Looking back on beverages, alcohol, and tobacco stocks’ Q1 earnings, we examine this quarter’s best and worst performers, including PepsiCo (NASDAQ:PEP) and its peers.

These companies' performance is influenced by brand strength, marketing strategies, and shifts in consumer preferences. Changing consumption patterns are particularly relevant and can be seen in the rise of cannabis, craft beer, and vaping or the steady decline of soda and cigarettes. Companies that spend on innovation to meet consumers where they are with regards to trends can reap huge demand benefits while those who ignore trends can see stagnant volumes. Finally, with the advent of the social media, the cost of starting a brand from scratch is much lower, meaning that new entrants can chip away at the market shares of established players.

The 13 beverages, alcohol, and tobacco stocks we track reported a strong Q1. As a group, revenues beat analysts’ consensus estimates by 4.9% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady as they are up 4.8% on average since the latest earnings results.

PepsiCo (NASDAQ:PEP)

With a history that goes back more than a century, PepsiCo (NASDAQ:PEP) is a household name in food and beverages today and best known for its flagship soda.

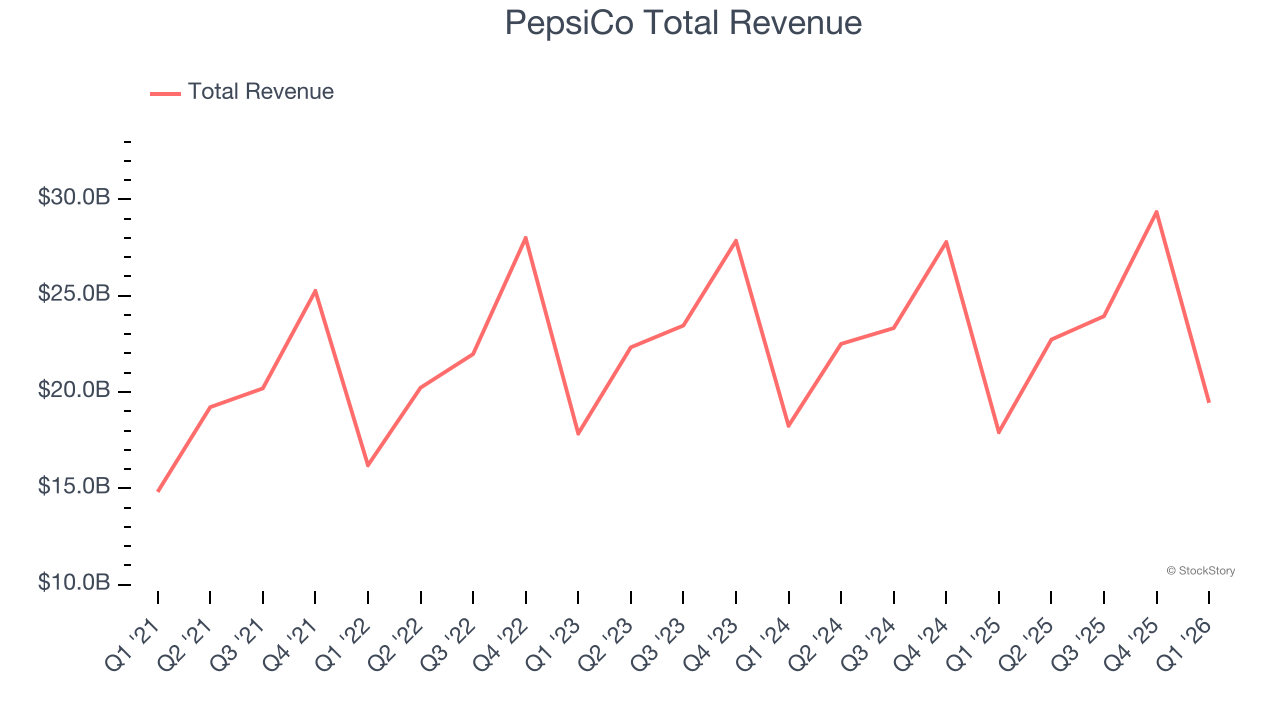

PepsiCo reported revenues of $19.44 billion, up 8.5% year on year. This print exceeded analysts’ expectations by 2.9%. Overall, it was a strong quarter for the company with a solid beat of analysts’ revenue and EBITDA estimates.

Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 7.3% since reporting and currently trades at $143.54.

Is now the time to buy PepsiCo? Access our full analysis of the earnings results here, it’s free.

Best Q1: Vita Coco (NASDAQ:COCO)

Founded in 2004 followed by a 2021 IPO, The Vita Coco Company (NASDAQ:COCO) offers coconut water products that are a natural way to quench thirst.

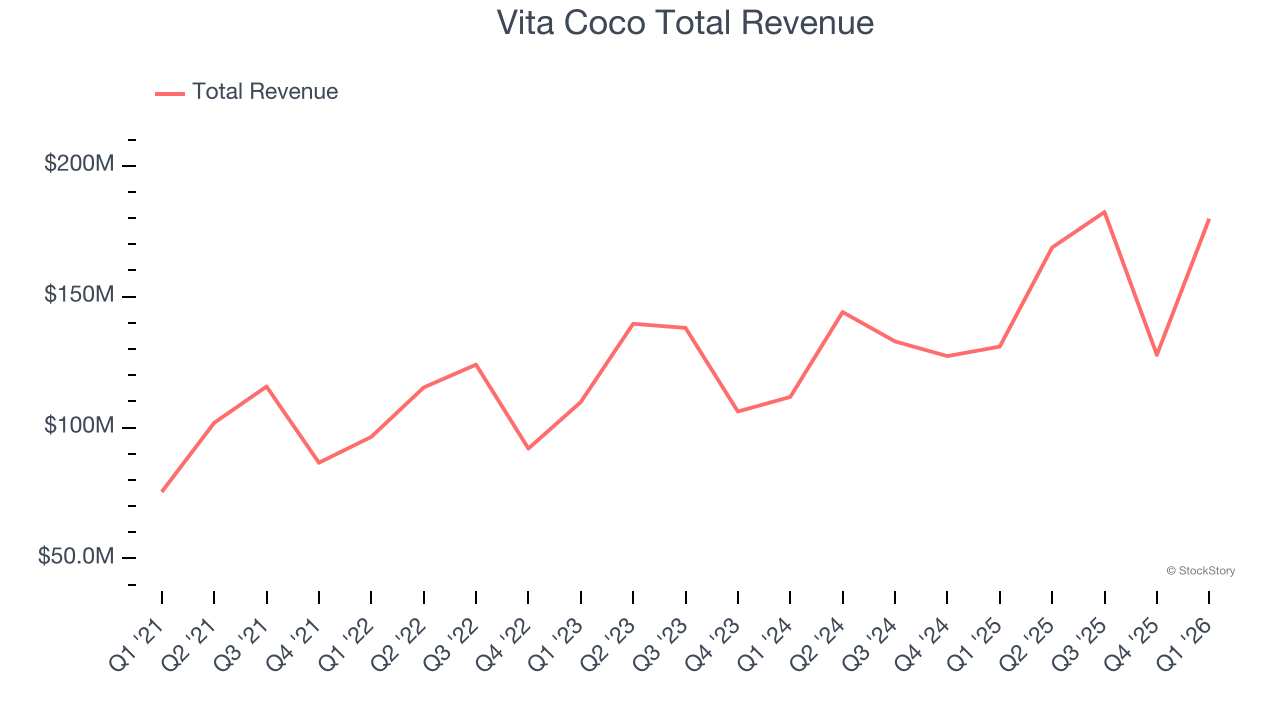

Vita Coco reported revenues of $179.8 million, up 37.3% year on year, outperforming analysts’ expectations by 20.5%. The business had a stunning quarter with a beat of analysts’ EPS and EBITDA estimates.

Vita Coco achieved the biggest analyst estimate beat among its peers. The market seems happy with the results as the stock is up 51.5% since reporting. It currently trades at $78.24.

Is now the time to buy Vita Coco? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Boston Beer (NYSE:SAM)

Known for its flavorful beverages challenging the status quo, Boston Beer (NYSE:SAM) is a pioneer in craft brewing and a symbol of American innovation in the alcoholic beverage industry.

Boston Beer reported revenues of $433.9 million, down 4.4% year on year, in line with analysts’ expectations. It was a softer quarter as it posted a significant miss of analysts’ adjusted operating income and EPS estimates.

Boston Beer delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 24.2% since the results and currently trades at $179.72.

Read our full analysis of Boston Beer’s results here.

MGP Ingredients (NASDAQ:MGPI)

Headquartered in Atchison, Kansas, MGP Ingredients (NASDAQ:MGPI) is a leading supplier of high-quality ingredients to the food and beverage industry

MGP Ingredients reported revenues of $106.4 million, down 12.5% year on year. This number surpassed analysts’ expectations by 1.4%. It was a very strong quarter as it also put up a beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

MGP Ingredients pulled off the highest full-year guidance raise but had the slowest revenue growth among its peers. The stock is down 19.7% since reporting and currently trades at $16.24.

Read our full, actionable report on MGP Ingredients here, it’s free.

Altria (NYSE:MO)

Best known for its Marlboro brand of cigarettes, Altria (NYSE:MO) offers tobacco and nicotine products.

Altria reported revenues of $4.76 billion, up 5.3% year on year. This result topped analysts’ expectations by 4%. Overall, it was a strong quarter as it also recorded a solid beat of analysts’ EBITDA and revenue estimates.

The stock is up 5.1% since reporting and currently trades at $71.68.

Read our full, actionable report on Altria here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.

/Space/Planet%20earth%20with%20flying%20rocket%20by%20Sergey%20Mironov%20via%20Shutterstock.jpg)

/Alphabet%20(Google)%20Image%20by%20Markus%20Mainka%20via%20Shutterstock.jpg)

/Jen-Hsun%20Huan%20NVIDIA's%20Founder%2C%20President%20and%20CEO%20by%20jamesonwu1972%20via%20Shutterstock.jpg)

/Robinhood%20app%20on%20phone%20by%20Andrew%20Neel%20via%20Unsplash.jpg)