Nvidia (NVDA) is still the king of the AI trade, but the vibe around the stock has clearly changed. Bulls still point to massive AI spending from hyperscalers. Bears are now asking a harder question. How much of that spending is real demand, and how much is a loop of companies funding each other?

That is why TS Lombard’s Cisco (CSCO) comparison landed so hard. The firm just warned that Nvidia’s run has echoes of the dot-com era, when Cisco looked unstoppable right before the market reset.

Nvidia’s latest quarter, though, still showed no sign of a slowdown, which is why the debate is so sharp right now.

Is NVDA Priced for Perfection?

Nvidia is not just a chipmaker anymore. It has become the backbone of AI infrastructure. Its GPUs, networking gear, and software now sit inside the biggest cloud and data center buildouts in the world. That makes NVDA a simple stock to follow and a very hard stock to value. When AI demand is hot, Nvidia looks like a machine. When sentiment cools, it can look like a very expensive machine.

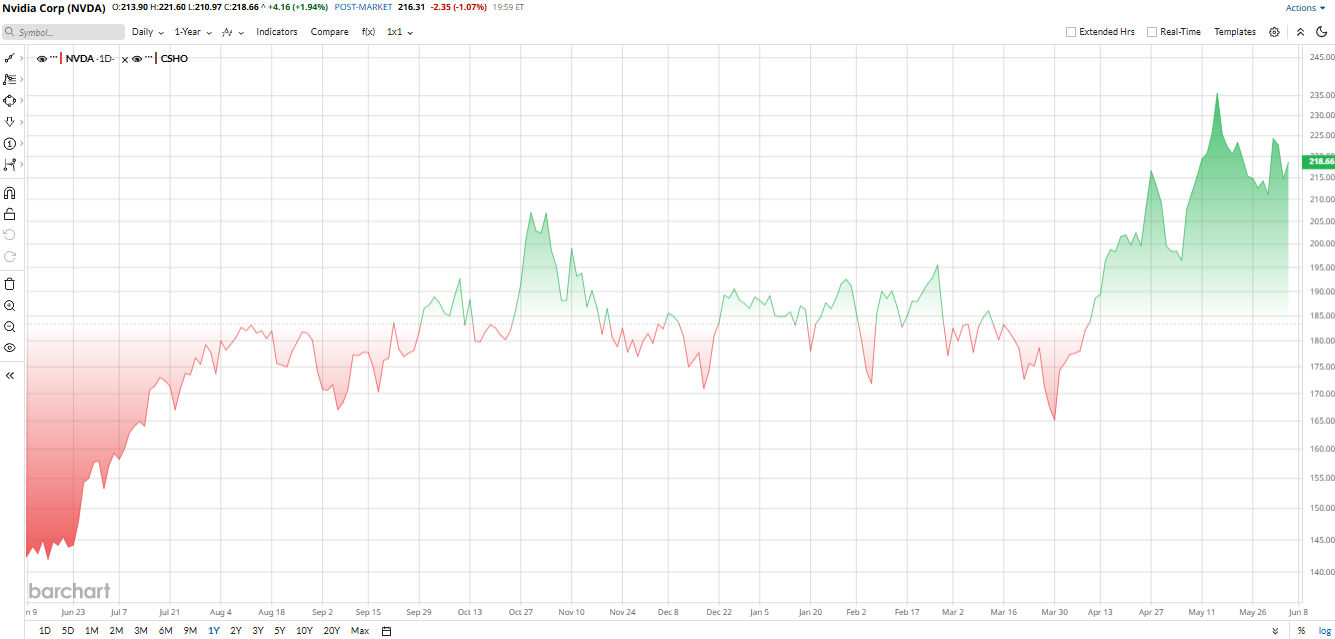

The stock has done what great momentum names usually do. Over the past 12 months, NVDA has climbed about 50%, and Barchart data shows it was still up more than 6% over the prior month heading into early June. The technical picture stayed firm too, with the stock trading above both its 50-day and 200-day moving averages. That matters because it tells you the trend is still intact, even after a huge run. In simple words, buyers have kept showing their love for Nvidia.

Valuation is where the Cisco talk starts to get real. Nvidia’s forward PE sits around 24x, which is below a semis industry median near 26x. That sounds cheaper than the headlines suggest. But on EV to EBITDA, Nvidia still looks rich at roughly 39 times versus an industry average around 28. So the stock is not screaming cheap. It is still priced for strong growth, strong margins, and very little stumble in the AI story.

TS Lombard's Warning

TS Lombard's warning argues that Nvidia is not weak today, but that investor expectations may be running too far ahead of reality, much as they did with Cisco during the dot-com era. As TS Lombard's Dario Perkins put it, “Perhaps NVIDIA is the new Cisco.”

The concern centers on circular financing within the AI ecosystem. Companies continue spending heavily on chips, networking, and data centers, but some of that capital may be circulating among the same players. Investors largely shrugged off the warning, but it reignited debate over whether Nvidia's stock has already shown too much future growth.

Nvidia Crushes Q1 Earnings Estimate

Nvidia’s latest quarter did not help the bears much. Revenue hit $81.6 billion, up 85% from a year earlier. Data Center revenue alone reached $75.2 billion, up 92%. Edge Computing added $6.4 billion, up 29%. The net income jumped to $58.3 billion, and adjusted EPS came in at $1.87, up 140% year-over-year (YoY). Free cash flow was $48.6 billion, and cash and cash equivalents stood at $13.2 billion.

Jensen Huang said the buildout of AI factories is the largest infrastructure expansion in human history, and that is precisely how Nvidia is framing the moment. Guidance was strong too. The company expects about $91 billion in revenue for the next quarter and gave a clean signal that China data center compute is not in that view.

Nvidia is also busy building beyond the headline GPU trade. In 2026, it rolled out the Vera Rubin platform, new BlueField 4 STX infrastructure, Dynamo software, and new agentic AI tools.

It expanded work with Google (GOOG) (GOOGL) Cloud and Marvell (MRVL), and it kept pushing into automotive with Hyundai, Kia, Uber (UBER), BYD (BYDDY), Geely (GELHY), Isuzu (ISUZY), and Nissan (NSANY). That matters because it shows Nvidia is not relying on one product cycle. It is trying to own more of the AI stack, from compute to networking to edge devices.

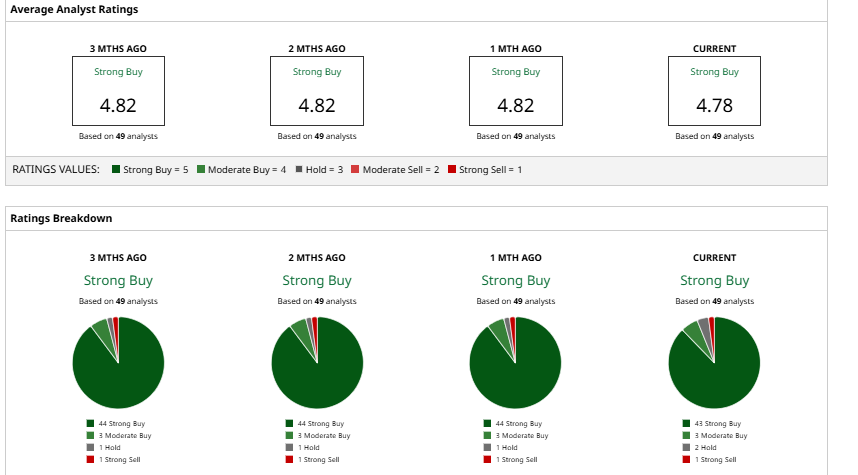

Analysts Still Like NVDA Stock

Analysts are mostly bullish on NVDA stock, but the spread in targets shows the debate is alive. Barchart says the consensus rating is “Strong Buy,” with an average target of $302.32, indicating about a 38% upside.

Morgan Stanley raised its target to $285 and called Nvidia its top semiconductor pick. Goldman Sachs lifted its target to $285 and kept a “Buy” rating. Susquehanna raised its target to $275 and said it expects better results as GB300 ramps.

So the bottom line is that Wall Street still likes Nvidia. It just does not all agree on how much room is left.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)