/The%20Cloudflare%20logo%20displayed%20on%20a%20smartphone%20screen%20by%20T_%20Schneider%20via%20Shutterstock.jpg)

For years, Cloudflare (NET) became one of the internet’s most important gatekeepers, helping websites load faster, blocking cyber threats, and keeping digital traffic moving behind the scenes. But now, the company finds itself at the center of a very different conversation. And it's one that’s becoming impossible for the tech industry to ignore.

Cloudflare recently posted another quarter of record revenue, yet investors still hit the brakes after the company disclosed its plans for a sweeping workforce reduction linked to its strategic shift toward artificial intelligence (AI). The company announced plans to cut roughly 20% of its workforce, marking its first major layoffs in its 16-year history.

Management insists the move is not simply about cutting costs, but about rebuilding Cloudflare around what executives describe as an “agentic AI-first” future. CEO Matthew Prince said internal AI usage has surged over 600% in Q1, with AI agents now helping teams across engineering, finance, HR, and marketing handle tasks that once required far larger support operations. That shift is expected to ultimately make the company leaner, faster, and more innovative.

Still, the transition is creating fresh uncertainty on Wall Street. The company expects to take restructuring charges of up to $150 million, while investors question whether aggressive AI-driven restructuring could slow hiring, strain customer-facing operations, and weigh on near-term growth, especially as expectations for AI companies remain sky-high.

With analysts somewhat optimistic on Cloudflare, let’s take a closer look at the stock.

About Cloudflare Stock

Founded in 2009, San Francisco-based Cloudflare has become one of the internet’s most important infrastructure companies. Best known for its cloud-based cybersecurity and networking tools, Cloudflare helps businesses protect websites, apps, public cloud systems, and even IoT devices from cyber threats while keeping digital traffic running smoothly.

Its platform includes web application firewalls, bot management, content delivery services, and load balancing tools designed to improve both speed and security. The company’s cloud-first networking platform, Cloudflare One, has also gained traction with enterprises, financial firms, and government organizations. More recently, Cloudflare has leaned heavily into AI infrastructure, supporting generative AI workloads and strengthening security around AI-driven applications. With a market capitalization of $69 billion, Cloudflare is increasingly positioning itself at the center of the next era of cloud and AI computing.

Shares of the cloud security and performance company have been trading like a high-speed tech thriller over the past year – full of sharp rallies, sudden drops, and enough volatility to keep investors glued to their screens. After Cloudflare’s blockbuster Q3 report, shares hit an all-time high of $260 level in early November as Wall Street piled into the company’s AI and cybersecurity story.

Then reality stepped in. As 2026 began, concerns began to build that AI-native systems could eventually push cybersecurity further upstream, reducing the need for some traditional monitoring layers. That pressured the stock, sending shares lower through February. But true to form, NET bounced back hard, and by May 7, the stock had climbed right back to $258.88, nearly reclaiming their previous highs and reminding investors why Cloudflare remains one of the market’s favorite AI-infrastructure plays.

Then came the latest twist. Despite strong Q1 numbers, the stock lost momentum fast and plunged nearly 24%, dragging shares down to $196.13 as investors reacted nervously to the company’s AI-driven restructuring plans. Trading activity also hinted at the mood shift. Green volume bars that dominated much of the recent rally suddenly gave way to a heavy red selloff in the latest session. Meanwhile, the 14-day RSI has slipped to 43.41 amid rising selling pressure.

Still, even after the chaos, NET stock is up nearly 46.52% over the past year.

When we look at NET’s valuation, it still feels expensive enough to make traditional value investors choke on their coffee. The stock trades at roughly 165 times forward adjusted earnings and nearly 25 times forward sales, definitely not bargain-bin territory. But here’s the twist – compared to its own history, the stock is actually cheaper than where it traded through much of the last five years. So, while Cloudflare stock still carries a hefty premium versus the broader software sector average, the market is no longer pricing it like pure hype alone.

A Closer Look at Cloudflare’s Strong Q1 Report

Cloudflare started 2026 with impressive numbers. When the company reported first-quarter results on May 7, the numbers came in stronger than expected, almost across the board, showing that demand for AI infrastructure, cybersecurity, and enterprise networking is still running strong. CEO Matthew Prince said AI is creating a “fundamental replatforming of the Internet” and called it one of the biggest opportunities in Cloudflare’s history.

That momentum showed up clearly in the numbers. Non-GAAP EPS amounted to $0.25, up 56.3% year over year (YOY) and ahead of expectations. Revenue climbed 34% annually to $639.8 million, again beating Wall Street’s projections.

The growth was fueled by strong enterprise demand, rising public-sector adoption, and customers continuing to prioritize cybersecurity and zero-trust networking. The web security and content delivery company also saw a major boost from channel partners, which generated $193 million in revenue and surged 71% annually. Direct customers brought in another $446.8 million, up 22%.

Big customers kept rolling in, too. During the quarter, Cloudflare added new large clients spending more than $100,000 annually, bringing the total to 4,416. Those larger customers now account for roughly 72% of total revenue. Even more encouraging, the company’s dollar-based net retention rate improved to 118% from 111% a year earlier, showing existing customers are continuing to spend more.

Ordinarily, those kinds of numbers would have sparked a rally. Instead, investors focused on what came next. Alongside earnings, Cloudflare revealed a major restructuring tied to its push toward an “agentic AI-first” operating model. The company plans to cut around 1,100 jobs – roughly 20% of its workforce – marking the first mass layoff in its history. Management says the move is aimed at improving speed, efficiency, and innovation as AI agents increasingly handle internal workflows. The restructuring is expected to cost between $140 million and $150 million, with most of the charges landing in the second quarter and the process largely complete by the end of Q3.

Looking ahead, Cloudflare expects second-quarter revenue between $664 million and $665 million, representing 30% YOY growth. While that is still a strong growth rate by most standards, investors appeared uneasy because it marks a slowdown from the company’s top-line growth in Q1. Non-GAAP EPS is estimated to be about $0.27.

Management raised its full-year 2026 outlook. The company now expects annual revenue between $2.805 billion and $2.813 billion, while non-GAAP EPS is projected between $1.19 and $1.20, both higher than previous guidance.

Analysts tracking Cloudflare predict its Q3 revenue to be around $666.2 million, while loss per share is expected to narrow to $0.04 per share. Wall Street also sees the company steadily moving closer to profitability over the longer term, with loss per share for fiscal 2026 anticipated to shrink by 74.4% YOY to $0.11, and then narrow by another 81.1% annually to $0.02 per share loss in fiscal 2027.

What Do Analysts Expect for Cloudflare Stock?

Even after Cloudflare’s stock slipped following its Q1 earnings report, most Wall Street analysts did not seem overly worried about the company’s decision to cut its workforce. In fact, many brokerage firms viewed the layoffs as part of a much bigger shift – one where Cloudflare is trying to rebuild itself early around AI instead of waiting for the rest of the software industry to catch up. On job cuts, management said customer-facing sales roles would largely be protected, and the number of quota-carrying sales representatives is actually expected to grow in 2026.

That distinction mattered to analysts. Wolfe Research acknowledged its stellar results and believes that the workforce reduction could ultimately help expand margins while revenue growth reaccelerates through 2026.

Morgan Stanley took an even more bullish tone, calling the layoffs a sign of Cloudflare’s innovation leadership and management’s confidence in building an AI-first operating model. Analysts there argued the restructuring was designed to improve productivity, not weaken the company’s go-to-market strategy. They pointed out that future hiring will stay focused on engineers, developers, and sales reps, which are roles tied directly to growth. Morgan Stanley maintained its “Overweight” rating and $245 price target, describing Cloudflare as a potential winner in the emerging “agentic AI” era.

RBC Capital Markets also viewed Cloudflare’s layoff move as a strategic shift rather than a traditional cost-cutting exercise. Analysts said Cloudflare appears to be acting from a position of strength, helped by strong business momentum and massive productivity gains from AI tools already being used internally. According to the brokerage firm, management now believes large support structures and layers of middle management may simply become less necessary in an AI-driven workplace. The firm maintained its “Outperform” rating and $240 price target.

Analysts at Truist Securities echoed similar thoughts, saying rapid AI adoption inside the company is already improving efficiency across engineering and sales operations. They see the restructuring as a proactive effort to align Cloudflare around AI-native workflows that could eventually lead to faster innovation and stronger profit margins. Truist maintained its “Buy” rating and $225 price target.

Not every analyst was fully comfortable, though. Jefferies kept a “Hold” rating and noted that there could be some near-term disruption, especially around internal execution and sales pipeline creation. Still, even Jefferies admitted Cloudflare has historically been quick to adapt during major technology shifts. The brokerage firm pointed out that total headcount could eventually rise again by 2027 as hiring ramps up in customer-facing sales roles that were mostly untouched by the layoffs.

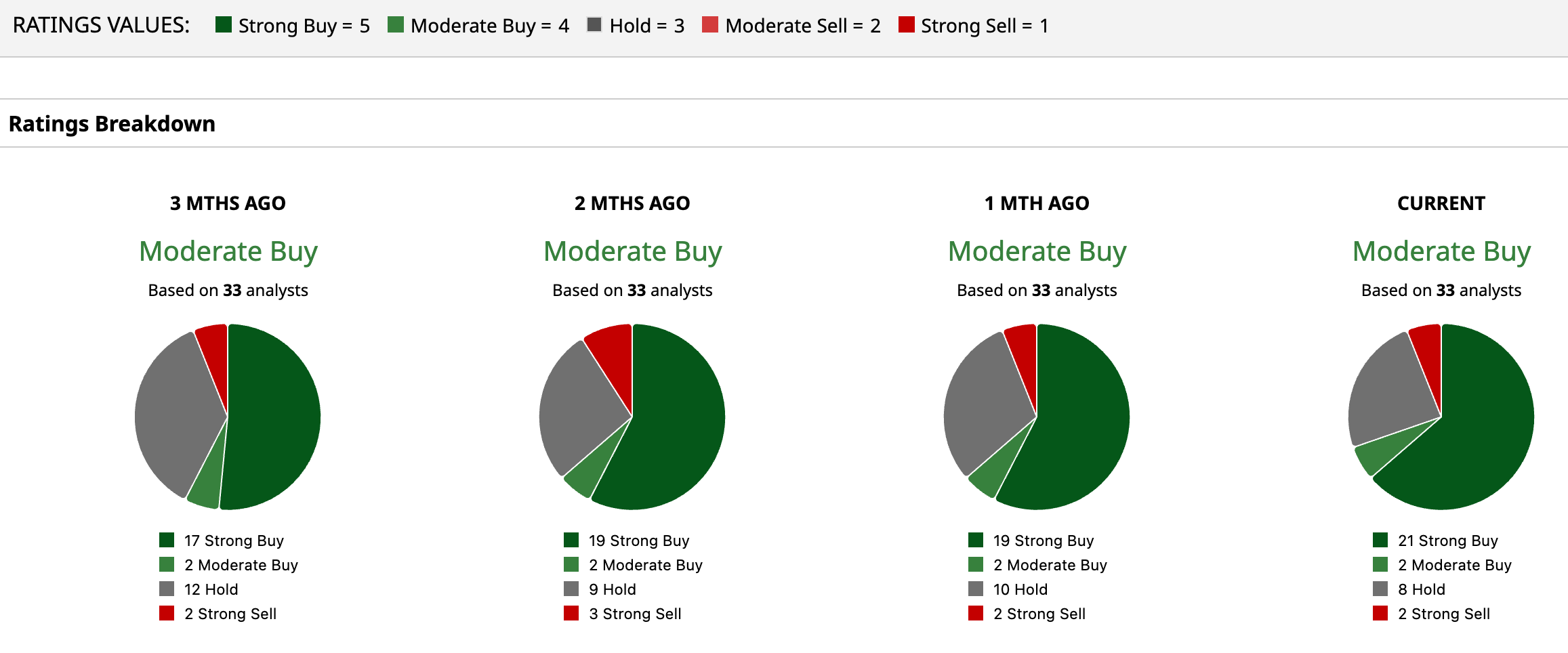

Cloudflare has a consensus “Moderate Buy” rating overall. Of the 33 analysts covering the stock, 21 advise a “Strong Buy,” two give a “Moderate Buy,” eight play it safe with a “Hold,” and the remaining two recommend a “Strong Sell.”

The mean price target of NET stock is $235.97, suggesting a rebound potential of 21.5% from the current price levels. The Street-high target price of $300 implies that the stock could rally as much as 54.5% from here.

Conclusion

Cloudflare now finds itself caught between strong momentum and growing investor caution. The company is still delivering solid revenue growth, winning larger enterprise customers, and pushing deeper into the fast-growing AI infrastructure market. But at the same time, its sweeping layoffs and restructuring plans are raising fresh questions about how disruptive this transition could become. Investors are also paying close attention to the company’s outlook, especially after Q2 revenue growth guidance came in slower than Q1’s pace.

Cloudflare is hardly alone. Companies including PayPal (PYPL), Coinbase (COIN), and Freshworks (FRSH) have tied recent workforce reductions to growing AI adoption, while tech giants like Meta (META), Microsoft (MSFT), and Block (XYZ) are increasingly shifting spending away from payroll and toward AI infrastructure.

For now, Wall Street appears split between viewing these moves as genuine productivity improvements or as aggressive positioning to keep pace with the market’s AI expectations. While many analysts still see meaningful long-term upside for Cloudflare, the next few quarters will likely determine whether this AI-driven transformation becomes a competitive advantage, or creates more volatility before the benefits fully materialize.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Zoetis%20sign%20at%20their%20Canadian%20By%20JHVEPhoto.jpeg)

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)