Looking back on oilfield services stocks’ Q1 earnings, we examine this quarter’s best and worst performers, including Halliburton (NYSE:HAL) and its peers.

Oilfield services companies provide equipment, technology, and services enabling exploration and production activities, including drilling, completion, well intervention, and reservoir evaluation. Their fortunes closely track upstream capital spending cycles. Tailwinds include increased drilling activity during favorable commodity environments, demand for efficiency-enhancing technologies, and growing offshore and unconventional resource development. Headwinds include significant revenue volatility tied to oil and gas price swings and producer spending discipline. Intense competition pressures pricing and margins, while the energy transition may structurally reduce long-term demand. Workforce availability and technological disruption require continuous adaptation.

The 26 oilfield services stocks we track reported a strong Q1. As a group, revenues beat analysts’ consensus estimates by 3.8%.

While some oilfield services stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 4.7% since the latest earnings results.

Halliburton (NYSE:HAL)

Behind nearly every oil and gas well drilled worldwide, Halliburton (NYSE:HAL) provides drilling, completion, and production services that help oil and gas companies extract hydrocarbons from underground reservoirs.

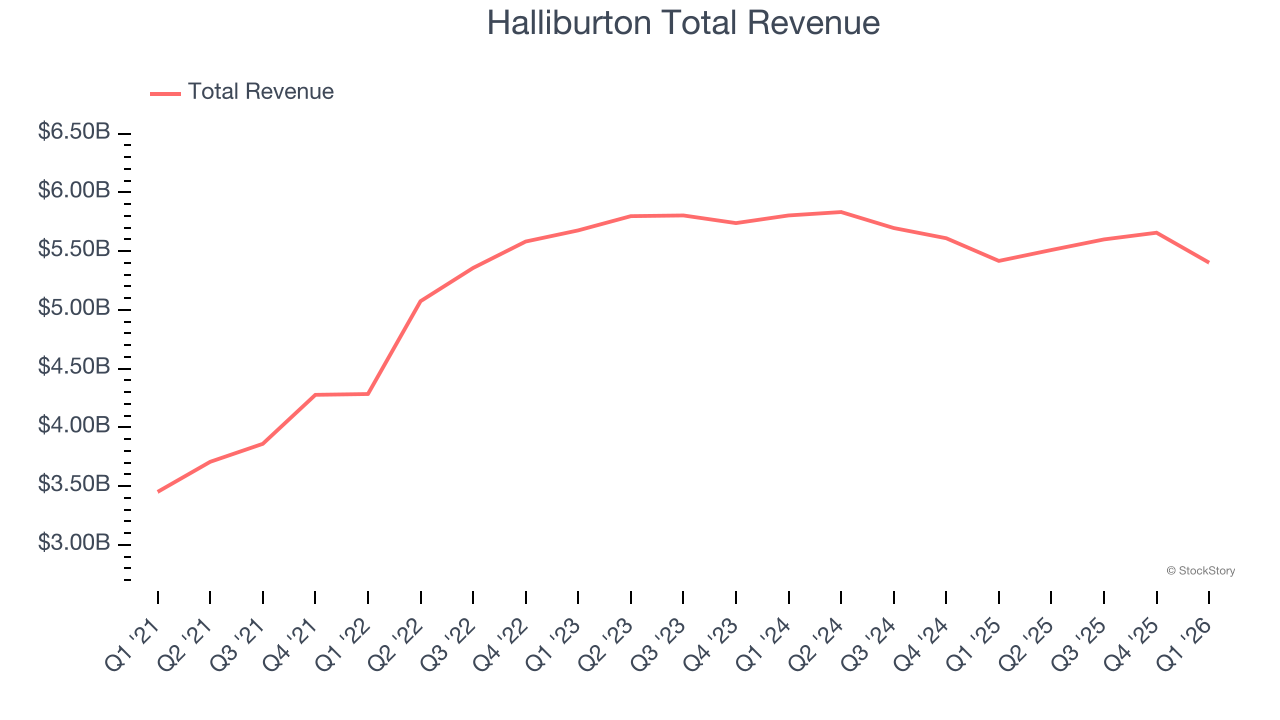

Halliburton reported revenues of $5.40 billion, flat year on year. This print exceeded analysts’ expectations by 1.9%. Overall, it was a strong quarter for the company with a beat of analysts’ EPS and EBITDA estimates.

Interestingly, the stock is up 7.1% since reporting and currently trades at $39.29.

Is now the time to buy Halliburton? Access our full analysis of the earnings results here, it’s free.

Best Q1: Select Water Solutions (NYSE:WTTR)

Managing over 24 billion barrels of produced water annually across major U.S. shale plays, Select Water Solutions (NYSE:WTTR) provides water sourcing, recycling, disposal, and treatment services for oil and gas producers.

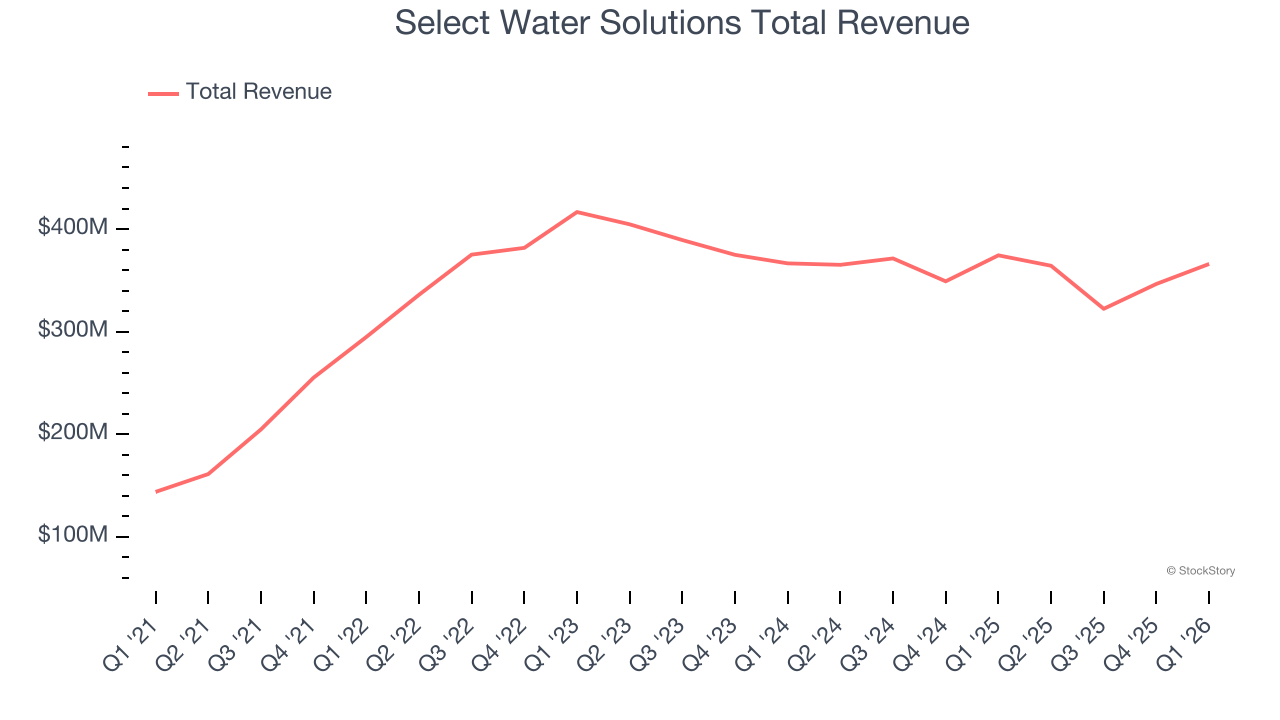

Select Water Solutions reported revenues of $366 million, down 2.3% year on year, outperforming analysts’ expectations by 6.8%. The business had an incredible quarter with a beat of analysts’ EPS and EBITDA estimates.

The market seems content with the results as the stock is up 4.1% since reporting. It currently trades at $17.96.

Is now the time to buy Select Water Solutions? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Borr Drilling (NYSE:BORR)

Operating one of the world's youngest jack-up fleets with an average age under eight years, Borr Drilling (NYSE:BORR) operates jack-up rigs that drill oil and gas wells in shallow waters up to 400 feet deep for exploration and production companies.

Borr Drilling reported revenues of $247 million, up 14% year on year, falling short of analysts’ expectations by 2.1%. It was a disappointing quarter as it posted a significant miss of analysts’ EBITDA and EPS estimates.

Borr Drilling delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 18.3% since the results and currently trades at $5.05.

Read our full analysis of Borr Drilling’s results here.

RPC (NYSE:RES)

Operating primarily in the Permian Basin with 10 hydraulic fracturing fleets, RPC (NYSE:RES) provides specialized services and equipment like hydraulic fracturing, coiled tubing, and cementing to help oil and gas companies complete and maintain wells.

RPC reported revenues of $454.8 million, up 36.6% year on year. This result surpassed analysts’ expectations by 13.6%. It was an exceptional quarter as it also logged EPS in line with analysts’ estimates and an impressive beat of analysts’ EBITDA estimates.

RPC achieved the biggest analyst estimate beat and fastest revenue growth among its peers. The stock is down 10.1% since reporting and currently trades at $6.64.

Read our full, actionable report on RPC here, it’s free.

Baker Hughes (NASDAQ:BKR)

Tracing lineage to a 1907 cable tool drill bit patent, Baker Hughes (NASDAQ:BKR) provides equipment and services for oil and gas drilling, production, and transport.

Baker Hughes reported revenues of $6.59 billion, up 2.5% year on year. This number beat analysts’ expectations by 4.1%. Overall, it was a stunning quarter as it also produced a beat of analysts’ EPS and EBITDA estimates.

The stock is flat since reporting and currently trades at $64.18.

Read our full, actionable report on Baker Hughes here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 6 Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.

/International%20Business%20Machines%20Corp_%20logo%20on%20phone-by%20rafapress%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)