Between Wars and Warsh: What Is Driving Bonds Right Now

The past month has delivered a sustained, multi-front attack on long-duration Treasuries, with bond prices bearing the full weight of deteriorating fiscal credibility, geopolitical instability, and a seismic shift at the top of the Federal Reserve.

The closure from the US-Iran war has driven oil and gas prices to their highest levels in four years and is directly feeding the inflation surge now gripping markets. As of today, May 28, the situation remains deeply unstable: the US and Iran have been trading strikes, with both sides accusing the other of violating the existing ceasefire. American forces in Kuwait were the suspected target of an Iranian missile strike overnight, while CENTCOM conducted self-defense strikes near the Strait of Hormuz earlier this week. While Axios reported on Thursday that US and Iranian negotiators had reached agreement in principle on a memorandum of understanding for a 60-day ceasefire extension, the Jerusalem Post reported the same day, citing a source familiar with the matter, that Iranian Supreme Leader Mojtaba Khamenei has not approved the drafted MOU, and that this is precisely why President Trump has also not agreed to sign off on it. In effect, there may be working-level alignment between Iranian Foreign Minister Abbas Araghchi and US envoy Steve Witkoff's team, but the two decision-makers who actually matter have not yet given their approval, leaving markets caught between hope and anxiety.

The inflation consequences of this energy shock have been severe. The April CPI came in at its highest annual rate in three years, and the core PCE for April is expected to print at 3.9% year-on-year, which would be the highest reading since May 2023. Adding to the pressure, Moody's downgraded US sovereign debt from Aaa to Aa1 in mid-May, making it the last of the three major rating agencies to strip the US of its top credit rating. The 30-year yield responded by briefly hitting 5.197% on May 19, its highest level since July 2007.

The leadership transition at the Federal Reserve has amplified the uncertainty. Kevin Warsh was confirmed by the Senate in a 54-45 vote on May 13 and sworn in on May 22, succeeding Jerome Powell. His first FOMC meeting is scheduled for June 16-17. Markets, which entered 2026 pricing in rate cuts, have completely repriced: traders are now assigning roughly 50% probability to a rate hike by December 2026, with Fed Governor Waller having stated publicly that he can "no longer rule out rate hikes further down the road if inflation does not abate soon." The combination of these forces has kept sellers firmly in control of the long end.

Context - What the Market Has Done

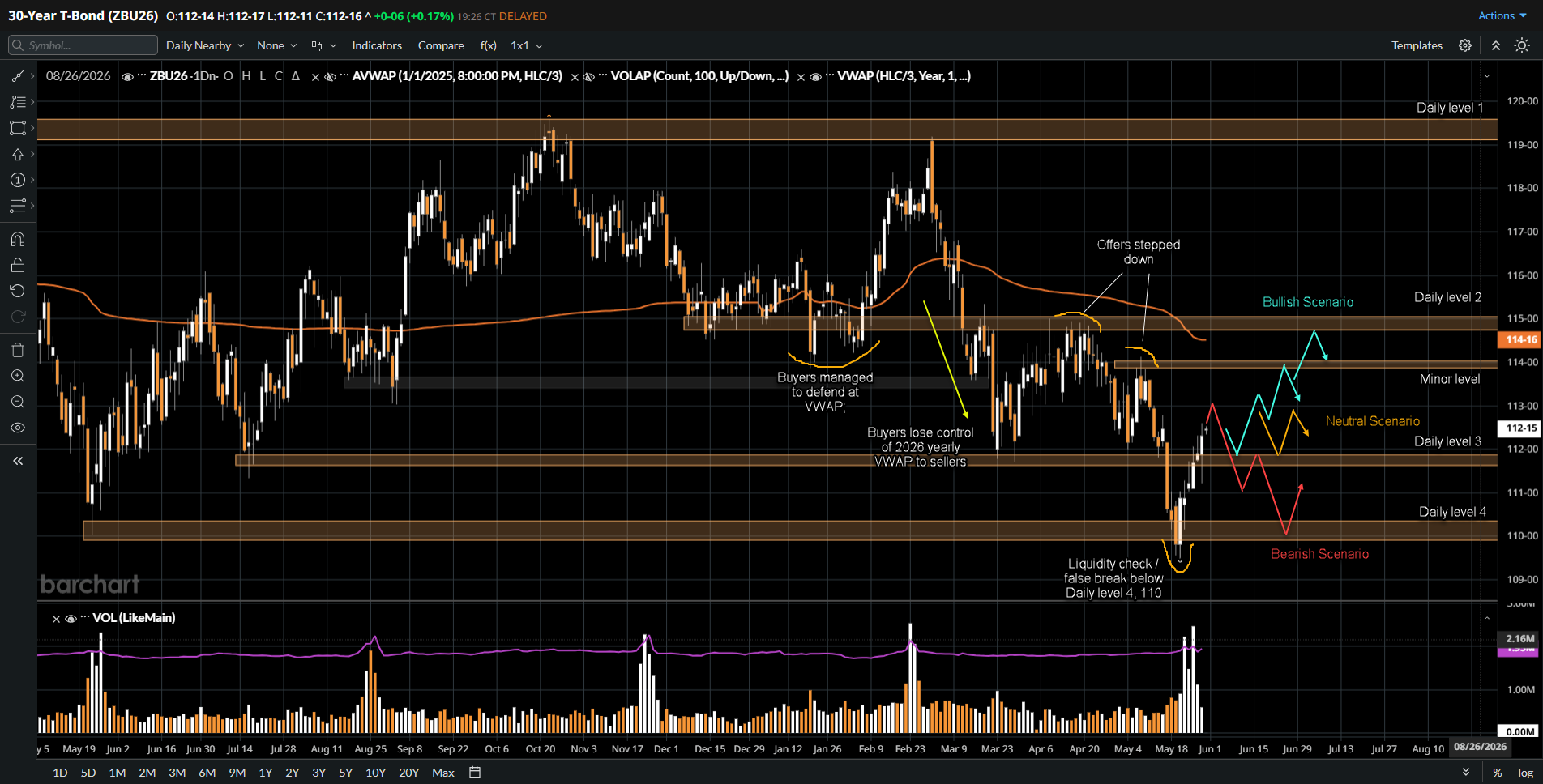

- Market has remained in a broader downward trend within a larger range structure since the start of 2026, with sellers maintaining control of rallies while buyers continue responding at key lower references.

- Sellers previously stepped down offers around the 119 area which marked Daily Level 1 and initiated a broader move lower in price.

- In mid-March, market broke below the 115 area which marked Daily Level 2, where buyers were flushed out aggressively as downside momentum accelerated.

- Responsive buyers were then found at 111 25 which marked Daily Level 3, resulting in a rotational move back toward the 115 area where sellers once again stepped down offers and defended the level successfully.

- During the first week of May, sellers stepped down further into the 114 area which initiated another leg lower through 111 25 and into the 110 area which marked Daily Level 4.

- Market recently produced a false break below the 110 level where buyers responded aggressively, bidding price back above 111 25 and forcing short covering activity near the lows.

- Current price action suggests the market remains rotational for now, although the broader structure still favors sellers unless buyers can reclaim higher resistance references convincingly.

What to Expect in the Coming Weeks

The key level to watch is 111-25 (daily level 3).

Neutral Scenario

- Possible two-way rotation as the market balances below 113 and 111-25 before directional resolution, with neither buyers nor sellers able to assert dominance.

- A possible macro trigger for this scenario would be the ongoing US-Iran peace deal negotiations producing incremental progress but no signed agreement, keeping energy prices elevated but stable and giving neither inflation bulls nor bond bulls a decisive catalyst to act on.

Bullish Scenario

- If buyers are able to continue holding 111 25, expect potential rotation higher toward the 114 area which remains a minor resistance level.

- If sellers fail to defend 114, the market could extend toward the 115 area which marks Daily Level 2 where stronger seller response would be expected.

- A possible macro trigger here would be a signed US-Iran memorandum of understanding and the gradual reopening of the Strait of Hormuz, which would bring energy prices lower, reduce inflationary pressures materially, and shift market pricing away from rate hike territory and back toward a neutral-to-dovish Fed outlook under Warsh.

Bearish Scenario

- Possible push higher which ultimately fails, followed by buyers losing control of 111 25, which could reopen downside movement toward the 110 area, which is Daily Level 4.

- Buyers are expected to respond again near 110, although failure there would expose lower range extensions and reinforce the broader bearish structure.

- The possible macro trigger for this scenario would be a full breakdown of peace negotiations, a fresh escalation in US-Iran hostilities, and an April PCE print at or above the expected 3.9%, cementing the case for a rate hike at Warsh's June 16-17 inaugural FOMC meeting and driving further bond selling from institutional investors and foreign holders of US debt.

Conclusion

ZB is sitting at a technically and fundamentally charged crossroads. The false break and recovery at the 110 level have given buyers something to work with, but the weight of the macro environment remains firmly bearish for long bonds. Inflation is running at multi-year highs, fiscal credibility has been eroded by the Moody's downgrade, and a Fed that was expected to cut rates is now discussing hikes. The singular wildcard that can change everything in this market is the US-Iran conflict: a credible and signed peace agreement reopening the Strait of Hormuz would materially alter the inflation trajectory and the rate path and give the long end room to breathe. Until that clarity arrives, 111-25 remains the line in the sand, and how price interacts with that level over the coming sessions will tell the market's next story.

We believe that professional growth is impossible without the truth found in your own data. Our presence on Barchart bridges the gap between complex exchange data and professional execution. Open an Account and access the tools you need to see your performance clearly.

Disclaimer:

This article is provided for informational and educational purposes only and does not constitute financial, investment, or trading advice. The analysis presented reflects the author’s market observations and opinions at the time of writing and is not a recommendation to buy or sell any futures contract, security, or financial instrument. Futures trading involves significant risk and is not suitable for all market participants. Losses may exceed initial margin deposits, and market conditions can change rapidly.

Any scenarios, levels, or market expectations discussed are hypothetical in nature and are intended solely to illustrate potential market behavior. They do not represent actual trading results and should not be interpreted as guarantees of future performance. Past performance, market behavior, or historical price action are not indicative of future outcomes.

Readers are solely responsible for their own trading decisions and risk management. Always conduct independent research, consider your financial situation and risk tolerance, and consult with a qualified financial professional, if necessary, before engaging in futures or derivatives trading.

/Qualcomm%2C%20Inc_%20logo%20on%20phone-by%20viewimage%20via%20Shutterstock.jpg)

/Advanced%20Micro%20Devices%20Inc_%20logo%20and%20chart%20data-by%20Poetra_%20RH%20via%20Shutterstock.jpg)