Poet Technologies (POET) shares ripped higher on Thursday after the semiconductor design firm announced a landmark commercial agreement with Lumilens.

This optical networking deal includes an initial purchase order worth $50 million and a framework that could scale to more than $500 million over five years.

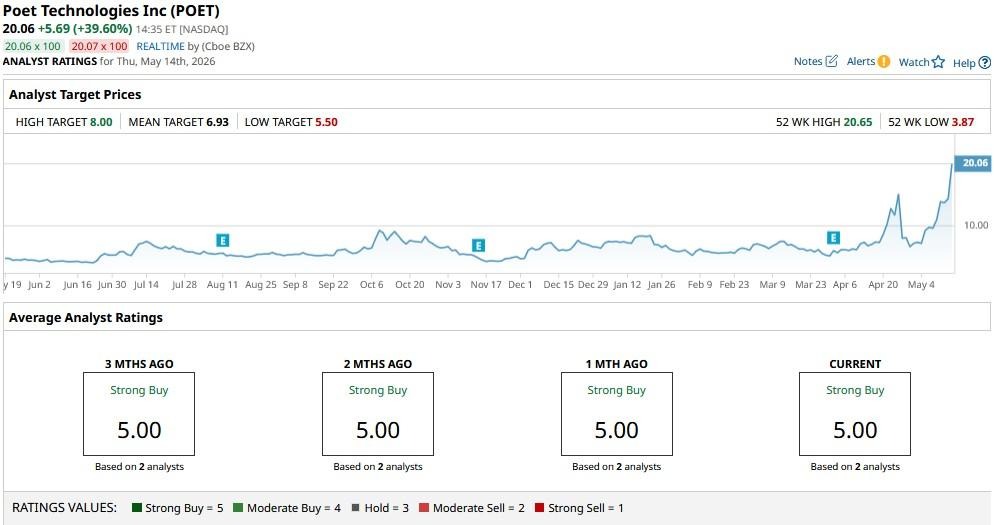

Including today’s gains, POET stock is trading at more than triple its price late April.

Why Lumilens Deal Isn’t Bullish for POET Stock

The Lumilens agreement may look transformational on the surface, but the “warrant structure” is actually a glaring red flag.

POET has granted Lumilens the right to purchase nearly 23 million of its shares at $8.25 only — an alarming discount to its current price of about $20.

That’s not a small incentive; it’s a deeply dilutive, value‑transfer mechanism that effectively hands Lumilens long‑term upside at shareholders’ expense.

If milestones are met, POET’s share count balloons. If they aren’t, it would signal weak demand.

Either way, the discount implies POET needed aggressive sweeteners to secure the deal, raising questions about bargaining power and underlying commercial strength.

Fundamentals Warrant Selling POET Shares

POET shares are unattractive also because the company remains deeply unprofitable, with limited recurring revenue.

Its balance sheet has historically relied on issuing new shares to fund operations, and yet POET is trading at a concerning four-digit sales multiple, pricing in flawless execution on a contract that’s largely conditional – not guaranteed.

Add in supply-chain dependencies and the long lead times typical in photonics commercialization, and the risk-reward skews unfavorably at current levels.

Even from a technical perspective, POET appears bound to sell off in the weeks ahead. Its relative strength index (RSI) has climbed into the mid-70s, indicating overbought conditions that often precede a sharp pullback.

What’s the Consensus Rating on Poet Technologies

Investors should also note that Poet Technologies doesn’t currently receive broad Wall Street coverage either.

As of writing, only two analysts cover POET stock, and while their consensus rating sits at “Strong Buy,” the mean price target of roughly $7 signals massive downside potential from current levels.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Alphabet%20Inc_%20and%20Google%20logos%20by%20IgorGolovinov%20via%20Shutterstock.jpg)

/Technological%20process%20of%20soldering%20chip%20components%20on%20PCB%20board%20by%20I%20Viewfinder%20via%20Adobe%20Stock.jpeg)