Since May 2021, the S&P 500 has delivered a total return of 79.9%. But one standout stock has more than doubled the market - over the past five years, BNY has surged 169% to $136.58 per share. Its momentum hasn’t stopped as it’s also gained 27% in the last six months thanks to its solid quarterly results, beating the S&P by 15.5%.

Is now the time to buy BNY, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is BNY Not Exciting?

We’re happy investors have made money, but we're swiping left on BNY for now. Here are three reasons there are better opportunities than BK and a stock we'd rather own.

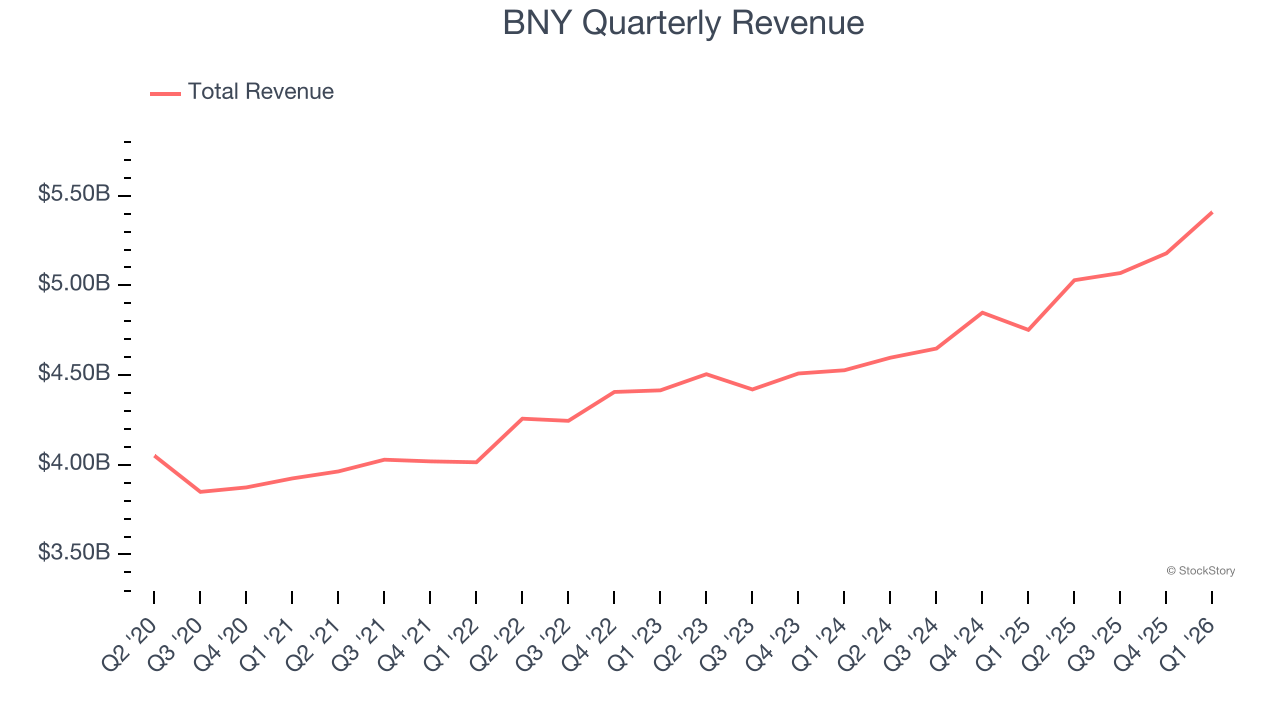

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

Regrettably, BNY’s revenue grew at a tepid 5.7% compounded annual growth rate over the last five years. This was below our standard for the financials sector.

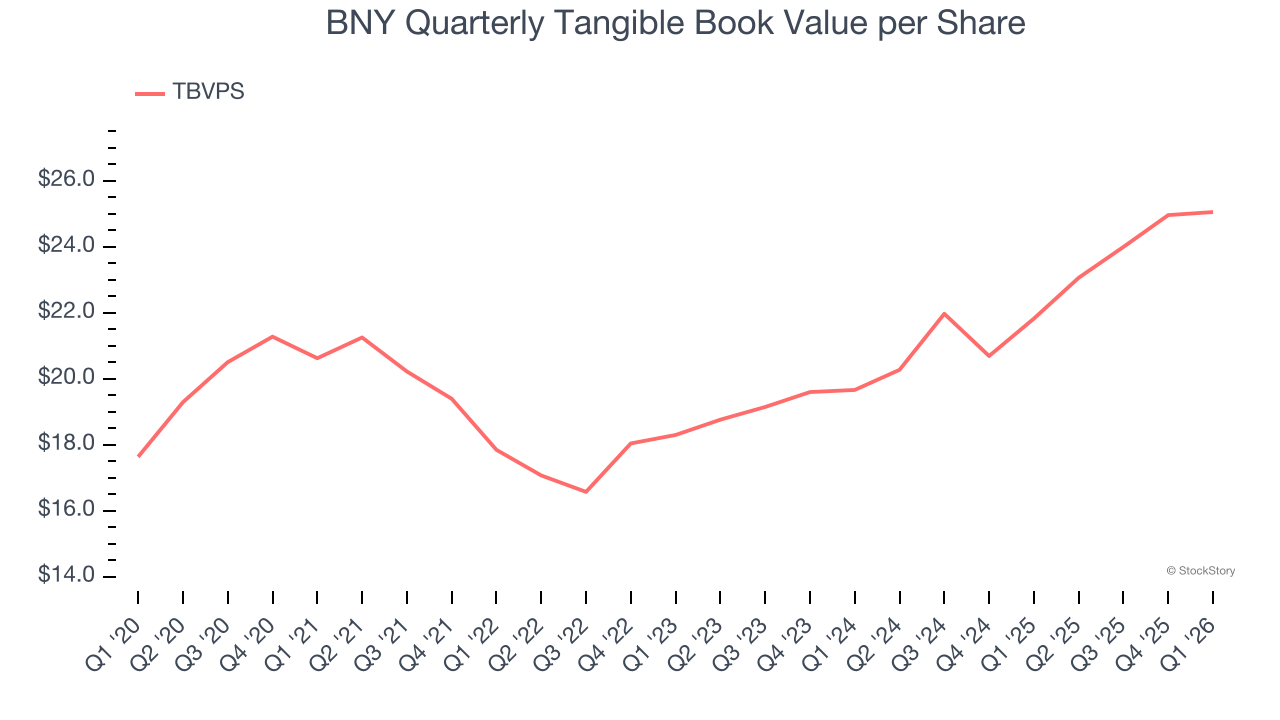

2. Growing TBVPS Reflects Strong Asset Base

We consider tangible book value per share (TBVPS) an important metric for financial firms. TBVPS represents the real, liquid net worth per share of a company, excluding intangible assets that have debatable value upon liquidation.

Although BNY’s TBVPS increased by a meager 4% annually over the last five years, the good news is that its growth has recently accelerated as TBVPS grew at an impressive 12.9% annual clip over the past two years (from $19.66 to $25.06 per share).

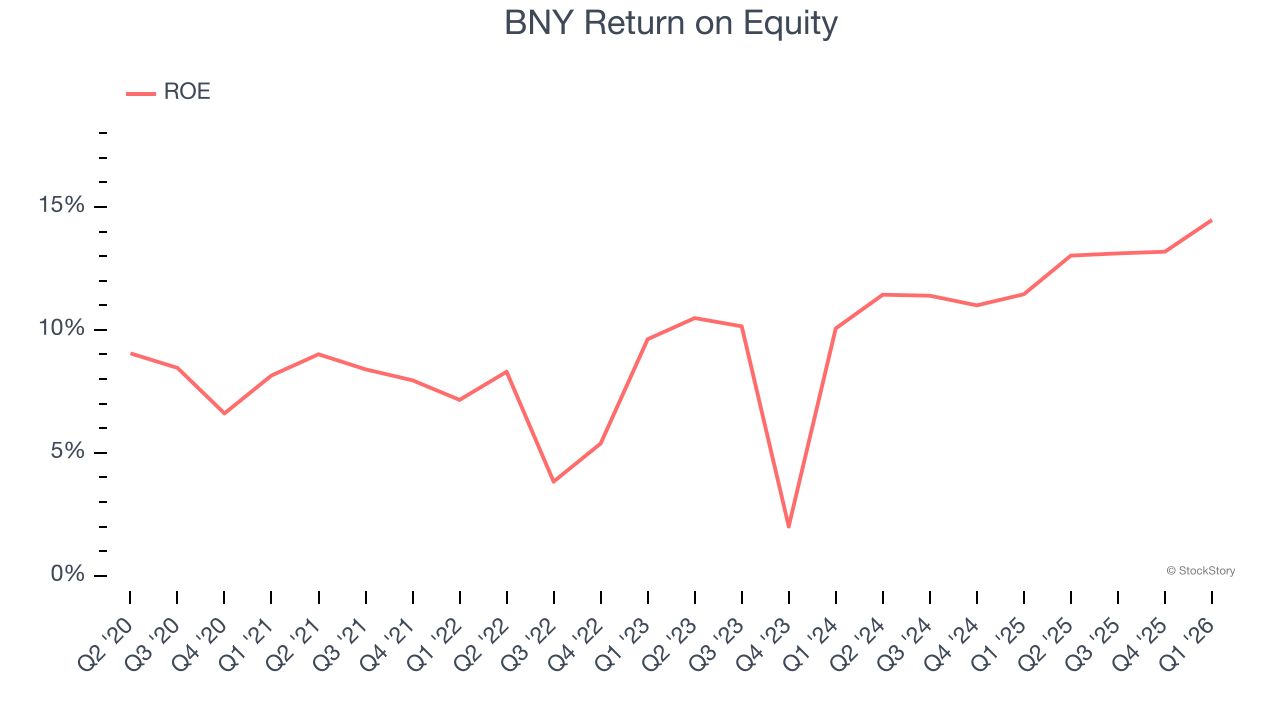

3. Previous Growth Initiatives Haven’t Impressed

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, BNY has averaged an ROE of 9.6%, uninspiring for a company operating in a sector where the average shakes out around 10%.

Final Judgment

BNY isn’t a terrible business, but it doesn’t pass our quality test. With its shares topping the market in recent months, the stock trades at 15.4× forward P/E (or $136.58 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're pretty confident there are superior stocks to buy right now. We’d suggest looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Like More Than BNY

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

/An%20Intel%20sign%20out%20front%20of%20a%20corporate%20office%20by%20wolterke%20via%20Adobe%20Stock.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)