/Marsh%20%26%20McLennan%20Cos_%2C%20Inc_%20office%20building-by%20JHVEPhoto%20via%20Shutterstock.jpg)

With a market cap of $80.3 billion, Marsh & McLennan Companies, Inc. (MRSH) is a leading global professional services firm specializing in risk, insurance, and consulting. The New York City-based company provides advisory services that help clients manage risk, optimize workforce strategies, and improve organizational performance.

Companies worth $10 billion or more are generally described as “large-cap” stocks, and Marsh & McLennan fits right into that category with its market cap exceeding this threshold. Its key competitive advantage lies in its diversified portfolio of market-leading businesses spanning insurance brokerage, reinsurance, consulting, and risk advisory services. The company’s broad geographic footprint and ability to cross-sell services across businesses further strengthen its competitive position, making Marsh McLennan one of the most resilient and dominant players in the professional services and risk management industry.

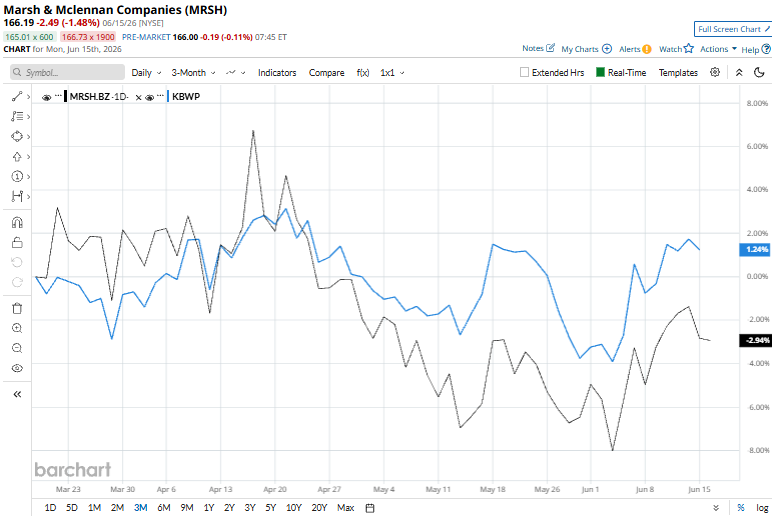

But it’s not all sunshine and rainbows for the stock. MRSH is currently trading 24.6% below its 52-week high of $220.32. Shares of MRSH have declined 7.2% over the past three months, trailing the Invesco KBW Property & Casualty Insurance ETF (KBWP), which gained marginally over the same time frame.

However, MRSH has tanked 10.4% on a YTD basis, underperforming KBWP’s 4.7% returns. Moreover, shares of MRSH have plunged 23.6% over the past 52 weeks, trailing the ETF’s marginal gains over the same time frame.

MRSH has been trading below its 50-day and 200-day moving averages for the past year, reinforcing a sustained bearish trend.

On June 1, shares of Marsh McLennan rose 1.6% after the company completed its previously announced acquisition of TriBridge Partners, a Maryland-based independent benefits broker and retirement and wealth advisor. The acquisition strengthens Marsh McLennan Agency's Mid-Atlantic operations by adding expertise in employee benefits, wealth management, and personal lines insurance to its existing property and casualty capabilities.

In the competitive arena of insurance brokers, Aon plc (AON), MRSH’s top rival, is in the lead, declining 6.7% over the past 52 weeks.

Wall Street remains cautiously bullish about its prospects. The stock has a consensus rating of “Moderate Buy” from the 25 analysts covering it, and the mean price target of $200 represents a 20.3% premium over the current market price.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/Green%20hydrogen%20by%20Scharfsinn%20via%20Shutterstock.jpg)

/Abbvie%20Inc%20HQ%20photo-by%20vzphotos%20via%20iStock.jpg)