/Super%20Micro%20Computer%20Inc%20logo%20on%20phone%20and%20stock%20data-by%20Poetra_RH%20via%20Shutterstock.jpg)

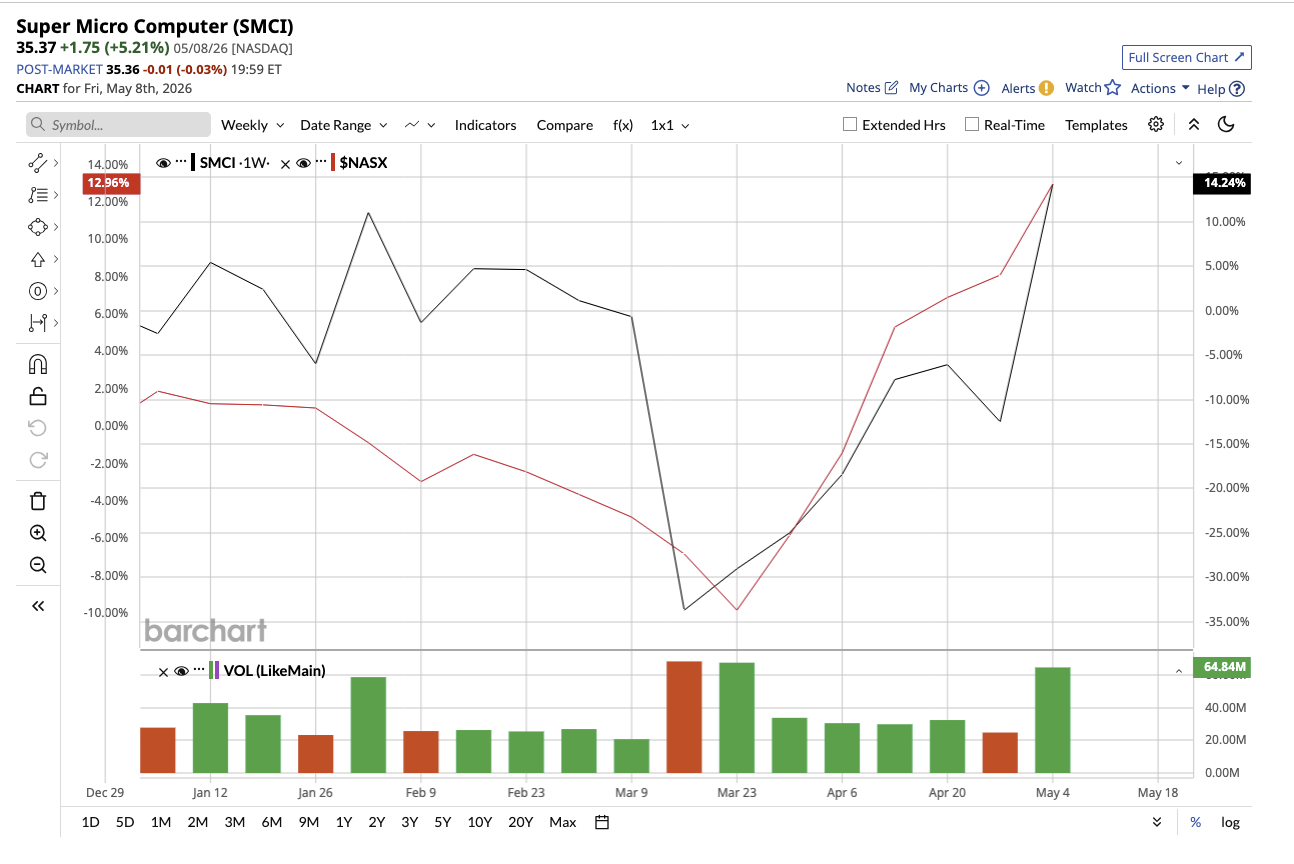

Super Micro Computer (SMCI) has endured a volatile period driven by accounting concerns, regulatory scrutiny, canceled contracts, and controversy surrounding former employees. But with its Q1 print on May 5, SMCI finally gave investors a reason to focus on its business rather than the headlines. Investors cheered the Q1 report which showed improving margins, strong AI infrastructure demand, and rapidly growing software and enterprise businesses. While the stock is up just 14% year to date, Q1 results sent the stock soaring nearly 25% on a single day.

Let’s examine two reasons that says SMCI’s long-term story is improving and one problem that could put pressure on the stock.

Reason No. 1: SMCI Is Moving Beyond Servers Into Full AI Infrastructure

One of the key highlights of the quarter was Super Micro’s expansion from a server manufacturer into a full AI data center infrastructure provider. During the Q3 earnings call, CEO Charles Liang repeatedly emphasized the company’s growing Data Center Building Block Solutions business (DCBBS). This segment includes direct liquid cooling systems, networking, power shelves, battery backup systems, management software, deployment services, and other artificial intelligence (AI) factory infrastructure products.

The company is aggressively expanding production capacity in Taiwan, Malaysia, and Silicon Valley, where it recently announced a new DCBBS campus that will increase its Bay Area footprint to nearly 4 million square feet. The company anticipates this segment to eventually contribute more than 25% of the company’s total profit within the next few years.

Additionally, the software side of this transformation is equally growing stronger with the SuperCloud Composer platform gaining traction. However, its AI GPU-related platforms continue to dominate, accounting for more than 80% of overall revenue, indicating that demand for AI infrastructure remains exceptionally high despite deployment delays. By offering software subscriptions and services alongside hardware, Super Micro Computer is aiming to build stronger recurring revenue streams and improve long-term profitability. In the third quarter, total revenue increased 123% year over year (YOY) to $10.2 billion. However, it dipped 19% sequentially due to customer site readiness delays and ongoing supply constraints.

Reason No. 2: Gross Margins Finally Rebounded

After several quarters of pressure, one encouraging sign for investors was improvement in profitability Adjusted gross margin rebounded to 10.1%, up from 6.4% in the previous quarter, and from 9.7% in the year-ago quarter. Adjusted earnings per share (EPS) also increased 171% YOY to $0.84 per share. Management credited this improvement to a better product mix, lower tariff and expediting costs, increased operational efficiency, and greater exposure to enterprise customers and higher-value infrastructure solutions.

Investors applauded the improvement, since one of the main concerns has been whether SMCI was compromising profitability to gain market share. However, management assured that the company can maintain a double-digit gross margin model over time as its business mix evolves toward enterprise infrastructure, software, and services. Notably, enterprise channel revenue reached $2.8 billion, accounting for 28% of overall sales and increasing by 46% YOY. Analysts expect revenue to increase by 83% in fiscal 2026, accompanied by 29% increase in earnings.

The One Big Risk

Despite its strong AI demand environment, SMCI’s balance sheet and cash flow pressures remain a risk that investors should not overlook. The company reported negative operating cash flow of $6.6 billion along with negative free cash flow of $6.7 billion as inventory levels and working capital requirements increased. Inventory increased to $11.1 billion from $10.6 billion in the prior quarter. The company’s cash conversion cycle also deteriorated sharply, rising from 54 days to 106 days quarter-over-quarter.

Negative operating cash flow means its core business isn’t generating enough cash to cover its day-to-day operations. And negative FCF implies that the company has nothing left after paying for operations. For a fast-growing company like SMCI, this will lead to the company borrowing debt, which is exactly what happened. Super Micro ended the quarter with $1.3 billion in cash but $8.8 billion in bank and convertible note debt. This resulted in a net debt position of $7.5 billion, over just $787 million in the prior quarter. While management believes these pressures are temporary, investors should keep an eye on whether the company can convert its enormous AI demand backlog into healthier and more stable cash generation.

Is SMCI a Buy Now?

Despite all the scandals, Super Micro’s Q1 showed meaningful progress in areas investors were most worried about, particularly margins, enterprise expansion, and recurring software and infrastructure revenue. However, the balance sheet risk remains substantial. For aggressive investors who believe AI infrastructure spending will continue to grow over the next several years, SMCI is a compelling long-term buy-and-hold stock. But conservative investors might want to see signs of improving cash flow stability before buying.

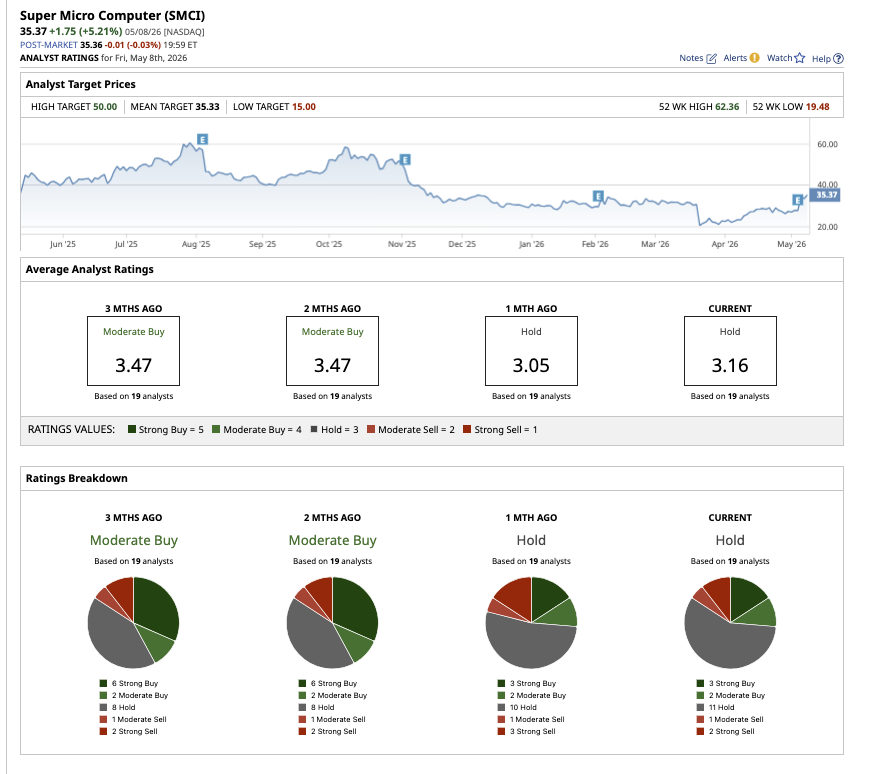

Wall Street also has a cautiously optimistic stance on SMCI stock rating it an overall “Hold.” Of the 19 analysts who cover the stock, three rate it a “Strong Buy,” two say it is a “Moderate Buy,” 11 rate it a “Hold,” one says it is a “Moderate Sell,” and two say it is a “Strong Sell.” The stock is trading above its average target price. But, the Street-high estimate of $50 suggests a potential 41.4% jump over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)