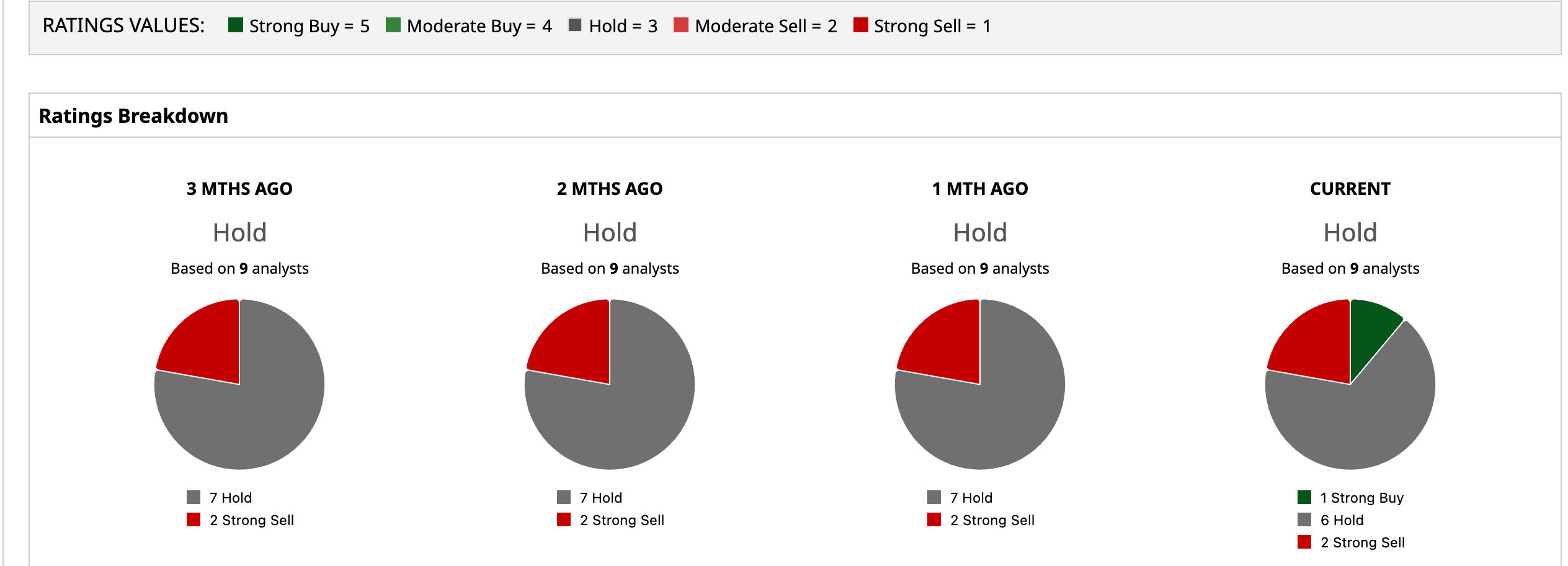

Moreover, FCEL stock has a consensus “Hold” rating overall. Among the nine analysts covering the stock, one recommends a “Strong Buy,” six analysts stay cautious with a “Hold” rating, and two recommend a “Strong Sell” rating.

While the stock is trading above its average price target of $14.71, Canaccord Genuity’s Street-high target price of $30 suggests that the stock could rally as much as 71.43%.

On the date of publication, Subhasree Kar did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Space/Rocket%20launching%20into%20space%20by%20BEST%20BACKGROUNDS%20via%20Shutterstock.jpg)

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/Close-up%20shot%20of%20Rivian%20R1T_%20Image%20by%20Trong%20Nguyen%20via%20%20Shutterstock_.jpg)