/Cisco%20Systems%2C%20Inc_%20HQ-by%20Sundry%20Photography%20via%20iStock.jpg)

Cisco Systems (CSCO) reported lower free cash flow compared to last year, as well as lower FCF margins. Nevertheless, CSCO's fair value could be 16% higher based on significantly higher revenue forecasts. Value buyers are shorting near-term CSCO puts to set a lower buy-in price and shorting covered calls in case it stays flat or rises slightly.

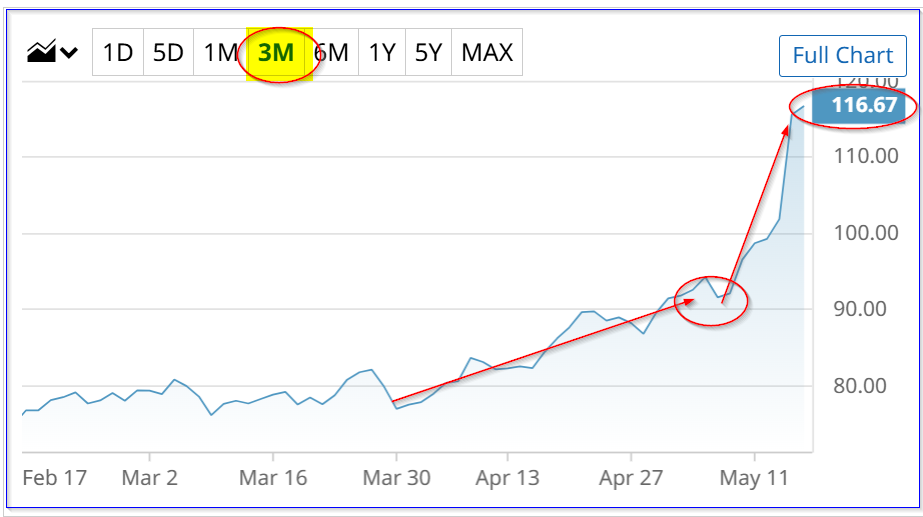

CSCO was up over 1.4% on Friday, May 15, at $117.59 in midday trading. That is a peak price, so value investors are looking for a lower entry point. One way to do this is to short out-of-the-money (OTM) puts and calls. This article will show how to do this.

Lower Cash Flow in Fiscal Q3

Cisco Systems, the internet security software and hardware company benefiting from sales to AI hyperscalers, reported that its fiscal Q3 revenue (ending April 25) rose +12% YoY, and for the 9 months was up +9.75%.

Most of that was from hardware and product sales, which still represent $12.1 billion of its $15.8 in quarterly sales, or 76%. Its services revenue actually fell for the quarter.

That could be one reason why both its operating cash flow (OCF) and free cash flow (FCF) were lower, as were related margins (i.e., percent of revenue).

For example, its Q3 OCF was down from $4.057 billion last year to $3.757 billion this year, according to data from Stock Analysis. On top of this, capex rose from $261 million to $414 million. In addition, the trailing 12-month (TTM) OCF was off 4.85% to $13.025 billion.

As a result, its Q3 free cash flow (FCF) fell 12% from $3.796 billion to $3.343 billion in Q3. And its TTM FCF dropped to 7.9% to $11.788 billion.

This implies that its Q2 and TTM FCF margins have fallen. For example, its Q3 margin fell from 26.83% last year to 21.1%. Moreover, its TTM margin was 19.4%, down from 23.0%.

Nevertheless, analysts project significantly higher revenue next fiscal year ending July 31, 2027. That could lead to higher FCF. This may be why CSCO stock is still rising.

Higher Cisco Systems FCF Forecasts

For example, 23 analysts surveyed by Seeking Alpha have an average revenue projection of $68.05 billion, up +8.2% over FY 2026 forecasts.

That implies that, using a 20.25% FCF margin (i.e., the average of its Q3 and TTM FCF margins - see above), FCF could be higher:

$68.05 billion x 0.2025 = $13.78 billion FCF

That's $1.99 billion higher than its TTM figure of $11.788 billion (i.e., +16.9%). This implies that CSCO stock could be worth significantly more.

CSCO Price Targets

One way to value a tech stock like this is to look at its FCF yield. That assumes that 100% of free cash flow is paid out to shareholders. As it stands, CSCO is paying out 87% of its FCF, in both dividends and buybacks, according to page 5 of its presentation deck.

So, for example, its $11.788 billion in TTM FCF represents a FCF yield of 2.55% (i.e., using the Yahoo! Finance calculation of its market cap today):

$11.788 billion TTM FCF / $462.3 billion mkt cap = 0.0255 = 2.55% FCF yield

Therefore, using our FCF forecast of $13.78 billion in FCF next year, Cisco's fair market value could rise to over $540 billion:

$13.78b FCF 2027 / 0.0255 = $540.4 billion market value

That is 16.89% higher than the $462.3 billion market cap today. In other words, CSCO stock could be worth 16.89% more:

$117.59 x 1.1689 = $137.45 per share target price (TP)

This is higher than other analysts' PTs. For example, Yahoo! Finance reports that the average of 26 analysts is $117.95, and Barchart's mean survey PT is $89.24. However, AnaChart.com, which tracks recent analyst recommendations, shows that 16 analysts have an average PT of $128.44 (i.e., +9.5% higher).

So, analysts disagree whether CSCO stock is at a peak. One way to avoid this issue is to set a lower price target by shorting near-term puts in lower strike prices, as well as shorting covered calls.

Shorting OTM CSCO Puts and Calls

This play allows an investor to earn income by selling out-of-the-money (OTM) puts and calls. Shorting OTM puts allows an investor to potentially buy in at a lower price if CSCO falls, and selling OTM calls gives existing investors extra income if CSCO stays flat or rises slightly.

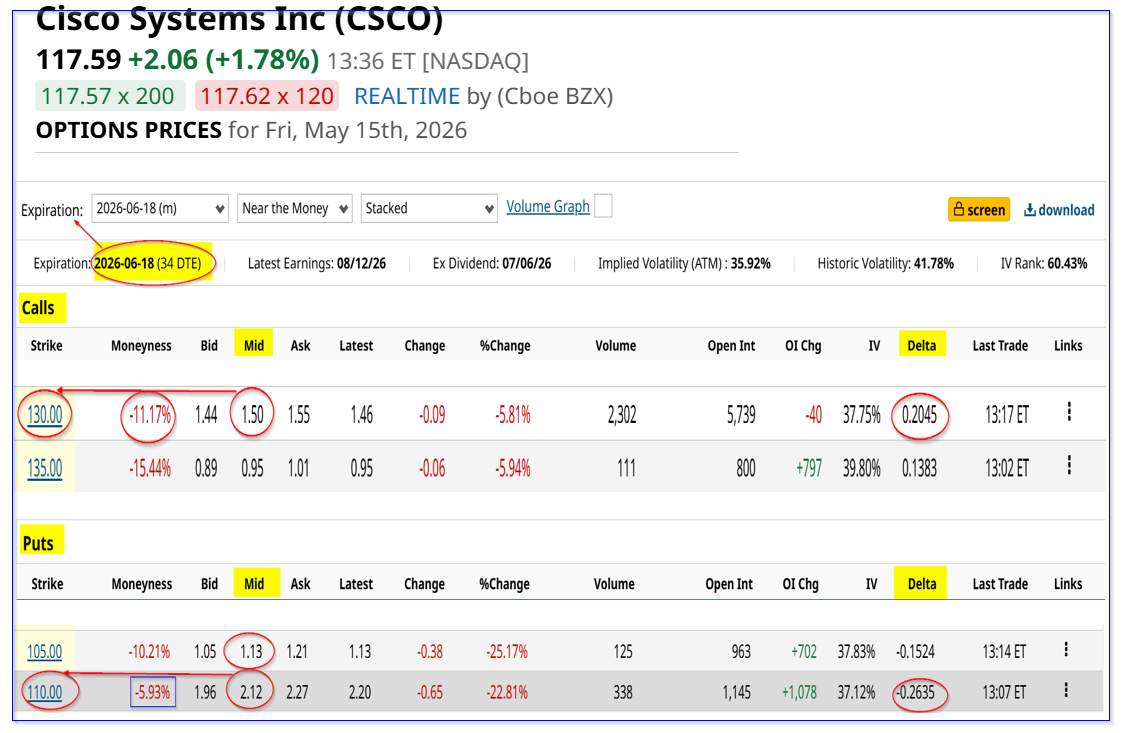

For example, look at the June 18 expiry period, 34 days from now. It shows that the $130 call option has a midpoint premium of $1.50. That provides a 1.3% yield (i.e., $1.50/$117.59) for an investor, along with potential upside if CSCO rises over 11% to $130.

In addition, the $110.00 put option contract has a higher premium of $2.12 for 6% lower strike price. That would provide an investor with the following income:

$212 / $11,000 collateral = 1.93% one-month yield

However, note that the put option play delta ratio is slightly higher than the call option (i.e., 26% vs 20.5%). This implies a slightly higher chance that CSCO will drop to the put option strike price than rise to the higher call option price.

Nevertheless, an investor can choose to do either one of these trades, or even both (with twice as much investment capital).

The bottom line is that these are two plays that value investors can make to play CSCO Systems stock. CSCO still looks undervalued here for the long term, but these short-term plays are a way to take advantage of any near-term weakness in CSCO stock.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)