Shares of Marvell Technology (MRVL) have more than doubled this year as accelerating investment in artificial intelligence (AI) infrastructure is driving strong demand for its products. But after such a massive rally, can Marvell still move higher?

So far, the company’s performance and solid outlook suggest the AI boom is far from over. The semiconductor company is seeing explosive demand across its data center business, driven by rising adoption of AI workloads that require faster networking, advanced connectivity, and high-performance storage infrastructure. As hyperscalers and cloud giants race to expand AI capacity, demand for Marvell’s interconnect, switching, and storage solutions continues to accelerate.

One of the emerging growth drivers for Marvell is its custom AI chip business. The segment delivered a major breakout in fiscal 2026, with revenue roughly doubling year-over-year. That surge reflects a broader industry shift with big tech companies increasingly seeking custom-built silicon optimized for their own AI models and cloud platforms.

Moreover, management’s bullish outlook suggests momentum remains strong heading into the rest of the fiscal year, particularly as AI infrastructure spending continues to scale globally. Still, after such a strong rally, valuation concerns are beginning to surface.

With this backdrop, is Marvell stock still worth buying?

Marvell’s AI-Fueled Growth Story Is Just Beginning

Marvell Technology has emerged as one of the biggest beneficiaries of the AI infrastructure boom, and its growth trajectory appears to be accelerating. The company closed fiscal 2026 with solid fourth-quarter revenue of $2.22 billion, up 7% sequentially.

Management expects fiscal Q1 2027 revenue to climb another 8% sequentially to roughly $2.4 billion, driven by surging AI-related demand from hyperscale cloud providers and large technology companies. Even more importantly, Marvell expects revenue growth to remain strong throughout the entire year, with its top line registering a solid sequential increase.

Based on current guidance, Marvell’s revenue could rise more than 30% year-over-year in fiscal 2027 and hit $11 billion.

The demand drivers are powerful. Cloud giants are pouring billions into AI data centers to support increasingly compute-intensive workloads, and Marvell is directly benefiting from that spending wave. The company says bookings continue to accelerate, particularly in its data center business. As a result, Marvell expects fiscal 2027 data center revenue to jump roughly 40% year-over-year.

Its interconnect segment is now projected to grow more than 50%. Meanwhile, Marvell’s communications and other end markets are expected to return to growth, with management forecasting roughly 10% revenue growth in fiscal 2027.

Looking ahead to fiscal 2028, management expects another year of robust expansion across its AI-focused businesses. Its interconnect business will continue growing rapidly. At the same time, its custom AI silicon business could at least double year-over-year, and its Ethernet switching business will ramp significantly as AI clusters scale.

Moreover, the company’s recent acquisitions of Celestial AI and XConn are also expected to contribute meaningfully to its growth. Altogether, Marvell could deliver 50% year-over-year growth in data center revenue in fiscal 2028.

Alongside solid top-line growth, Marvell is set to deliver strong earnings thanks to the operating leverage and better product mix.

Is Marvell Stock Still a Buy After Its Massive Rally?

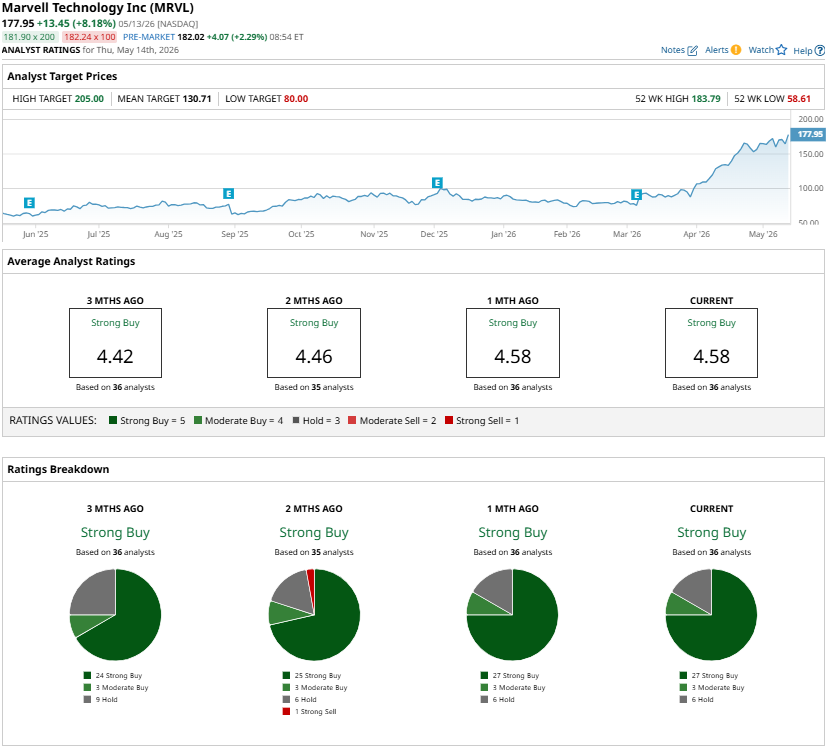

Marvell’s investment case remains strong. Demand for Marvell’s data center and custom AI chips continues to accelerate as hyperscalers ramp up spending on next-generation AI infrastructure. That momentum is expected to translate into significantly faster revenue growth over the next several quarters. Wall Street remains optimistic and rates MRVL stock a “Strong Buy.”

The company’s earnings outlook is equally impressive. Consensus estimates project earnings growth of roughly 41% in fiscal 2027, followed by a 48% jump the year after.

However, Marvell now trades at 56.2 times forward earnings, which is high and indicates that positives are priced in.

For long-term investors, Marvell remains one of the most compelling AI semiconductor plays on the market. However, waiting for a better entry point could offer a more favorable risk-reward setup.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Boeing%20Co_%20sign%20at%20airport-by%20sanfel%20via%20iStock.jpg)