/Quantum%20Computing/Image%20by%20Funtap%20via%20Shutterstock.jpg)

Quantum computing stocks, over the last few years, have largely soared on bold promises, futuristic projections, and investor excitement, rather than actual commercial progress. But IonQ (IONQ) is starting to look different, claiming that the quantum industry is finally moving beyond experimentation and into commercialization. IonQ builds quantum computers and related quantum networking, security, and sensing technologies. According to its recent Q1 report, the company’s major technological breakthroughs could accelerate the timeline for practical quantum computing.

Over the last five years, IonQ shares have soared 390%, outperforming the broader market gain of 76%. But, so far this year, the stock has climbed just 5.2%.

Let’s find out what if IonQ isn’t just claiming but showing concrete proof that could boost its stock towards $100 in 2027.

IonQ Q1 Growth Suggests Real Commercial Demand

IonQ reported its strongest quarter in its history this year. In the first quarter, total revenue under GAAP (generally accepted accounting principles), climbed by a staggering 755% year over year (YOY) to $64.7 million, marking its fourth consecutive quarter of record revenue. Revenue exceeded the company’s guidance by 30% and above consensus estimates by $14.9 million.

Importantly, much of this growth was organic rather than driven purely by acquisitions or accounting adjustments. And IonQ expects organic revenue growth to hit 100% year-over-year for full-year 2026. Furthermore, commercial customers accounted for around 60% of Q1 revenue rather than government contracts. International demand is also gaining traction, with 35% of revenue coming from global markets. IonQ stated that it sold products in more than 30 countries compared to only a handful a year ago, showing meaningful commercial progress.

Another strong signal of demand was the jump in RPO (remaining performance obligations) from roughly $72 million to $470 million in just one year. RPO measures the contracts the company has signed but not delivered or recognized it as sales yet. This suggests that more clients are prepared to commit to IonQ's technology prior to delivery. This is critical for an industry that is still in its infancy and trying to prove its commercial relevance. Analysts project IonQ revenue to climb by 106.5% in 2026, followed by another 45% in 2027.

IonQ Says It Already Has a Technical Edge

IonQ also claimed that its technology is outperforming competitors in significant ways. Its systems have shown up to 10,000-fold faster time-to-solution for some quantum algorithms, including a 1,000-fold gain in the quantum Fourier transform, according to the company. These systems are extremely valuable for cryptography, drug development, and advanced materials research.

One major concern has been that quantum computing still lacks practical real-world uses, which IonQ argues is changing. It highlighted projects across several industries, including engineering simulations with Synopsys and logistics optimization for autonomous freight systems with Einride, among others. It is also expanding into health care applications such as cancer research, DNA reconstruction, and gene therapy optimization.

Despite the impressive revenue growth, IonQ is still far from profitability. Its research and development expenses rose 215% YOY to $125.7 million in Q1. While the company reported GAAP net income of $805.4 million, management made it clear that it was largely driven by a non-cash $1.1 billion warrant valuation adjustment tied to stock price movements. So, while the GAAP net income looked positive on paper, it was not from selling quantum products profitably. Moreover, management expects full year adjusted EBITDA loss between negative $310 million and negative $330 million.

On the brighter side, IonQ's balance sheet remains unusually strong for an emerging growth stock. It ended the quarter with $3.1 billion in cash, cash equivalents, and investments, allowing it a flexible runway for research, manufacturing expansion, acquisitions, and commercialization efforts.

Is IonQ Stock a Buy Now?

With rapidly growing revenue, rising commercial adoption, expanding global demand, meaningful government partnerships, and increasingly detailed plans for scaling its technology, IonQ may be ahead of its rivals. However, the quantum computing industry remains young, expensive, and highly competitive. IonQ is spending aggressively, profitability is still years away, and many of the biggest promises surrounding quantum computing may take time to materialize. Thus, IonQ remains a long-term, high-risk, high-return stock suitable for aggressive investors.

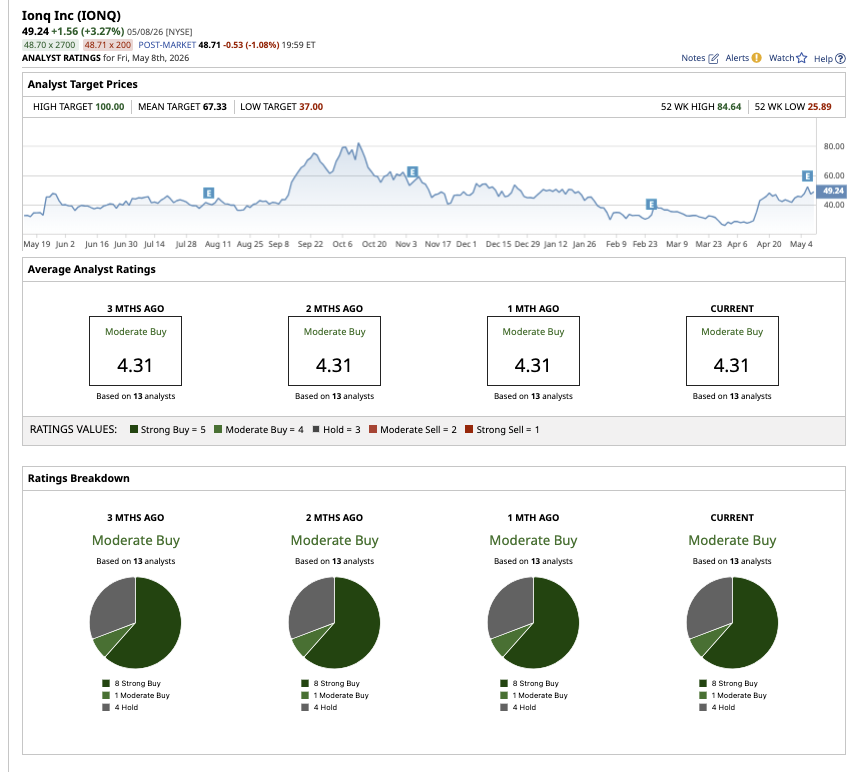

On Wall Street, IonQ has a consensus rating of “Moderate Buy.” Among the 13 analysts covering IONQ stock, eight rate it a “Strong Buy,” one calls it a “Moderate Buy,” and four suggest it is a “Hold.” Analysts have assigned an average price target of $67.33, suggesting the stock can rally 37% from current levels. The high price estimate of $100 implies upside potential of 103% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)