/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

Tech and DevOps stocks have been jittery as AI hype meets cost cutting. Most recently, all-remote DevSecOps platform GitLab (GTLB) drew attention with a big restructuring. On May 11, CEO Bill Staples announced an “agentic AI” overhaul, flattening management, splitting R&D into roughly 60 teams, and automating workflows with AI agents. Staples set a voluntary separation window to “right-size” roles by June 1.

GitLab said that it is cutting jobs and reshaping the business around the agentic AI era. Raymond James answered the move by downgrading GTLB stock to “Market Perform” from “Outperform," digesting the "letter to employees […] outlining an intent for major internal changes in an effort to move GitLab to its second act as a public company.”

Shares fell about about 10% on May 12 in reaction to the news. Here's what investors should know.

Why This Matters for GitLab

GitLab is not some tiny niche name. It is the intelligent orchestration platform for DevSecOps, which means it sits in the workflow where companies build, test, secure, and ship software. The bigger story now is GitLab Duo Agent Platform, the company’s push into AI tools that help automate more of that work. Management says that is the future. Investors are just asking how much pain comes with that future.

GitLab’s strategy this year has centered on AI partnerships. In April, the firm rolled out support for Anthropic’s Claude models in its Duo Agent Platform, and deepened ties with cloud providers. In the first quarter, GitLab also launched a $400 million share buyback, signaling management’s confidence in the core business. However, the internal upheaval is tangible. The headcount cuts and reorganization are large changes, and the company will reveal the final cost savings and restructuring impact on the June earnings call.

The Stock Performance Has Been Ugly

GTLB stock has already taken a beating this year. Shares are down more than 57% over the past 52 weeks. Barchart data also shows the stock is still below its 100-day and 200-day moving averages, even though it sits near its 50-day line. That tells you GTLB stock has had some recent bounce, but the longer trend is still weak. Year-to-date (YTD), shares are down about 40%.

GitLab does not look outrageously cheap, but it also does not look like a high-flying software stock anymore. The company’s market capitalization is about $3.75 billion against trailing revenue of $955.2 million, which puts it at just under 4 times sales. Its forward earnings valuation is about 30 times. That feels more like a fairly valued or slightly expensive software name than a bargain, especially with growth now slowing from its earlier pace.

What Happened With the Layoffs

The layoff story is the real pressure point here. GitLab said it is restructuring to fit the agentic era, and the memo described a big organizational reset. The company plans to flatten management, move work into smaller teams, and use AI agents inside internal workflows.

That may sound efficient on paper, but Wall Street does not love uncertainty, and this kind of overhaul creates execution risk fast. It also raises questions about morale and whether the company could lose talent while trying to rebuild itself.

GitLab’s Latest Quarter Was Solid

The good news is that GitLab’s latest earnings report was not a disaster. Full-year fiscal 2026 revenue climbed 26% YOY to $955.2 million. In the fiscal fourth quarter of 2026, revenue rose 23% year-over-year (YOY) to $260.4 million. Most of that came from subscription revenue, which totaled $234.3 million in the quarter, while license revenue added $26.1 million. That is a clean reminder that this is still a real growth company, not a broken one.

Profitability also moved in the right direction. Net income flipped to a $2.6 million loss from a $6.9 million profit a year ago, but non-GAAP EPS still came in at $0.30, down only a bit from $0.33 the same time last year.

For the full year, operating cash flow reached $232.9 million, and adjusted free cash flow hit $219.6 million. GitLab also ended the quarter with $229.6 million in cash and cash equivalents, plus $1.03 billion in short-term investments.

CEO Bill Staples said GitLab sits at the heart of how enterprises build and deliver software. Meanwhile, CFO Jessica Ross noted that fiscal 2026 saw the company cross $1 billion in annual recurring revenue (ARR) and deliver $220 million in free cash flow.

Those are strong numbers, but they do not erase the fact that growth is now slowing from a much hotter phase. GitLab guided fiscal 2027 revenue between $1.099 billion and $1.118 billion and non-GAAP EPS of $0.76 to $0.80.

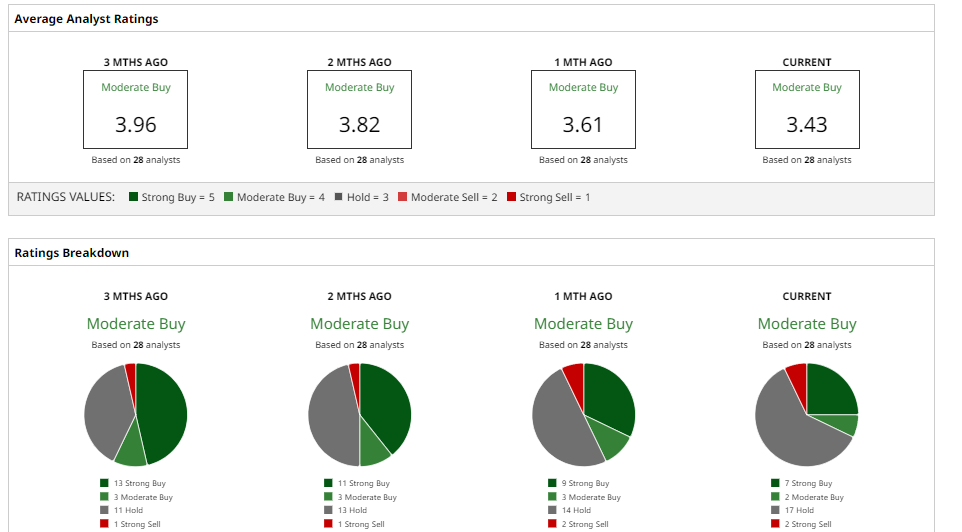

What Do Analysts Think About GitLab Stock?

At the moment, Wall Street is playing by Wall Street's own rules with GitLab. GTLB stock currently has a consensus “Hold” rating, and an average price target of $31.96. That implies potential upside of approximately 42% from the current levels.

However, a number of analysts have lowered their forecasts over the past several weeks. Bank of America recently lowered its price target to $27 and cut its rating to “Neutral.” Both Morgan Stanley and RBC reduced their price targets as well, with Morgan Stanley down to $29 and RBC down to $25 per share.

Even though GitLab has had a few early successes, the company still has a far bigger enterprise to build and steady-to-beat revenue growth. However, investors are concerned that this transition to AI and job cuts may lead to more issues in the short term. Strength of execution is required before analysts become uber bullish on GTLB stock again.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)