/Unitedhealth%20Group%20Inc%20HQ%20photo-by%20jetcityimage%20via%20iStock.jpg)

UnitedHealth Group (UNH) stock slipped more than 2% after Berkshire Hathaway (BRK.B)(BRK.A) revealed it had completely sold its position in the healthcare giant.

The move was part of a broader portfolio reshuffling under new Berkshire chief executive officer Greg Abel. However, UNH remains one of the most compelling long-term turnaround stories in the healthcare sector, and patient investors could see this dip as an opportunity.

Why Berkshire's UnitedHealth Exit Spooked the Market

In August 2025, Berkshire disclosed that it had purchased five million shares of UNH. Soon after, the healthcare stock gained momentum as investors interpreted Warren Buffett's backing as a vote of confidence in the company's recovery under returning chief executive officer Stephen Hemsley.

Berkshire's latest filings reveal the entire position had been liquidated during the first quarter. UNH stock had risen roughly 20% year-to-date (YTD) at the time of the disclosure, following a brutal 2025 in which the stock lost more than 30% of its value and ranked as the worst performer on the Dow Jones Industrial Average ($DOWI).

According to Reuters, analysts who follow Berkshire closely were quick to point out that the exit may say more about internal portfolio decisions than any serious concern about UNH's business trajectory. The report stated:

- Bill Stone, chief investment officer at Glenview Trust Company, noted that Berkshire's trades tend to move markets regardless of who is actually calling the shots. Given how well UNH had recovered heading into the exit, Stone suggested profit-taking was a plausible motive.

- Morningstar analyst Julie Utterback characterized the move as a roster change at Berkshire rather than a fundamental signal about managed care, especially given that the broader health insurance sector reported strong first-quarter 2026 results.

- Senior vice president James Harlow at Novare Capital Management, which owns more than 54,000 UNH shares, told Reuters that while the news may take some air out of the stock in the near term, it does nothing to change the operational momentum clearly building within the company.

UnitedHealth's Operational Turnaround is the Real Story for Investors

UnitedHealth raised its full-year 2026 profit forecast in April after beating Wall Street's first-quarter earnings and revenue expectations. Speaking at the Bank of America Global Healthcare Conference in May 2026, UnitedHealth chief financial officer Wayne DeVeydt said the first four months of the year had all shown strong results with no anomalous month in the data.

"If the trends we saw in the first quarter were to continue, this will be a very strong year," DeVeydt said at the conference.

The company is targeting a return to its long-term earnings growth algorithm of 13% to 16% annually. Management is focused on two core engines to get there: Optum Health, its value-based care arm that now serves over 20 million patients, and Optum Insight, which is being retooled around artificial intelligence to reduce friction across the entire healthcare ecosystem.

UnitedHealthcare chief executive officer Timothy Noel added that all business units are on track to return to targeted margin ranges by 2028. For 2026 specifically, management expects to land in the upper half of its UnitedHealthcare margin targets.

UNH is also making notable operational changes that should win back both customers and providers. UnitedHealthcare announced a 30% reduction in prior authorization volumes and committed to processing all prior authorizations in real time by the end of 2027.

These moves are designed to rebuild trust with physicians and patients after a difficult period that included rising medical costs, criticism of insurer practices, and a federal investigation into government-backed plans.

Is UNH Stock Undervalued?

Analysts tracking UNH stock forecast free cash flow to improve from $16 billion in 2025 to $30 billion in 2030. If UNH stock is priced at 16.33 times forward FCF, which is in line with its 10-year average, it could deliver a 44% return over the next four years. If we adjust for dividends, cumulative returns could be closer to 55%.

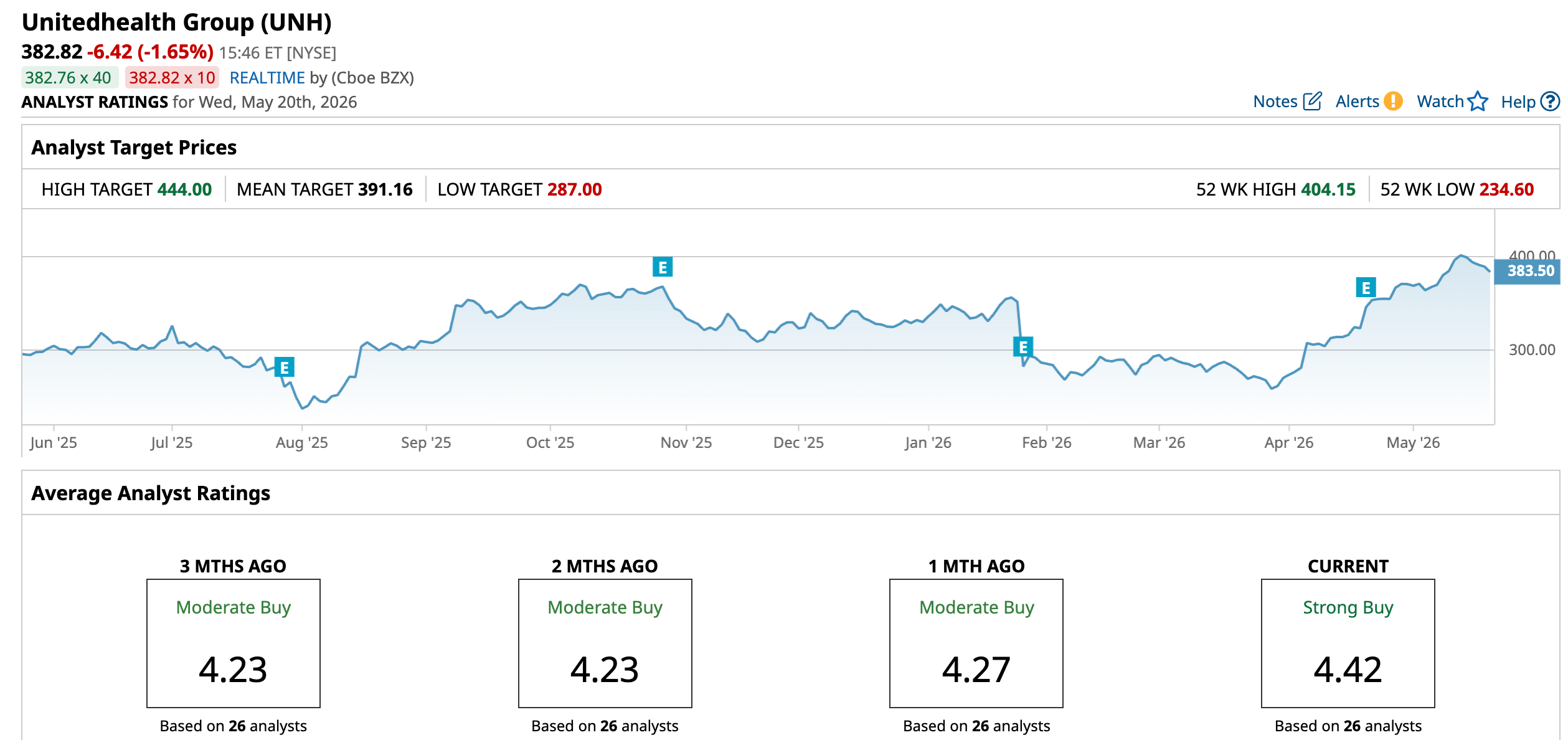

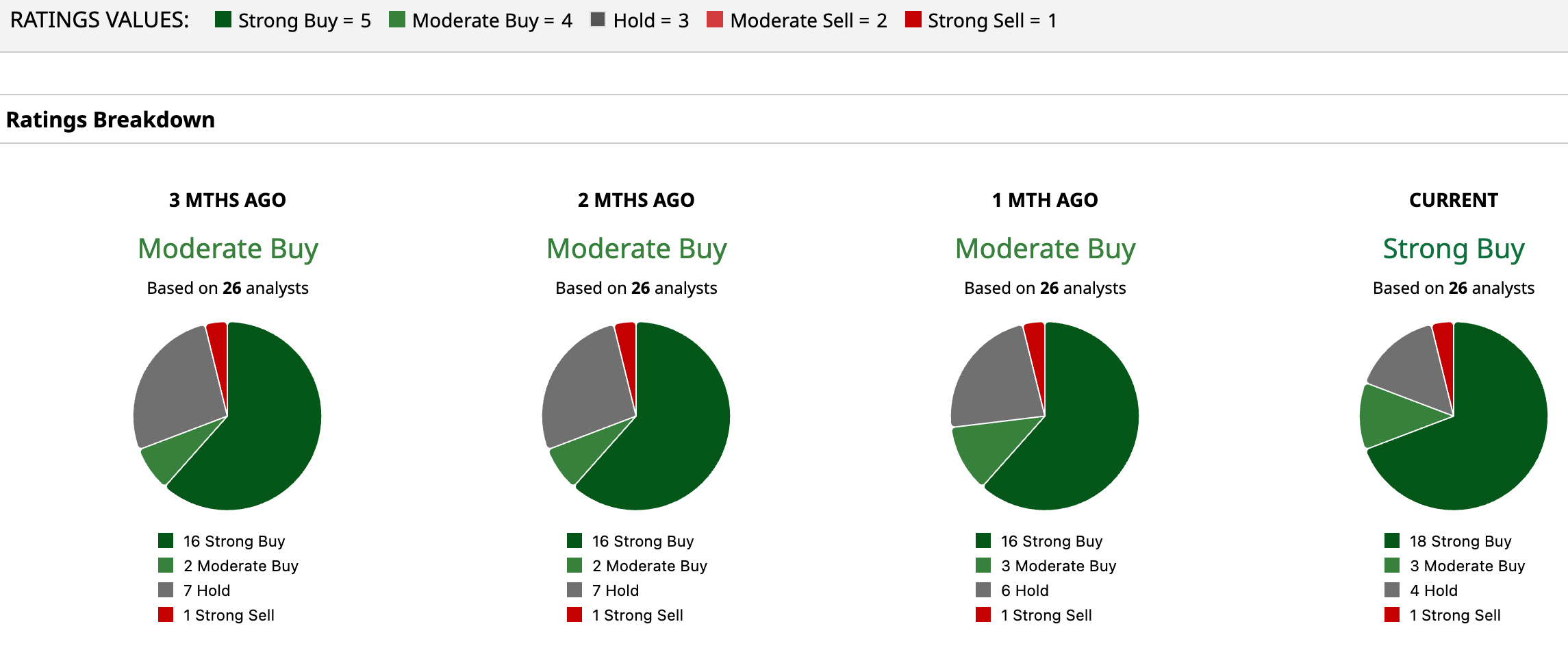

Out of the 26 analysts covering UNH stock, 18 recommend “Strong Buy," three recommend “Moderate Buy," four recommend “Hold," and one recommends “Strong Sell." The average UNH stock price target is $391.16, showing marginal 2.18% upside.

The bottom line for investors: Berkshire's exit is noise.

With a clear path to margin recovery, a growing artificial intelligence investment program north of $1.5 billion in 2026 alone, and management delivering on its commitments quarter by quarter, UNH looks like one of the more compelling opportunities in large-cap healthcare right now.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)