/Semiconductor%20Chip%20by%20Gorodenkoff%20via%20Shutterstock.jpg)

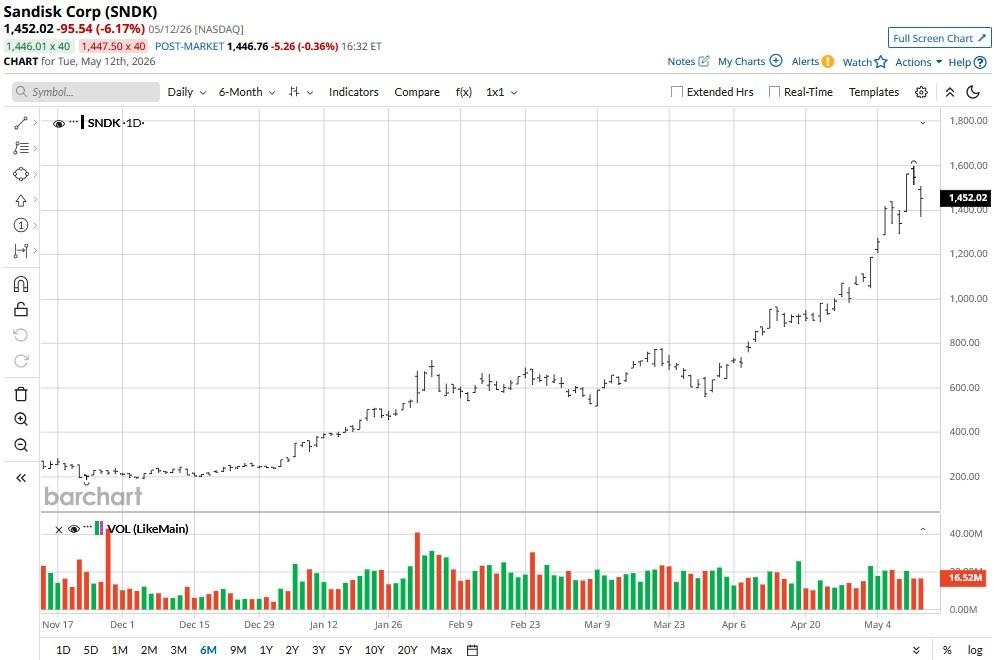

SanDisk (SNDK) shares closed meaningfully lower on May 12 amid a coordinated selloff across the entire memory and semiconductor names.

Investors also bailed on Micron Technology (MU) and Western Digital (WDC) today, reinforcing that weakness in SNDK was mostly related to profit-taking, not company-specific fundamental deterioration.

Despite the decline on Tuesday, SanDisk stock is trading at more than 5x its price at the start of 2026.

Why SanDisk Stock Closed in the Red on Tuesday

Multiple macro factors converged to prompt a selloff in SNDK stock and its AI peers on Tuesday.

A hotter-than-expected April CPI reading of 3.8% year-over-year, the highest in nearly three years, raised fresh concerns about persistent inflation and the Fed holding rates steady through the end of 2026.

Meanwhile, crude oil (CLM26) rallied more than 3% to surpass $100 a barrel again after President Donald Trump cast doubt on the viability of the ceasefire with Iran, describing it as being on “massive life support.”

The continued closure of the Strait of Hormuz feeds directly into inflation expectations, creating a challenging backdrop for high-multiple growth stocks like SanDisk.

Should You Buy the Dip in SNDK Shares?

Long-term investors should consider buying the dip in SanDisk shares as the Nasdaq-listed firm’s fundamental backdrop remains exceptionally strong.

In its latest reported quarter, the multinational saw revenue more than triple to $5.95 billion, with the data center segment gaining an incredible 645% on a year-over-year basis.

On the bottom line, SNDK’s earnings per share (EPS) came in at $23.41, up nearly $9 versus consensus estimates, as adjusted gross margins expanded to 78.4% and free cash flow approached $3 billion.

More importantly, management sees continued upside ahead, guiding for at least $7.75 billion Q4 revenue on $31.5 per share of earnings.

SanDisk has also undergone a structural transformation in its business model.

It has signed five multi-year supply agreements with hyperscaler customers, backed by over $11 billion in financial guarantees, covering more than one-third of projected fiscal 2027 bit output.

These contracts replace volatile spot-market exposure with predictable contracted sales, offering a cash flow floor unprecedented in the NAND flash industry.

Moreover, the firm has retired all long-term debt and authorized a $6 billion share repurchase program that makes this AI stock even more attractive to own in 2026.

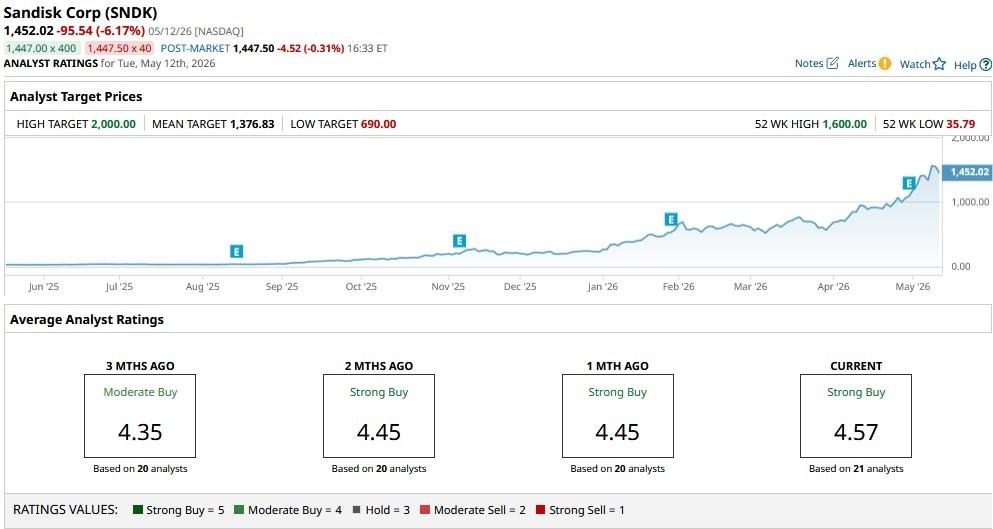

SanDisk Remains Buy-Rated Among Wall Street Firms

What’s also worth mentioning is that Wall Street analysts continue to see significant further upside in SNDK shares.

As of this writing, the consensus rating on SanDisk sits at “Strong Buy,” with price targets as high as $2,000, indicating potential upside of another 38% from here.

This article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20corporate%20sign%20for%20SK%20Hynix%20by%20Tada%20Images%20via%20Adobe%20Stock.jpeg)

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Server%20racks%20by%20dotshock%20via%20Shutterstock.jpg)