/Super%20Micro%20Computer%20Inc%20logo%20on%20phone%20and%20stock%20data-by%20Poetra_RH%20via%20Shutterstock.jpg)

Super Micro Computer (SMCI) reported a 123% jump in revenue year-over-year (YOY) for fiscal Q3 2026, putting it among the fastest-growing AI infrastructure players right now. But even with that growth, the stock has spent much of 2026 under pressure as investors question its credibility.

On March 19, the U.S. Department of Justice charged three people linked to the company, including a co-founder and Senior VP, over an alleged $2.5 billion scheme involving restricted Nvidia AI chips shipped to China. The news wiped out 33.3% of the stock in a single day.

Since then, the company has been trying to win back trust, one quarter at a time. Investors responded after its Q3 results showed improvement, with the stock jumping nearly 25% on May 6, though it still sits 48.7% below its 52-week high of $62.36.

Then on May 11, just days after that rebound, Super Micro Computer named Vik Malyala as its new Chief Business Officer, promoting him from within. He previously led technology and AI efforts and ran EMEA operations, and brings nearly 30 years of experience. He will now focus on partnerships and business growth with major tech players. After losing a co-founder under legal scrutiny, choosing an insider for such a key role sends a clear message. But is that move enough to steady the stock?

Breaking Down the Numbers

Super Micro Computer makes servers and data center systems for cloud, enterprise, and AI-related workloads, with a focus on building customized hardware quickly for customers.

The stock has had a mixed run lately. Shares are down 16.98% over the past 12 months, but they are up 10.3% so far this year.

Also, SMCI trades at a forward price-to-earnings of 17.61 times, which is below the sector average of 24.20 times and suggests the stock is priced more cautiously than many of its peers.

In fiscal Q3 2026, net sales reached $10.2 billion. That was down from $12.7 billion in the previous quarter, but up sharply from $4.6 billion a year earlier. Gross margin improved to 9.9% from 6.3% in Q2, while net income rose to $483 million from $401 million in the prior quarter and $109 million a year ago.

Diluted EPS came in at $0.72, while non-GAAP EPS was $0.84. One weaker spot was cash flow, with $6.6 billion used in operations during the quarter as the company spent heavily to support growth. For Q4, management expects revenue between $11 billion and $12.5 billion, and for full-year fiscal 2026, it sees sales reaching $38.9 billion to $40.4 billion.

The Engines Powering SMCI’s Expansion

Super Micro Computer recently added new Arm-based server platforms built on the Arm AGI CPU, along with new Open Compute Project (OCP) ORv3-compliant rack systems. That gives customers more choice in how they build out their infrastructure and strengthens Supermicro’s position as more than just a server maker.

The company says it now has more than 20 OCP-inspired systems, and its Data Center Building Block Solutions cover everything from GPUs and networking switches to full racks, site infrastructure, management software, and related services.

That broader lineup is also being backed by a much larger operating footprint. Supermicro Computer announced its biggest U.S. expansion yet with a new DCBBS campus near its San Jose headquarters. The site adds about 32.8 acres and more than 714,000 square feet, making it the company’s fourth Bay Area location and bringing its total regional footprint to nearly four million square feet. The facility is meant to handle system design, manufacturing, testing, service, and global distribution.

Furthermore, the company is pushing beyond traditional data center hardware and into edge systems. It introduced a new line of compact, energy-efficient platforms powered by AMD EPYC 4005 series processors for AI inferencing and other workloads in places with limited space and power. That includes three new edge AI systems aimed at retail, manufacturing, healthcare, and branch locations. The use cases include real-time analytics, loss prevention, frictionless checkout, and in-store analytics.

Analyst Sentiment and What It Signals for Investors

For the current quarter ending June 2026, analysts expect earnings of $0.59 per share, up from $0.31 a year ago, which is a 90.32% increase. For the next quarter ending September 2026, estimates are at $0.55 versus $0.26 last year, showing projected growth of 111.54%. For full-year fiscal 2026, earnings are expected to come in at $2.12, compared to $1.72 last year, a growth rate of 23.26%.

On April 16, J.P. Morgan’s Samik Chatterjee kept a “Hold” rating and cut his price target to $28 from $40, pointing to concerns around execution and consistency. On the other hand, Rosenblatt Securities raised its target to $40 after gross margin improved to 10.1% from 6.4% in the prior quarter. The firm sees areas like Direct Liquid Cooling and the company’s AI infrastructure products as key drivers of future profits.

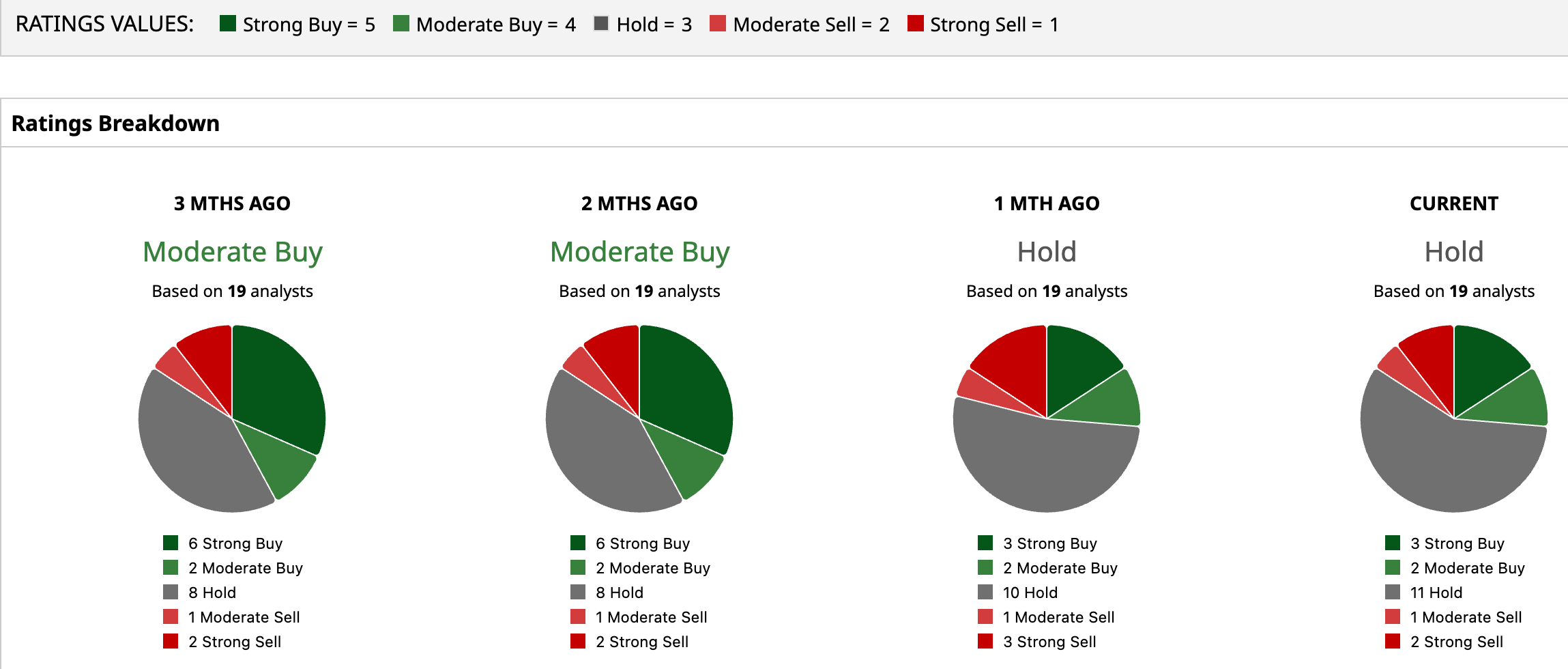

All 19 analysts covering the stock rate it a consensus “Hold”, and the average price target of $35.73 suggests 11.4% upside from current price levels.

Conclusion

The promotion of a chief business officer from within looks less like a short-term catalyst and more like a stabilizing move at a time when Super Micro needs tighter execution and clearer leadership signals. The company is still delivering strong growth and expanding aggressively across AI infrastructure, but investor confidence has not fully recovered, which is reflected in the cautious “Hold” consensus. This move helps reinforce continuity, but it does not eliminate execution risk. In the near term, the stock likely trades sideways with a slight upward bias, and a sustained move higher will depend on consistent margins, cleaner operations, and solid follow-through in upcoming earnings.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)