/Wells%20Fargo%20%26%20Co_%20logo%20banner-by%20jetcityimage%20via%20iStock.jpg)

With a market cap of $234.6 billion, Wells Fargo & Company (WFC) is one of the largest financial services companies in the United States. The company provides a wide range of banking, investment, mortgage, and consumer and commercial finance products and services both domestically and internationally.

Companies valued at $200 billion or more are generally considered “mega-cap” stocks, and Wells Fargo fits this criterion perfectly. It operates through four main segments: Consumer Banking and Lending; Commercial Banking; Corporate and Investment Banking; and Wealth and Investment Management.

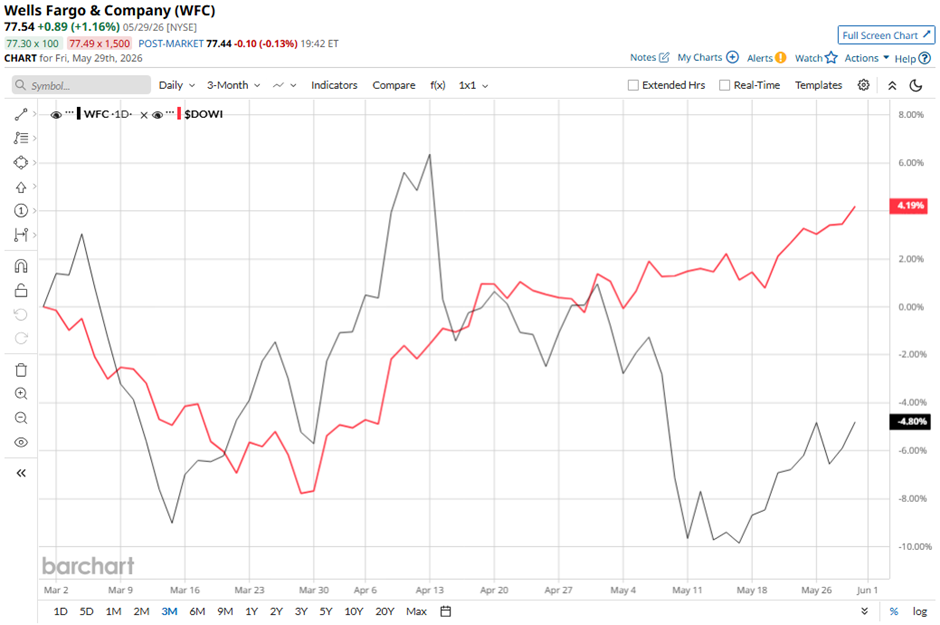

The San Francisco, California-based company stock has declined 20.7% from its 52-week high of $97.76. Shares of Wells Fargo have declined 4.8% over the past three months, lagging behind the Dow Jones Industrials Average's ($DOWI) 4.2% gain over the same time frame.

WFC stock is down 16.8% on a YTD basis, underperforming DOWI’s 6.2% return. In addition, shares of the biggest U.S. mortgage lender have risen 5.2% over the past 52 weeks, compared to Dow Jones' 21.2% increase over the same time frame.

The stock has been trading below its 50-day moving average since January. Also, it has fallen below its 200-day moving average since early February.

Shares of Wells Fargo fell 5.7% on Apr. 14 despite a slight EPS beat because investors focused on weaker-than-expected revenue and net interest income (NII). While Q1 2026 EPS of $1.60 exceeded estimates, revenue of $21.45 billion and NII came in at $12.10 billion, both missed consensus. Investor concerns were compounded by a 21.8% year-over-year increase in provision for credit losses to $1.14 billion, a decline in the CET1 capital ratio to 10.3%, and the company merely reaffirming its 2026 NII guidance of approximately $50 billion, below the consensus forecast.

Additionally, WFC stock has underperformed its rival, Citigroup Inc. (C). Citigroup stock has soared 7.9% on a YTD basis and 67.8% over the past 52 weeks.

Despite Wells Fargo’s underperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of “Moderate Buy” from 25 analysts' coverage, and the mean price target of $97.81 is a premium of 26.1% to current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Alibaba%20by%20Photo%20Agency%20via%20Shutterstock.jpg)