In the least surprising news of the day, Bloomberg reported that eBay (EBAY) has rejected GameStop's (GME) $56 billion takeover offer.

As someone said about the cash-and-stock deal, the stock portion would require GameStop to issue $28 billion in shares to pay for it. The video game and collectibles retailer’s stock is currently worth $10.3 billion. Forget the debt component; the stock portion of the transaction screamed dead on arrival.

But I digress.

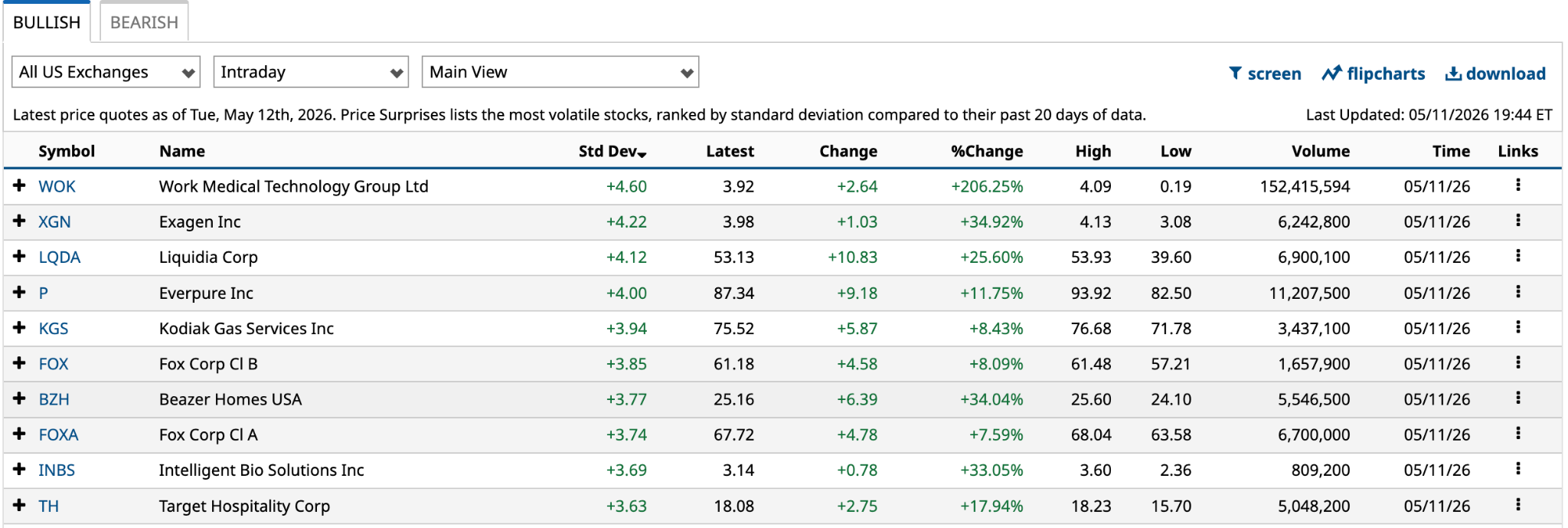

Today's commentary is about bullish and bearish price surprises. Given the market's momentum continues to confound me on valuation grounds, I'd like to examine a stock that remains relatively cheap but was one of Monday’s top 10 bullish price surprises.

I'm referring to Fox Corp’s Class A (FOXA) and Class B (FOX) shares, which both gained more than 7% yesterday on good Q3 2026 results, leading to standard deviations of 3.74 and 3.85, respectively.

I’ve watched it for a while now, thinking, how can it be so cheap? The Murdoch-controlled company -- CEO Lachlan Murdoch, Rupert Murdoch’s son, held 36.4% of the Class B voting shares as of Sept. 25, 2025, effectively controlling the business, as the Class A shares don’t carry voting rights -- owns several media properties, including Fox News and Fox Sports.

Business is good. But is it worth owning for the long haul? Let me dwell on that.

The Reason for Low Valuation

As a Canadian, I’m not a big fan of Fox News’ interpretation of what’s happening in the world today, but that doesn’t mean it’s uninvestable, far from it. Businesses such as Philip Morris (PM) have been good investments for decades because of their strong cash flow generation, despite selling products that routinely make people sick and, in many cases, die.

As I mentioned in the introduction, Fox reported its Q3 2026 results on Monday. Revenues and profits exceeded analyst expectations, but the quarter had some issues. It wasn’t perfect.

While its revenues of $3.99 billion were $180 million higher than the analyst consensus, they were 8.6% lower year over year. On the bottom line, its adjusted earnings per share were $1.32, 35 cents better than analyst expectations and 22 cents higher than last year.

The big reason for the decline in revenue was the absence of a Super Bowl in the quarter. In the third quarter of 2025, it reported advertising revenue from Super Bowl LIX, which set a record with an average of 127.7 million TV and streaming viewers during the broadcast. Fox will next televise the Super Bowl in February 2029.

That’s a loss of revenue in 3 out of 4 years, which isn’t ideal for attracting long-term investors. That’s one reason for a low valuation.

The second reason is also tied to the Super Bowl, as the company has hitched its wagon to linear television. Advertisers are moving away from broadcast and toward streaming to engage their customers.

Of course, this move away from linear TV has been going on for more than a decade. The Globe and Mail, Canada’s national newspaper, published an article in January 2014 titled How Fox aims to fix the traditional TV model.

It’s an interesting read that speaks to Fox management’s recognition at the time that traditional TV and, by extension, advertising, were completely changing how programs were made, when they reached your television, and how advertisers engaged their customers. It’s still changing.

Finally, the sale of Fox’s entertainment assets to Disney (DIS) for $71 billion in March 2019 left Fox less diversified amid changing tides in entertainment and media.

That’s reduced the attraction of owning Fox relative to other entertainment businesses.

For example, according to S&P Global Market Intelligence, Fox’s enterprise value (EV) is 8.2 times its EBITDA (earnings before interest, taxes, depreciation, and amortization), compared with 10.8x for Disney.

People are willing to pay more for Disney because it offers more entertainment, including Disney+, its successful streaming service, Disney Resorts and Cruises, and much more.

Fox is definitely the ugly duckling of the two.

Share Prices Follow Earnings

If you bought FOXA shares after the sale of the company’s entertainment assets to Disney, your stock has appreciated by 62% over seven years, a CAGR (compound annual growth rate) of 7.2%. The S&P 500 over this period has a 17.7% CAGR.

I don’t think you can argue that it’s delivered mediocre performance for shareholders since the breakup and sale of parts of its business.

But that doesn’t mean it can’t outperform in the years to come. Over the past year, it’s gained 29%, while its two-year return is 106%, so slowly it’s becoming a momentum stock, if not a growth stock.

The good news, as the adage says, is that share prices follow earnings. Since 2020, Fox has broadcast the Super Bowl three times: February 2020, 2023, and 2025.

The annual revenues in the off years (2021, 2022, and 2024) varied from a low of $12.91 billion in 2021 (June year-end) to $13.98 billion in 2024. Not much growth.

Meanwhile, despite the lack of revenue growth, its EBIT (earnings before interest, taxes, depreciation and amortization) stayed between $2.44 billion in 2024 and $2.74 billion in 2021. Yet, because of share repurchases, its earnings per share were higher in 2024 ($2.73) than in 2021 ($2.33), despite $300 million less in EBIT.

Perhaps the biggest eye-opener is the difference between June 2021 and June 2024 in their forward P/E ratios. In June 2021, it was 13.97x, compared to 8.92x in June 2024. Fast forward to March 2026. It was in between the two at 11.62x.

Free cash flow is one of my favorite financial metrics because it gives you a good idea of a business’s ability to cover its operating expenses and keep the lights on.

As of Q3 2026, its trailing 12-month free cash flow was $2.14 billion. Based on an EV of $30.53 billion, it has a free cash flow yield of 7.0%. I consider anything above 8% to be in value territory. Given valuations, that’s essentially in value territory right now.

As of June 30, 2021, its annual free cash flow was $2.16 billion. Based on an EV of $23.97 billion at the time, its free cash flow yield was 9.0%, putting it in value territory, 200 basis points above today's level.

The Bottom Line on FOXA Stock

In the first three quarters of fiscal 2026, Fox has repurchased $1.9 billion of its stock, 2.5 times higher than in the same three quarters a year ago. In the last three fiscal years, it has repurchased $4 billion of its stock at an average of $34.78, well below its current price.

The company clearly prefers share repurchases to dividends. They have been profitable for it, nearly doubling its return on investment. I’d have to look more closely at the share prices, highs, and lows in 2023, 2024, and 2025 to determine whether they bought well or just benefited from a rising tide.

While I personally wouldn’t buy the stock, if you’re not a dividend-focused investor, its profitability and stock buybacks should help keep its earnings per share moving higher.

And despite the gains over the past year, its valuation metrics are still very reasonable. In this market, it is a value buy.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Netflix%20on%20tv%20with%20remote%20by%20freestocks%20via%20Unsplash.jpg)

/Netflix%20open%20on%20tablet%20by%20rswebsols%20via%20Pixabay.jpg)