/cmdtyView%20Stock%20Photo%201.png)

Now valued at a market cap of just over $8 billion, Duolingo (DUOL) stock has more than doubled over the past year, outperforming even the Nasdaq-100 Index ($IUXX) amid its race to new highs. Founded in 2011, Duolingo is a language-learning platform and mobile application based out of Pittsburgh.

The company went public in July 2021, and has since returned 36% to shareholders. After the growth stock's breakout performance over the last 52 weeks, let’s see if you should buy DUOL stock at the current valuation.

How Did Duolingo Perform in Q3 of 2023?

In Q3 of 2023, Duolingo increased its daily active users, or DAUs, by 63% year-over-year to 24.2 million, while monthly active users grew 47% to 83.1 million. It ended the September quarter with 5.8 million paid subscribers, an increase of 60% year-over-year.

Total bookings were up 49% as the company increased sales by 43%, while subscription bookings in Q3 rose to 54% at $121.3 million. Its stellar growth metrics allowed Duolingo to report net income of $2.8 million in Q3, compared to a net loss of $18.4 million in the year-ago quarter.

Duolingo’s adjusted EBITDA (earnings before interest, tax, depreciation, and amortization) rose by 10x to $22.5 million, indicating a healthy margin of 16.3%. Its operating cash flow also rose 4x to $37.7 million while free cash flow stood at $33.5 million, up from just $6.1 million in the year-ago period.

The strong performance in Q3 allowed Duolingo to raise its full-year guidance. The company estimates total bookings to grow 40% year-over-year with an adjusted EBITDA margin forecast between 16.6% and 16.9%, representing a 13-point increase.

Duolingo Looks to Diversify

At its core, Duolingo is an e-learning platform that enables its users to learn foreign languages. Over the years, Duolingo has successfully increased its user growth on the back of gamification, resulting in higher retention and engagement rates.

The Duolingo platform operates on a freemium model where you can use the app for free or subscribe to gain access to advanced features. The company has grown its subscribers at a rapid pace, up from just 1.1 million at the end of 2020. This growth is the key driver of sales for the company, as it generated 77% of revenue from subscriptions in Q3.

Duolingo has gained traction in a competitive and highly fragmented space. Over the years, it has converted new learners into subscribers, and given the number of languages in the world, Duolingo has massive potential to grow in the upcoming decade.

In late 2023, Duolingo announced the launch of a new Music course, unlocking another revenue stream in the process. Further, it can add new subjects, which should help it further build out the platform's e-learnings ecosystem - creating a flywheel effect for future growth as it attracts new users, too.

Is DUOL Stock a Good Buy Right Now?

Analysts expect Duolingo’s sales to rise from $369 million in 2022 to $700 million in 2024. Its adjusted earnings are forecast at $0.81 per share in fiscal 2024, compared to a loss of $1.51 per share in 2022.

Priced at 11.5 times forward sales and 253.3 times forward earnings, DUOL is not cheap. But if the company can end 2024 with a free cash flow margin of 30%, it would be priced at 26 times FCF, which is not too steep.

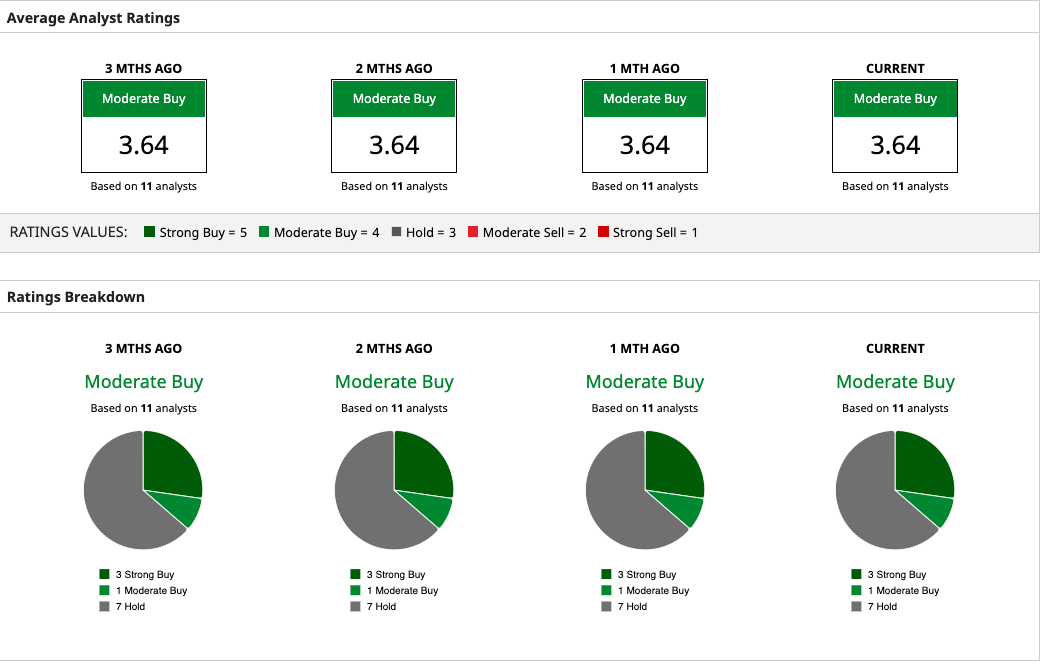

Out of the 11 analysts covering DUOL, three recommend “strong buy,” one recommends “moderate buy,” and seven recommend “hold.” The shares have already hit their average 12-month price target from analysts, but the Street-high target price of $230 - newly hiked by Bank of America this month - indicates upside potential of nearly 19%.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)