I concluded an April 16, 2026, Barchart article on the crude oil futures market with the following:

Expect volatility in crude oil prices over the coming days, weeks, and perhaps months, depending on developments in the Middle East. While historical trading patterns suggest an eventual implosive move, prices could rise before then. Moreover, the current environment supports wide price ranges with prices closely following the daily news cycle. Trading crude oil is optimal in the current environment.

Nearby NYMEX crude oil futures were at $92.57 per barrel on April 15, while nearby Brent futures were at $95.40 per barrel. Prices have been volatile over the past month, but the WTI and Brent futures were higher than the April 15 level on May 18.

Choppy price action in WTI and Brent futures

On February 27, 2026, the day before the U.S. and Israel launched attacks in Iran, nearby NYMEX crude oil futures settled at $67.02 per barrel. On December 16, 2025, the price reached a low of $54.89 per barrel.

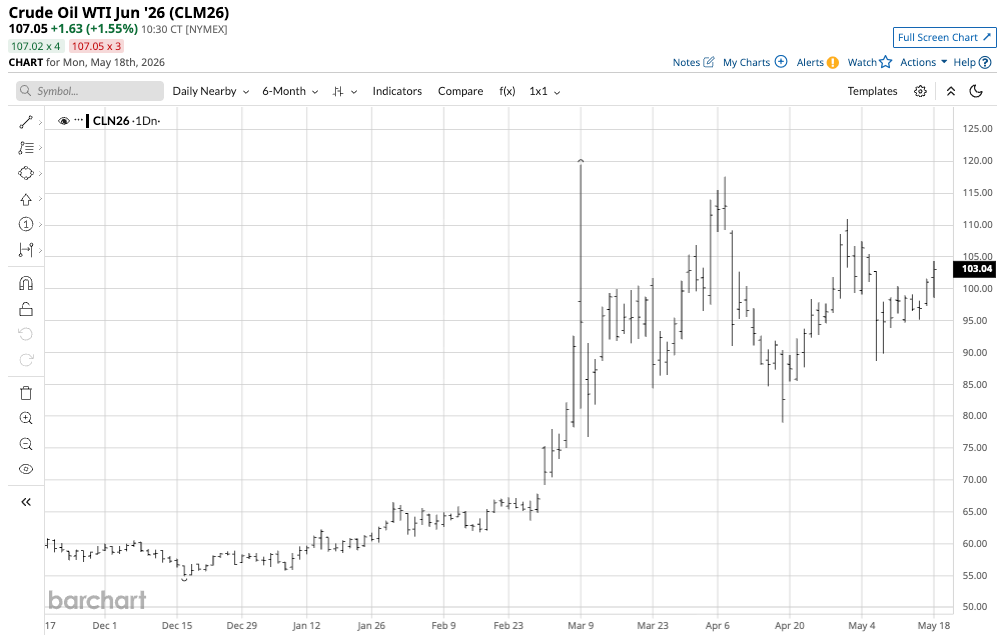

The daily continuous NYMEX WTI futures chart shows that the price spiked to a high of $119.48 on March 9, 2026, and while the energy commodity has made lower highs since the high on March 9, the price was above $107 on May 18, and has been trading around the $100 pivot point since mid-March.

On February 27, 2026, nearby ICE Brent crude oil futures settled at $72.87 per barrel. On December 16, 2025, the price reached a low of $58.72 per barrel.

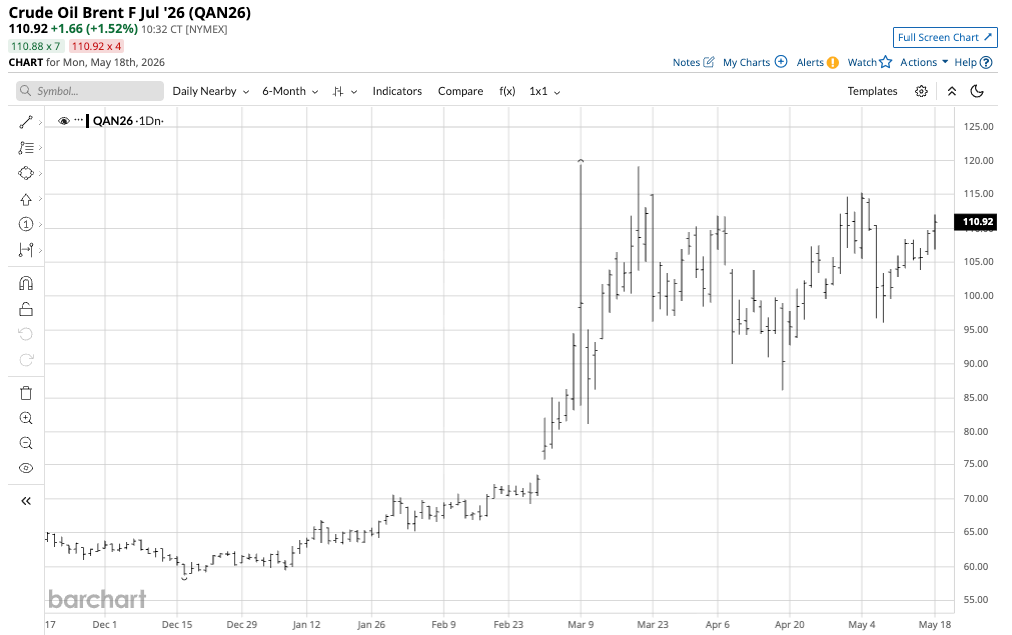

The daily continuous ICE Brent futures chart shows that the price spiked to a high of $119.40 on March 9, 2026, and while the energy commodity has made lower highs since the high on March 9, the price was near $111 on May 18, and has been trading around the $105 pivot point since mid-March.

Backwardations in forward curves

Backwardation is a condition in which the term structure of a commodity market is inverted, meaning that prices for deferred delivery are lower than those for nearby delivery. Backwardation signals short-term supply fears, but they believe that the higher prices will lead to increased production and lower prices in the long term.

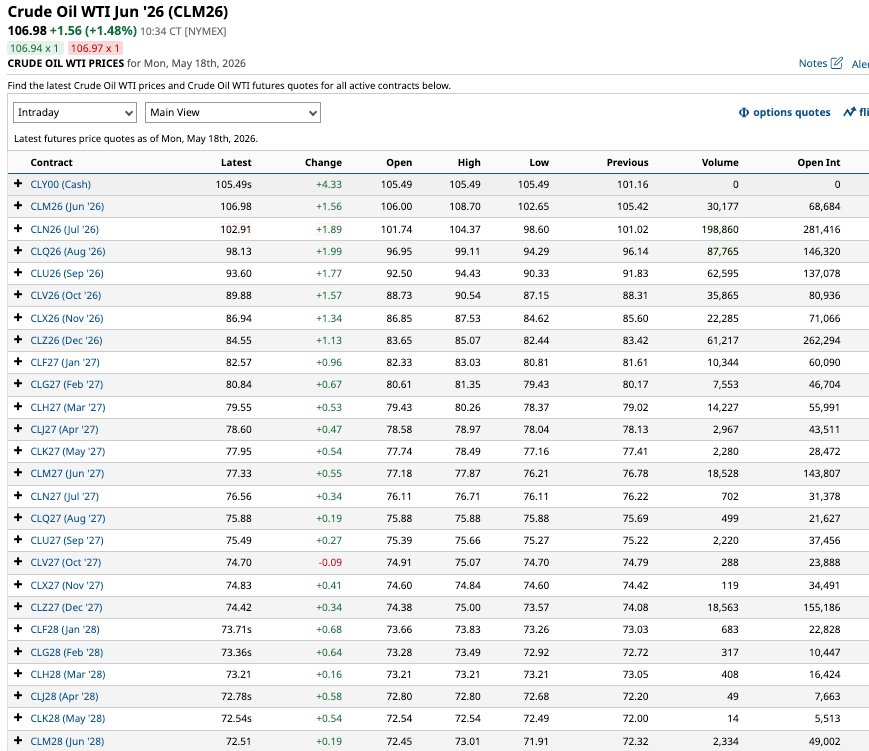

The forward curve shows that NYMEX WTI crude oil for June 2026 delivery is trading at a $20.65 premium to June 2027 delivery and a $34.47 premium to June 2028 delivery.

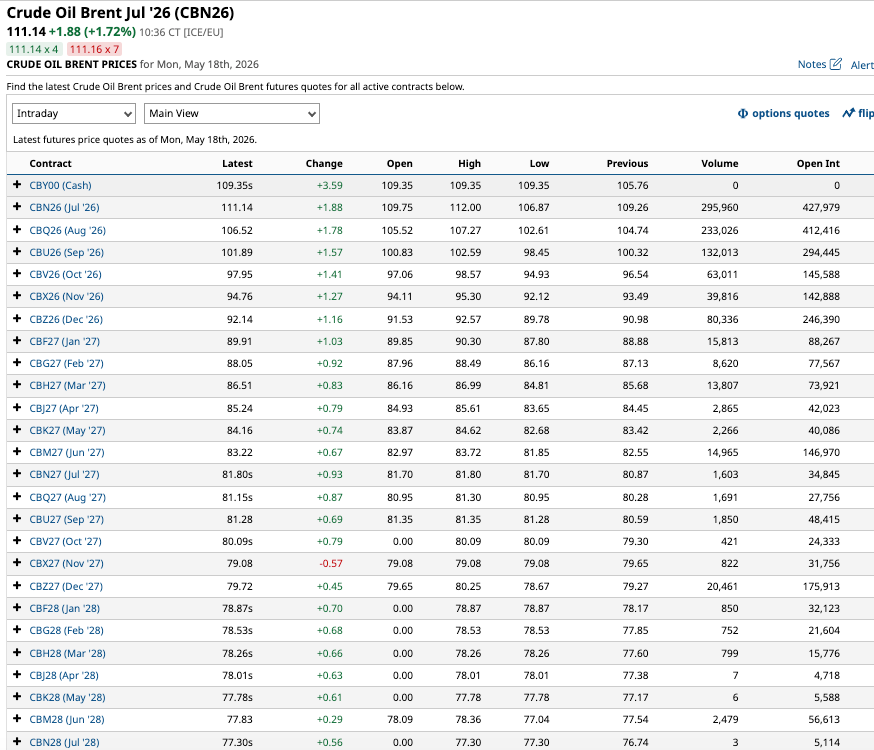

The forward curve shows that ICE Brent crude oil for July 2026 delivery was at a $29.34 premium to July 2027 delivery and a $33.84 premium to July 2028 delivery.

Both WTI and Brent futures are in steep backwardation due to events in the Middle East that are affecting petroleum flows through the Strait of Hormuz.

Backwardation favors the longs

Speculators tend to trade nearby or active-month commodity futures due to their higher open interest and volume, which increases liquidity. Investors and speculators who are long crude oil futures and rolling their risk positions to the next active month are benefiting from backwardation, as they sell the nearby contract to close the existing position at a premium and replace it with the next active month at a discount. The July-August Brent spread traded over $4.60 per barrel on May 18, while the WTI June-July spread traded over $4.00 per barrel. The longer backwardation persists, the more those rolling long positions will profit from selling the nearby and buying the next active month, making the long position a cash machine even if crude oil prices remain around current levels of $100 per barrel. If prices spike higher amid heightened Middle Eastern hostilities, the nearby WTI and Brent contracts will likely rally the most, benefiting long positions. The risk is that a sudden price plunge would result in losses on the long positions. Meanwhile, falling oil prices will likely cause backwardation to decline or shift to contango, a condition in which deferred prices are higher than nearby prices, indicating an oversupply in the oil market.

Backwardation tells us something about market sentiment

The current backwardation in WTI and Brent crude oil futures tells us a few things about market sentiment:

- Backwardation signals tight nearby supplies.

- Lower long-term prices signal that the market expects higher nearby prices to lead to increased production.

- Backwardation could signal that producers are hedging long-term output.

- Since most activity occurs in nearby futures contracts, backwardation signals bullish sentiment, as speculators and investors buy nearby crude oil futures.

For bulls who hold nearby long positions, there is beauty in backwardation. When markets shift into contango, it can be a curse for those with long positions, as they have to pay to roll rather than receive a premium. For hedgers, the opposite is true: backwardation involves a cost of rolling short positions, while contango can result in a credit.

Some signs point lower, but it could be a rocky road ahead

The following factors support lower WTI and Brent crude oil prices over the coming months and years:

- Backwardation signals that the current high prices will foster increased production, weighing on prices over the coming months.

- While Iran and the U.S. remain far apart on issues that would end the conflict, rising oil prices are having a global impact, prompting countries worldwide to become involved in efforts to reopen the Strait of Hormuz.

- The U.S. is energy-independent and could ramp up its petroleum output to increase exports and relieve some of the pressure created by the Middle Eastern conflict.

- An end to the conflict that removes some of the Middle Eastern risk factors could send crude oil prices appreciably lower.

While these factors favor an eventual decline in crude oil prices, the risk of sudden spikes remains high in May 2026. If the U.S. destroys Iranian oil production and refining infrastructure, and Iran retaliates by doing the same to its neighbors in the region, oil prices could spike to record highs, with many analysts forecasting a worst-case scenario of $200 per barrel or higher. In that case, expect the backwardation to widen significantly.

The bottom line is that we should expect lots of volatility in crude oil prices over the coming weeks and months. While the short-term path of least resistance is uncertain, with the potential for a spike or a plunge, the forward curve suggests crude oil prices are most likely to fall over the long term.

Crude oil could reach a new high, but that would only encourage increased production and alternative logistical routes to the Strait of Hormuz and other passages impacted by Iran and its proxies.

On the date of publication, Andrew Hecht did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)