/Lam%20Research%20Corp_%20logo%20on%20phone%20and%20stock%20chart-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

Lam Research Corporation (LRCX) is a global leader in materials engineering and wafer fabrication equipment for the semiconductor industry. Lam Research specializes in advanced thin-film deposition and plasma etch technologies, which are foundational to sculpting the nanoscale architectures of modern microchips. As semiconductor nodes shrink to atomic levels, Lam’s specialized hardware platforms enable the mass manufacturing of high-density 3D NAND flash memory, advanced DRAM, and complex logic circuitry.

Founded in 1980, the company is headquartered in Fremont, California.

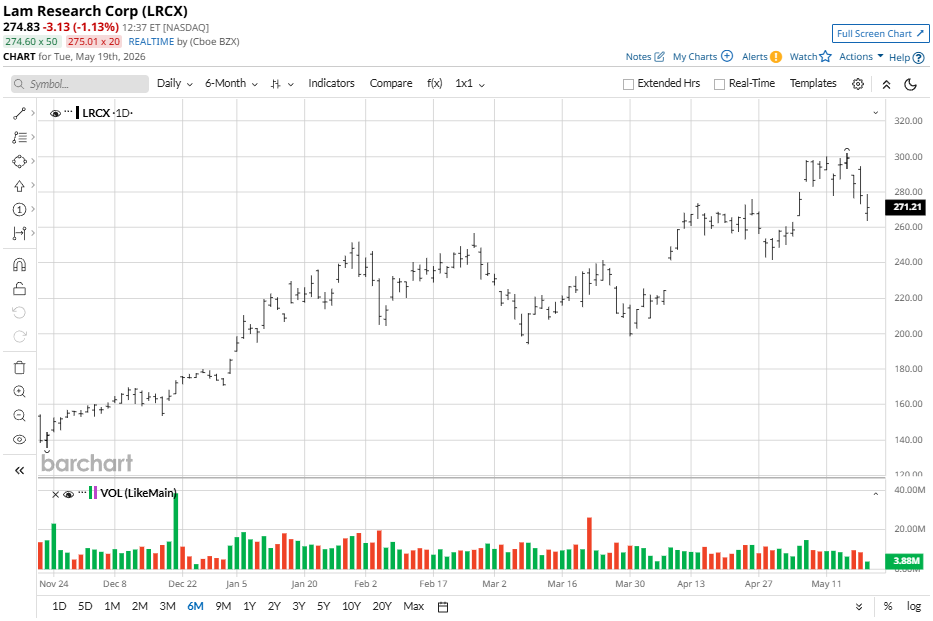

About LCRX Stock

Lam Research stock has seen an aggressive technological pivot toward high-bandwidth memory and advanced packaging infrastructure. The equity has experienced an extraordinary multi-month expansion, hitting an all-time closing high of $299.15 on May 14. The stock trades 245% above its 52-week low, pricing in permanent structural tailwinds.

Compared to the S&P 100 ($OEX), Lam Research has significantly outperformed broader market sentiments. While the index has decent numbers with strong double-digit growth in 52-weeks’ time, Lam Research’s 245% gain simply outshines the S&P.

Displaying an elevated beta of roughly 1.50, the equity carries a significantly higher volatility profile than the standard diversified index, exposing holders to steep short-term pullbacks during high-multiple rotations. However, its direct leverage to physical hardware manufacturing infrastructure has secured its spot as a premier growth vehicle inside the large-cap market.

Lam Research Notes Strong Results

Lam Research delivered an outstanding financial performance for its fiscal third quarter ended March 29, comfortably outpacing Wall Street expectations across all primary metrics. Total revenue rose 24% year-over-year to $5.84 billion, up 9% sequentially and beating consensus projections.

Profitability reached elite thresholds as the corporation achieved a stellar non-GAAP gross margin of 49.9% and a non-GAAP operating margin of 35%, reflecting robust factory efficiencies and an optimal product mix. Non-GAAP diluted earnings per share surged to a record $1.47, exceeding the consensus estimate of $1.36 by 8.1%, driven by relentless global tool demand.

The company's exceptional performance was heavily anchored by the customer support business group, which hit a historic milestone by bringing in its first $2 billion quarter at $2.11 billion in service revenue. Operationally, the firm faced a cash balance decline to $4.77 billion due to aggressive capital deployment for manufacturing expansion, including its second Malaysian facility slated to ramp up in the second half of the year.

Management has issued highly bullish forward guidance for the June quarter, forecasting revenues of $6.60 billion and a further expansion of non-GAAP gross margins to 50.5%. Backed by a scaling industry transition to 1c DRAM nodes and a projected 50% surge in advanced packaging segments, Lam Research raised its calendar 2026 wafer fab equipment market outlook to an unprecedented $140 billion with an upward bias, reinforcing its long-term market share dominance.

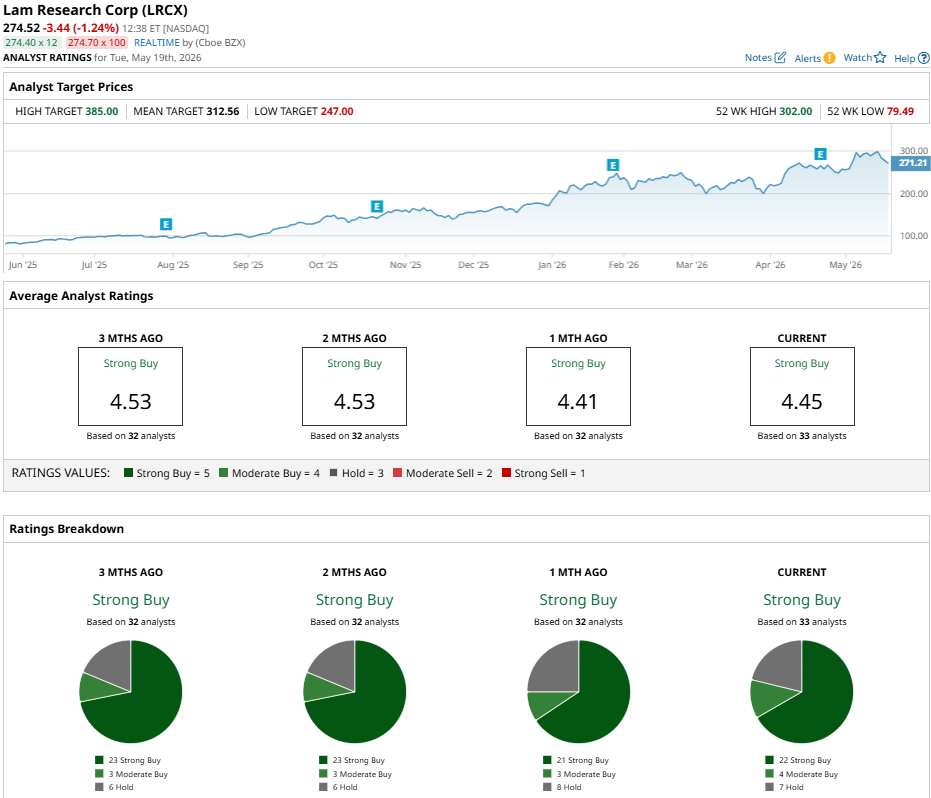

Morgan Stanley Upgrades LRCX

Morgan Stanley has upgraded Lam Research from “Equal weight” to “Overweight,” lifting its price target to $331 from $293, signaling to a potential upside of 14% from the market rate.

Led by analyst Shane Brett, Morgan Stanley simultaneously raised its 2026 wafer fabrication equipment (WFE) forecast to $149 billion, citing extended longevity in the semiconductor equipment cycle. This structural optimism is fueled by expanding leading-edge logic spending and an acute unconstrained bit demand exceeding 40% in both DRAM and NAND memory sectors.

While the analysts downgraded peer Applied Materials (AMAT) to “Equal Weight” due to shifting risk-reward profiles, they heavily backed Lam. After Lam’s shipments underperformed the WFE market by 33 percentage points in 2023 because of cyclical NAND slumps and China export restrictions, it rebounded sharply, beating the sector by 8 percentage points in 2024 with a projected 27 percentage point outperformance in 2025. Morgan Stanley expects this outperformance to persist through 2027, driven by a 59% explosion in NAND systems growth that will surpass prior 2021 peaks.

Operationally, Lam is primed for high-margin market share capture, supported by structural cost efficiencies gained from migrating primary manufacturing to Malaysia and leading the industry's critical 4F2 architecture transition in DRAM and advanced packaging.

Should You Bet on LRCX?

Morgan Stanley’s recent high-profile upgrade to “Overweight” shines a powerful spotlight on Lam Research’s structural recovery in NAND and market share gains in advanced packaging. This bullish momentum underpins a solid consensus "Strong Buy" rating across Wall Street.

Out of 33 analysts tracking the equity, a commanding 22 rate it a "Strong Buy," complemented by four "Moderate Buys" and seven "Holds." With a mean price target of $312.56, the stock offers a highly attractive 14% projected upside from its current market price. Backed by booming enterprise memory demand and its highly efficient Malaysian manufacturing pivot, Lam Research represents a premier, high-alpha vehicle for long-term semiconductor investors.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)