/International%20Business%20Machines%20Corp_%20logo%20on%20phone-by%20rafapress%20via%20Shutterstock.jpg)

Valued at a market capitalization of roughly $209 billion, IBM (IBM) is among the worst-performing mega-cap stocks in 2026. The tech stock has shed almost 25% year-to-date (YTD), making it the biggest laggard among large-cap names.

For a company that just reported one of its strongest quarters in years, that disconnect is worth understanding before you do anything with your money. Let's take a closer look.

IBM Stock Is Down Despite a Stellar Q1

According to reports, IBM ranks last among mega-cap stocks by YTD performance. Other notable laggards so far this year include Palantir Technologies (PLTR), Wells Fargo (WFC), and Microsoft (MSFT).

In Q1 2026, IBM grew revenue 6% year-over-year (YOY) on a constant currency basis to $15.9 billion. Free cash flow (FCF) rose 13% to $2.2 billion, marking the company’s highest Q1 FCF in over a decade. Software sales climbed 8% YOY to $7.1 billion, while the data segment grew by 16%. Interestingly, the mainframe business also posted a 48% revenue gain.

CEO Arvind Krishna said on the earnings call that the company is "off to a strong start" and remains confident in full-year constant currency revenue growth of 5% or more, plus roughly $1 billion in FCF growth for the year.

Shares of IBM had a very strong run coming into 2026, but when the broader market turned volatile, expensive stocks with stretched multiples got hit hardest. The selloff is less about what IBM is doing wrong and more about what the market is repricing across the board.

IBM Enjoys an AI Moat

IBM is embedding artificial intelligence (AI) across its entire portfolio. Its mainframe platform can now run AI inferences directly on transaction data in real time, something that was not possible before. Financial services clients are using this to catch fraud on 100% of transactions rather than using a small sample to assess risk, which IBM says is saving some clients millions of dollars.

The consulting business is seeing its backlog fill up with generative AI work, which now accounts for about 30% of total backlog. IBM's internal AI tool for software development, called Bob, is delivering 45% productivity gains across its developer workforce.

However, macro headwinds — including energy concerns in Europe and a choppy deal environment — add to the caution, even if IBM's own pipeline has not shown material weakness yet.

What Do Analysts Think of IBM Stock?

Analysts tracking IBM stock forecast free cash flow to expand from $14.7 billion in 2025 to $21.8 billion in 2030. If IBM stock is priced at 12.5 times forward free cash flow, which is in line with its 10-year average, it could surge more than 30% within the next four years. If we adjust for dividends, cumulative returns could be even higher.

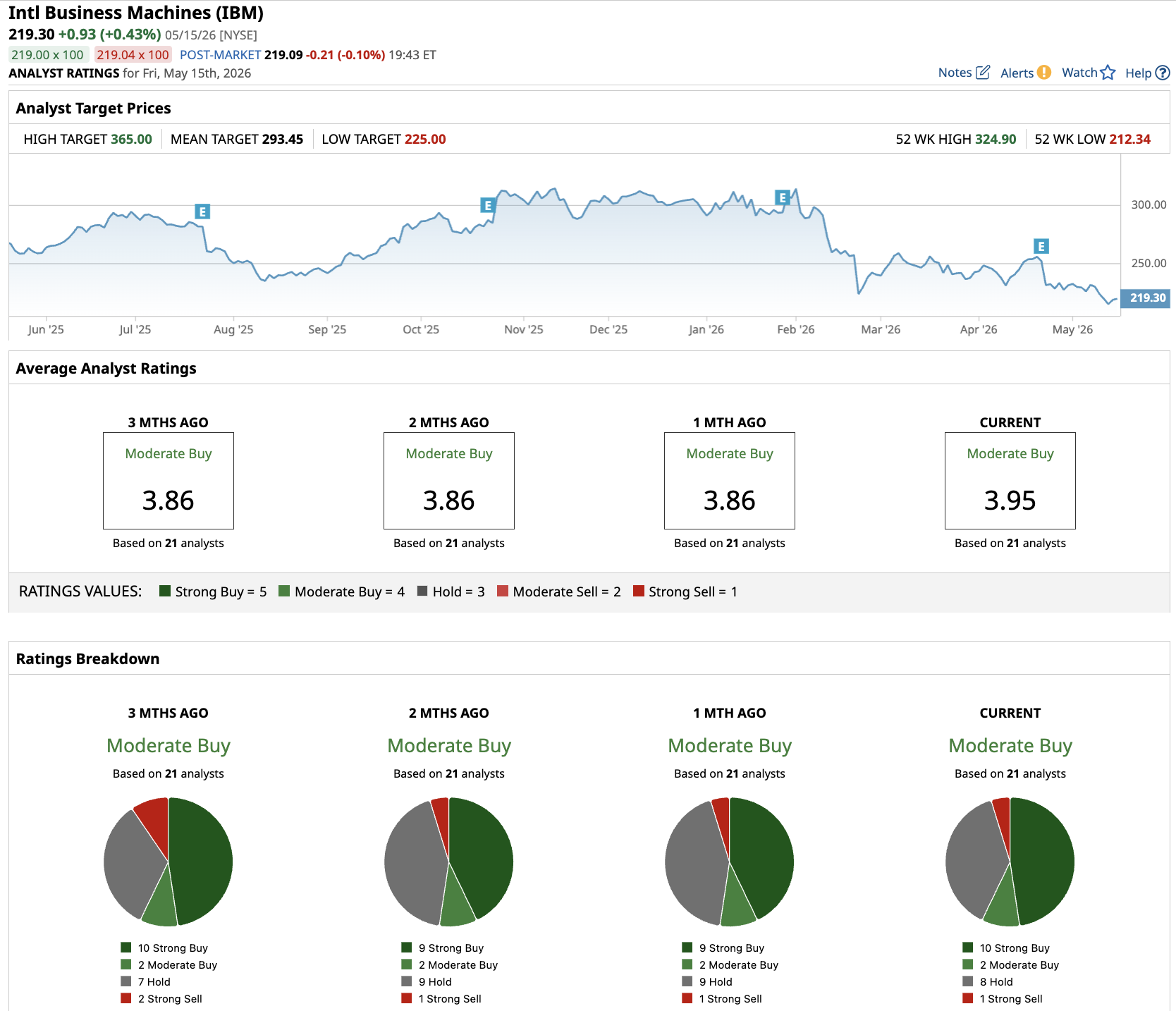

Out of the 21 analysts covering IBM stock, 10 recommend a “Strong Buy,” two recommend a “Moderate Buy,” eight recommend a “Hold” rating, and one analyst recommends a “Strong Sell.” The average price target is $293.45, which represents potential upside of 32% from here.

Investing in IBM carries downside risk, given that the market is yet to reset valuations on mega-cap technology names broadly. Until there is clearer evidence that shares have found a floor and that macro volatility has eased, patience is the smarter move here.

Watching how IBM executes in Q2 will matter far more than reacting to the YTD loss alone. That is when investors will know whether this is a value opportunity or a value trap.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)