/A%20Palantir%20sign%20displayed%20on%20an%20office%20building%20by%20Poetra_RH%20via%20Shutterstock.jpg)

When Palantir (PLTR) CEO Alex Karp recently met with Ukraine President Volodymyr Zelenskyy, they talked about AI. As the war between Ukraine and Russia continues, drones have become an essential part of the fight for both sides. So has AI, and Ukraine has decided to expand its AI prowess in the war by deepening its partnership with data analytics platform Palantir.

Reportedly, the talks between Karp and Zelenskyy revolved around how to use technology in regard to combat operations and civilian needs. That's pretty vague, and the company's post on X (formerly Twitter) also did not shed much light. "The deployment of Palantir’s software on the battlefield in Ukraine has helped defend the brave people of Ukraine against Russia’s aggression since 2022 — and it will define how the entire West fights and wins for decades," the company posted.

However, the Brave1 Dataroom collaboration between Palantir and Ukraine can give us an idea about the contours of their future partnership. Brave1 Dataroom made Ukrainian interceptor drones capable with AI, with the end goal of intercepting Russian drones. Reportedly, this has been a resounding success, with 33,000 Russian drones destroyed in March 2026 alone.

Yet, PLTR stock is still down 25% on a year-to-date (YTD) basis. Can an expanded partnership with Ukraine flip the multibagger's fortunes in 2026? Let's take a closer look.

Palantir's Perfect Q1

Palantir's report for the first quarter of 2026 did not deviate much from recent quarters. The Rule of 40 metric continued to be handily beaten by the company, along with revenue and earnings estimates.

Revenue of $1.63 billion marked growth of 85% year-over-year (YOY). While U.S. government revenue rose 84% YOY to $687 million, U.S. commercial revenue continued on its strong growth path with a 133% rise to $595 million. In fact, U.S. commercial remaining deal value, a key indicator of demand, more than doubled on a YOY basis to $4.92 billion. Notably, total contract value for the quarter stood at $2.41 billion, a rise of 61% from the prior year.

On the earnings front, EPS climbed to $0.33 per share. This was above the consensus estimate of $0.28, and also marked the ninth consecutive quarter of an earnings beat from the company.

Net cash from operations almost tripled from the prior year to $899.2 million, as Palantir exited Q1 2026 with a cash balance of $2.32 billion. Impressively, the company had no short-term debt on its books.

However, despite the share price decline, PLTR stock continues to trade at unsustainable levels. Its forward price-to-earnings (P/E) ratio of 115.3 times, price-to-sales (P/S) multiple of 72.6 times, and price-to-cash flow ratio of 196.9 times are all considerably higher than their respective sector medians.

Sovereign Opportunity

In a previous analysis of Palantir, I highlighted how the idea of the firm becoming irrelevant is ludicrous and unlikely. The recent news with Ukraine only strengthens the case for Palantir's longevity.

Palantir will certainly be targeting the AI software market for the defense and intelligence sector, which is projected to grow to $35 billion by 2035, driven by the acceleration of military modernization programs across Europe and Asia. The company, with its nearly two-decade track record in mission-critical analytics for governments, is arguably better positioned than any pure commercial software vendor to capture a portion of that spending.

Although Palantir has been slow to penetrate outside of the U.S., the increasing role of AI in the defense sector will certainly aid the company. Moreover, it's not that the firm has nothing to show for outside of the United States. Notably, since 2018, Palantir's revenue from the U.K. has grown by over 150%, and revenue from the rest of the world (excluding the U.K.) has surged by 229% over the same period. That is meaningful directional traction, though the absolute numbers still lag far behind the U.S. business. International government contracts are growing but remain largely in the early stages of multiyear deployment, which means revenue recognition tends to be back-weighted and lumpy.

Beyond the United Kingdom, the international picture is patchier but improving. NATO has formally awarded Palantir a contract to deploy its Maven Smart System for AI-enabled battlefield operations, a deal that covers all 32 NATO member states and could function as a powerful lead generation engine for individual country contracts as member governments evaluate the platform's capabilities. Germany, France, and the Nordic countries have also become focus areas, with Palantir working alongside public agencies and private-sector companies on challenges ranging from supply-chain operations to healthcare-data management. In Asia, the company has also expanded its partnership with HD Hyundai, signaling broader ambitions in industrial and manufacturing verticals across the region.

What Do Analysts Think of Palantir Stock?

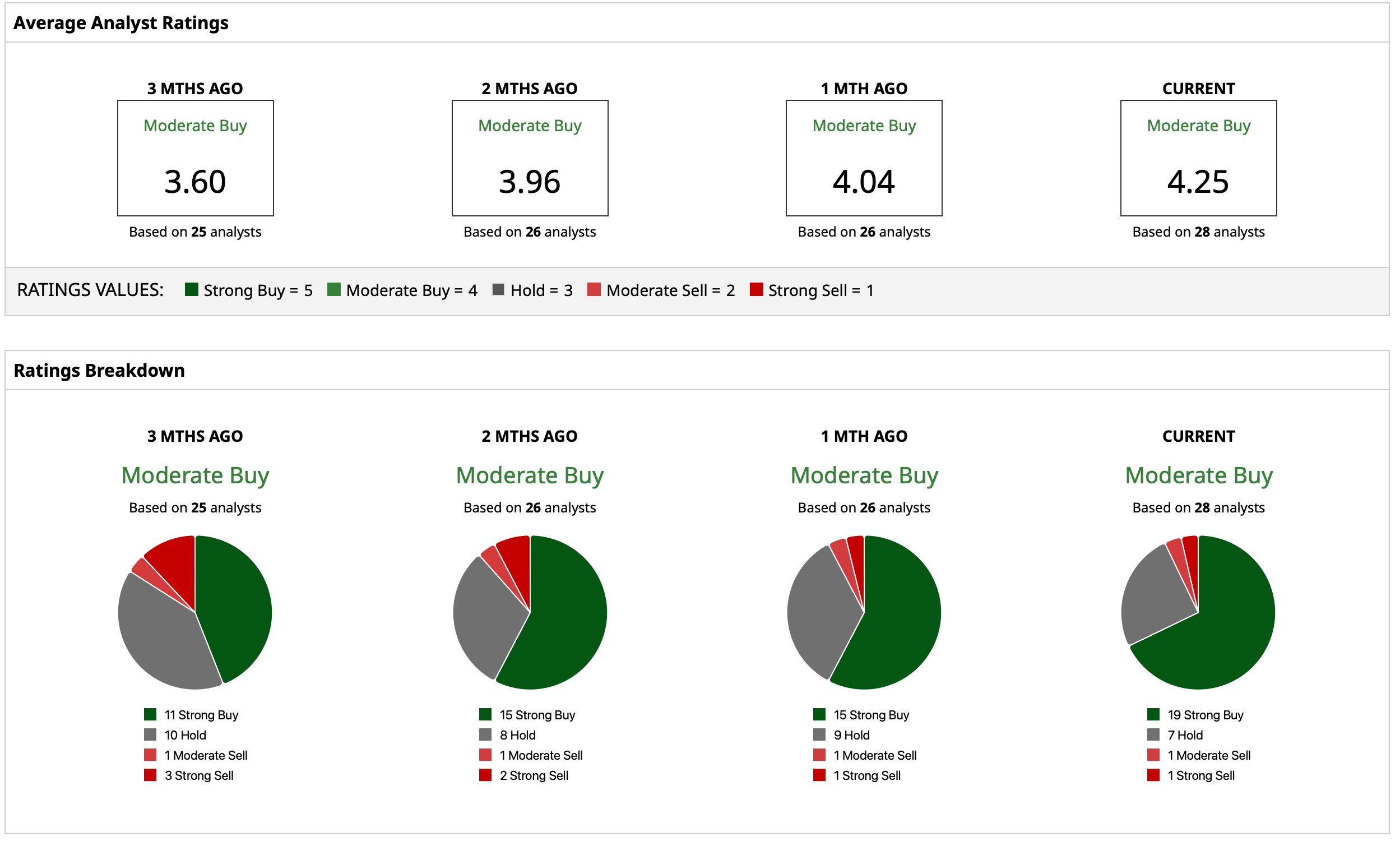

Overall, analysts have a consensus “Moderate Buy” rating for PLTR stock. The mean target price of $192.46 suggest potential upside of about 44% from current levels. Out of 28 analysts covering the stock, 19 have a “Strong Buy” rating, seven have a “Hold” rating, one has a “Moderate Sell” rating, and one has a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)