Across Wall Street and the broader tech sector, AI-driven restructuring is starting to look less like a trend and more like a survival strategy. Companies are cutting thousands of jobs as executives race to redirect spending toward AI, automation, and leaner operations. But for some businesses, AI is not just changing operations but also beginning to threaten the very services they sell.

That pressure is now hitting ZoomInfo Technologies (GTM) hard. The company, best known for helping sales and marketing teams find business contacts and identify potential customers through massive internet-sourced databases, announced plans to eliminate 600 jobs, roughly 20% of its workforce. Reports also suggest the company is shutting its research office in Israel, where nearly half of those cuts could take place.

The layoffs arrived alongside disappointing first-quarter 2026 results that rattled investors. ZoomInfo reported flat revenue growth and lowered its full-year sales forecast by about $60 million, pointing to softer customer demand and intensifying competition from AI-powered platforms that can increasingly automate data gathering and sales prospecting at lower costs.

The company’s restructuring effort appears aimed at protecting profitability. Rather than chasing weakening revenue streams tied to its traditional sales-intelligence business, ZoomInfo is trying to streamline operations and preserve margins while repositioning itself around AI-driven services and automation.

Investors reacted sharply to the update, sending the stock plunging to its lowest level since the company’s 2020 IPO, as concerns mounted over whether AI will ultimately become more of a long-term threat than a growth opportunity for the business.

About ZoomInfo Stock

Founded in 2007 and headquartered in Vancouver, ZoomInfo Technologies provides cloud-based business intelligence and go-to-market solutions for sales, marketing, recruiting, and operations teams. Its platform offers company and contact data, workflow automation, lead scoring, and engagement tools designed to help businesses identify prospects and improve customer outreach.

Serving clients ranging from small businesses to global enterprises, ZoomInfo supports industries including software, telecommunications, financial services, manufacturing, and real estate. The software company has expanded its capabilities over the years through product innovation and strategic acquisitions. Its market capitalization currently stands at $1.84 billion.

When ZoomInfo Technologies made its Nasdaq debut in 2020, the market treated it like one of the hottest names in cloud software. The company priced its IPO at $21 per share, and the stock surged 62% on its first trading day to close at $34, giving ZoomInfo a valuation of roughly $13.4 billion as investors piled into high-growth subscription-based tech plays.

But the story has changed dramatically since then. Shares of ZoomInfo have now collapsed 88% from its early trading days. Zooming in to the one-year period, GTM stock has fallen 60.62% over the past 52 weeks, while 2026 has been even tougher, with shares down 60.08% year-to-date (YTD). The stock has also logged 25 fresh lows over the last year, reflecting persistent selling pressure.

The latest blow came after weak first-quarter results after the close on May 11, softer revenue guidance, and a major layoff announcement, sending shares down 32.78% in premarket trading, with heavy red trading volumes signaling panic-driven selling and deepening bearish sentiment around the stock.

After such a sharp selloff, GTM’s valuation is starting to look far less demanding than it once did. The stock is priced at 5.4 times forward adjusted earnings, below both the broader sector average and its own historical median. The market might already be pricing in a large chunk of the company’s slowing growth and AI-related risks.

ZoomInfo’s Mixed Q1 Numbers and Softer Guidance

ZoomInfo delivered a mixed first-quarter report on May 11, beating Wall Street’s expectations on top and bottom lines but also revealing the quick AI disruption in reshaping the company’s business model. Revenue rose 1.5% year-over-year (YOY) to $310 million, while adjusted EPS climbed 21.7% annually to $0.28. Adjusted operating income increased 8.7% annually to $109.7 million, with margins improving to 35%.

The company returned cash to shareholders, repurchasing 13.1 million shares during the quarter and ending Q1 with more than $1 billion still available under its buyback program. ZoomInfo closed the quarter with $175 million in cash and investments alongside $1.3 billion in gross debt, while unlevered free cash flow slipped 4% YOY to $120 million.

Management acknowledged that demand weakened sharply late in March and into April, especially among software customers. Founder and CEO Henry Schuck described growing “AI and agentic confusion” among clients, with companies struggling to decide which tools to build internally versus purchase externally.

AI is rapidly reshaping the way in which enterprise software is built and consumed, and ZoomInfo Technologies is now trying to adapt before that shift leaves its traditional business model behind. Management acknowledged that AI-driven workflows are putting pressure on the company’s long-standing seat-based pricing structure, as customers increasingly want flexible access to data across multiple AI platforms, applications, and internal systems rather than fixed software licenses.

To respond, ZoomInfo plans to launch a new hybrid pricing model in the third quarter. Instead of relying mainly on seat-based subscriptions, customers will be able to combine lower annual platform fees with prepaid consumption credits that can be used across the company’s data, insights, applications, and AI agents.

Founder and CEO Henry Schuck said the company’s long-term strategy is to make ZoomInfo’s go-to-market data accessible wherever sales and marketing work happens, including platforms such as OpenAI ChatGPT, Anthropic Claude, Perplexity AI, Microsoft (MSFT) Copilot, and Alphabet's (GOOGL) Gemini. That transition is already underway. Roughly one-third of ZoomInfo’s annual contract value now comes from non-seat-based products, and management wants that mix to move closer to 50-50 over the next two years. Its Operations and Data-as-a-Service segment grew over 20% annually.

ZoomInfo is still seeing some resilience in its larger enterprise business. Upmarket annual contract value (ACV), which now makes up roughly 75% of the company’s total business, grew 5% YOY in Q1. That marked a slowdown from the prior quarter, but it still came in ahead of the 3% growth recorded a year earlier. Meanwhile, the downmarket segment continued to struggle, with ACV declining 11% annually. Net revenue retention held steady at 90% for the third straight quarter.

The company added 32 customers spending more than $100,000 in ACV compared to last year, although that figure declined by 21 sequentially. Management said the sequential drop was driven more by softer upsell activity late in the quarter rather than widespread churn among large clients. Software customers, however, became a fresh pressure point, as improving retention trends that had been building for nearly two years flattened out in Q1.

On the brighter side, ZoomInfo highlighted customer wins with Lyft (LYFT), Wyndham Hotels & Resorts (WH), and several AI-focused businesses. Management noted that many AI-native clients are using ZoomInfo less for traditional software seats and more for high-volume data consumption, signaling the evolution of customer behavior as AI reshapes sales workflows.

Looking ahead, ZoomInfo Technologies is clearly preparing investors for a rough transition period rather than a quick rebound. For the second quarter, management expects revenue between $300 million and $303 million, adjusted operating income in the range of $103 million to $106 million, and non-GAAP EPS of $0.26 to $0.28.

The bigger concern, though, came from the full-year outlook. ZoomInfo lowered its fiscal 2026 revenue forecast to between $1.185 billion and $1.205 billion, implying roughly a 4% YOY decline at the midpoint. Non-GAAP EPS is anticipated to be between $1.10 and $1.12, consistent with the company’s prior guidance, while unlevered FCF is expected to range between $400 million and $420 million.

Management admitted the business environment deteriorated more than expected, especially across software customers and lower-end clients. At the same time, the company is also moving away from its traditional seat-based pricing model, creating another layer of uncertainty around near-term revenue trends.

Chief Financial Officer Graham O'Brien said the guidance reset reflects weaker macro conditions, softer software demand, pricing transitions, and revenue variability tied to newer consumption-based plans. A large portion of the downgrade also came from restructuring ZoomInfo’s downmarket business. Even so, management believes the company can return to “sustainably positive” growth by the second half of 2027, though investors now seem far less willing to wait patiently for that turnaround story.

Analysts tracking ZoomInfo predict its Q2 revenue to be around $303.3 million, while EPS is expected to be around $0.18. Wall Street analysts also believe profitability could gradually improve over the next couple of years. Current estimates call for fiscal 2026 EPS $0.79, marking a 5.3% YOY growth, followed by another projected annual gain of 8.9% to approximately $0.86 in fiscal 2027.

ZoomInfo Shrinks Workforce

As ZoomInfo pushes deeper into AI-focused operations, the company plans one of its largest workforce restructurings to date, anticipated to eliminate around 600 roles, or roughly 20% of its employees, including the closure of its Israel facilities. The restructuring is expected to deliver nearly $60 million in annual cost savings by early 2027, although the company anticipates taking $45 million to $60 million in restructuring charges over the coming quarters.

Most of the layoffs are concentrated in R&D and downmarket sales and marketing teams as ZoomInfo redirects spending toward AI-enabled engineering, data infrastructure, large language model integrations, and higher-margin enterprise customers.

What Do Analysts Expect for ZoomInfo Stock?

Wall Street’s tone on GTM has turned noticeably more cautious following the company’s first-quarter report. Stifel downgraded the stock to “Hold” from “Buy” and slashed its price target from $12 to $4, pointing to mounting revenue pressures in 2026 and uncertainty around whether the company’s pricing and strategic changes will meaningfully improve growth.

Meanwhile, Citizens also cut its price target sharply, lowering it from $6 to $2.50 while keeping a “Market Underperform” rating after ZoomInfo’s weaker quarterly results and reduced full-year guidance disappointed investors.

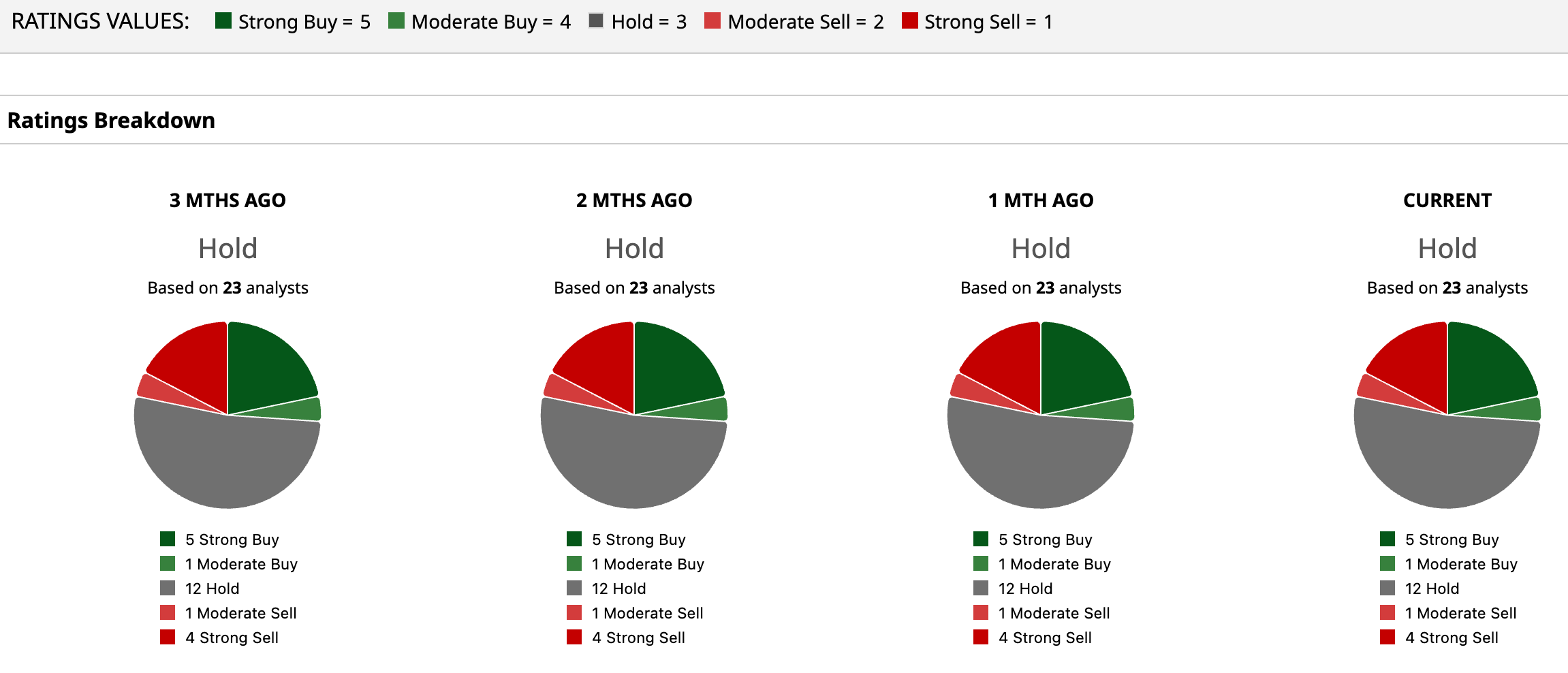

For now, Wall Street seems to be taking a wait-and-watch approach toward ZoomInfo Technologies. GTM stock currently carries a consensus “Hold” rating overall. Of the 23 analysts covering the stock, five advise a “Strong Buy,” one has a “Moderate Buy,” 12 play it safe with a “Hold,” one gives a “Moderate Sell,” and the remaining four are outright skeptical, recommending a “Strong Sell.”

While GTM’s mean price target of $9.11 suggest a rebound potential of 124.4% from the current price levels, the Street-high target price of $15 implies that the stock could rally as much as 269.5% from here.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Elon%20Musk%2C%20founder%2C%20CEO%2C%20and%20chief%20engineer%20of%20SpaceX%2C%20CEO%20of%20Tesla%20by%20Frederic%20Legrand%20-%20COMEO%20via%20Shutterstock.jpg)