/AI%20(artificial%20intelligence)/AI%20software%20engineering%20by%20Tapati%20Rinchumrus%20via%20Shutterstock.jpg)

The software sector entered 2026 under heavy pressure as Wall Street’s so-called “SaaSpocalypse” sparked fears that autonomous AI agents could weaken traditional subscription-based business models. Investors rushed for the exits, billions in software market value disappeared within days, and many enterprise software stocks were suddenly treated like businesses with uncertain futures.

But while the market focused on what artificial intelligence (AI) might destroy, it missed where enterprise spending was actually heading. Companies continued pouring money into cloud infrastructure, cybersecurity, AI systems, and digital operations as increasingly complex AI-driven environments created new operational challenges. That shift played directly into the hands of cloud-observability leader Datadog (DDOG).

Datadog was never just another SaaS company. As AI infrastructure and cloud complexity surged, its monitoring and security platform became more essential, turning the AI boom into a growth accelerator rather than a disruption risk.

And now, the company’s latest results made that pretty clear as it challenged many of the earlier fears. After initially falling alongside broader SaaS stocks, DDOG stock has surged and is now trading close to levels last seen in November. The turnaround came recently as the company delivered accelerating revenue growth, its first-ever billion-dollar quarter, expanding customer adoption, and rising demand for newer AI-focused products. An upbeat full-year forecast only added to the momentum, with Wall Street analysts turning more optimistic on the stock again.

What once looked like another casualty of the AI-driven SaaS panic is now looking more like proof that Wall Street may have panicked a little too hard.

About Datadog Stock

Datadog has evolved into one of the most important infrastructure software companies of the cloud and AI era. Founded in 2010 and headquartered in New York, the company provides a unified platform that helps businesses monitor applications, cloud infrastructure, cybersecurity, user experience, and data systems in real time. As enterprises increasingly rely on complex digital environments, Datadog’s software has become a critical tool for keeping operations running efficiently and securely.

Over the past few years, the company has expanded beyond traditional cloud monitoring by integrating artificial intelligence more deeply across its platform. From AI-powered automation tools to Bits AI Agents and LLM Observability, Datadog is positioning itself at the center of the growing AI infrastructure wave. It has a market capitalization of roughly $70.6 billion.

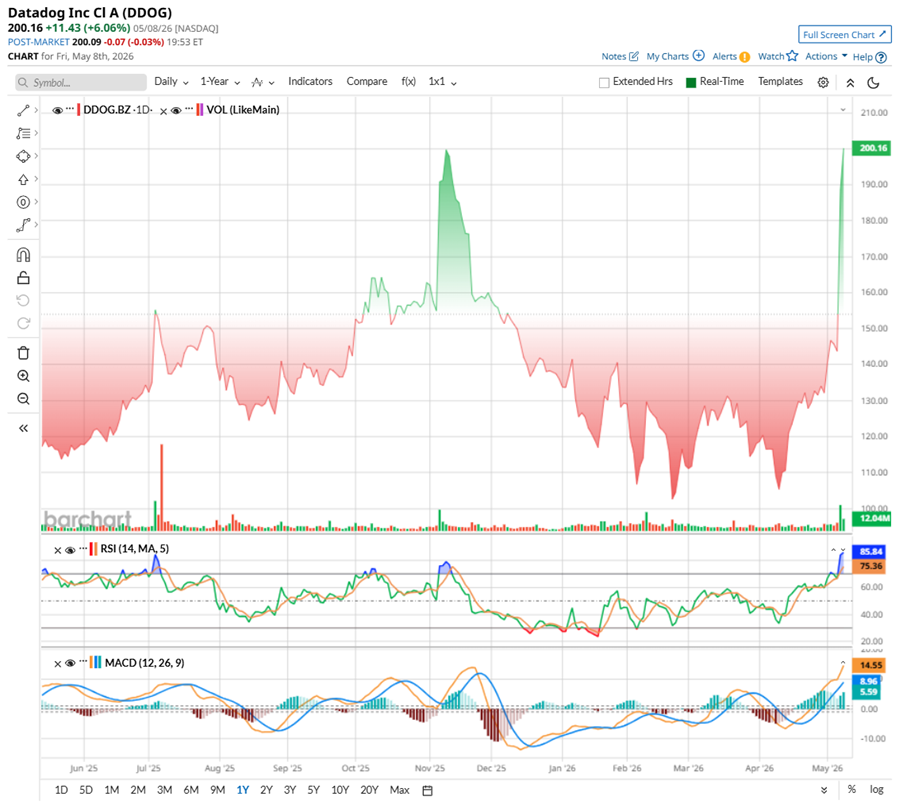

At the start of 2026, Datadog looked like another casualty of Wall Street’s “SaaSpocalypse” fears. The stock tumbled to a 52-week low of $98.01 in February, but that panic did not last long. Since those lows, DDOG has staged a massive comeback, soaring more than 104% and now trading near its all-time high of $201.69.

The momentum has been hard to ignore. Over the past 52 weeks, the stock has climbed 85.5%, while gaining 47.16% year-to-date (YTD). The rally became even sharper in recent months, with DDOG jumping 57.17% over the past three months, 89.92% in the last month alone, and an eye-popping 36.42% in just the past five trading sessions.

Much of that rally came after Datadog delivered a stronger-than-expected Q1 report alongside upbeat guidance. Investors cheered the company’s accelerating AI-native customer growth and improving profitability, sending the stock up 31.3% on May 7 and another 6% in the following session.

Technically, DDOG’s chart still looks heavily tilted toward the bulls. Its 14-day RSI has climbed deep into overbought territory at 85.80, showing just how aggressively investors piled into the stock after the earnings rally. That could lead to some short-term profit-taking or cooling after such a sharp run.

But the broader momentum story remains strong. The MACD line has crossed above the signal line, positive histogram bars continue expanding, and rising green trading volumes suggest bullish momentum remains firmly in control.

Valuation-wise, DDOG stock is priced at 82.73 times forward adjusted earnings and 16.4 times sales, which is higher than the sector averages but it sits below its five-year medians. That suggests the stock is not exactly cheap, but investors continue to justify the premium because of Datadog’s accelerating AI-driven growth and expanding role in enterprise cloud infrastructure.

Datadog’s Q1 Earnings Results Beat Estimates

Datadog delivered standout results for the first quarter of 2026 on May 7, reinforcing the idea that AI is becoming a growth accelerator for the company rather than a threat. The company generated $1.006 billion in revenue during Q1, up 32% year-over-year (YOY) and ahead of both management’s guidance and Wall Street’s expectations. Non-GAAP earnings rose 30.4% annually to $0.60 per share, also comfortably beating estimates. The results marked Datadog’s first-ever billion-dollar quarterly revenue and highlighted broad strength across both AI-native and traditional enterprise customers.

Customer growth remained healthy as Datadog ended the quarter with roughly 33,200 customers, up from 30,500 a year earlier. The company continued expanding deeper inside large enterprises. Customers generating at least $100,000 in annualized recurring revenue (ARR) climbed to around 4,550 from 3,770 last year, and those large customers now account for about 90% of the total ARR.

Datadog’s multi-product adoption trends also continued improving. By the end of Q1, 56% of customers were using four or more products, compared to 51% a year ago. Meanwhile, 35% used six or more products, and 20% used at least eight products, showing that customers are increasingly relying on Datadog across multiple workflows. And, net revenue retention improved into the low-120% range.

The company’s AI momentum appeared especially strong. CEO Pomel said Datadog is seeing a “move to production that is very real” as enterprises scale AI deployments into live environments. New logo annualized bookings more than doubled annually and reached an all-time high, while billings jumped 37% YOY to $1.03 billion, growing even faster than revenue. Remaining performance obligations (RPO) surged 51% annually to $3.48 billion, signaling strong future demand.

Looking ahead, Datadog expects the momentum to continue. Management guided Q2 revenue between $1.07 billion and $1.08 billion, alongside non-GAAP EPS between $0.57 and $0.59. For fiscal 2026, management expects revenue to be between $4.30 billion and $4.34 billion, with non-GAAP EPS projected to be between $2.36 and $2.44. Importantly, that stronger outlook came alongside accelerating billings growth, which often provides a better glimpse into future demand.

Analysts tracking Datadog predict its EPS to be around $0.32 in fiscal 2026, and then double annually to $0.64 in fiscal 2027.

What Do Analysts Expect for Datadog Stock?

Wall Street’s confidence in Datadog strengthened notably after its strong Q1 report, with several brokerages sharply raising their price targets. Stifel lifted its target to $305 from $160 while maintaining a “Buy” rating, pointing to accelerating core revenue growth and improving customer usage trends. The firm also highlighted how Datadog’s earlier investments in sales, marketing, and AI-focused innovation are continuing to pay off as the company gains ground in the fast-changing observability market.

Needham analyst Mike Cikos also turned more bullish, raising his target to $225 from $155 while keeping a “Buy” rating. Meanwhile, Evercore ISI increased its target to $225 from $175 and reiterated its “Outperform” rating, saying Datadog’s impressive beat-and-raise quarter helped ease investor concerns about a possible slowdown in growth during the second half of the year.

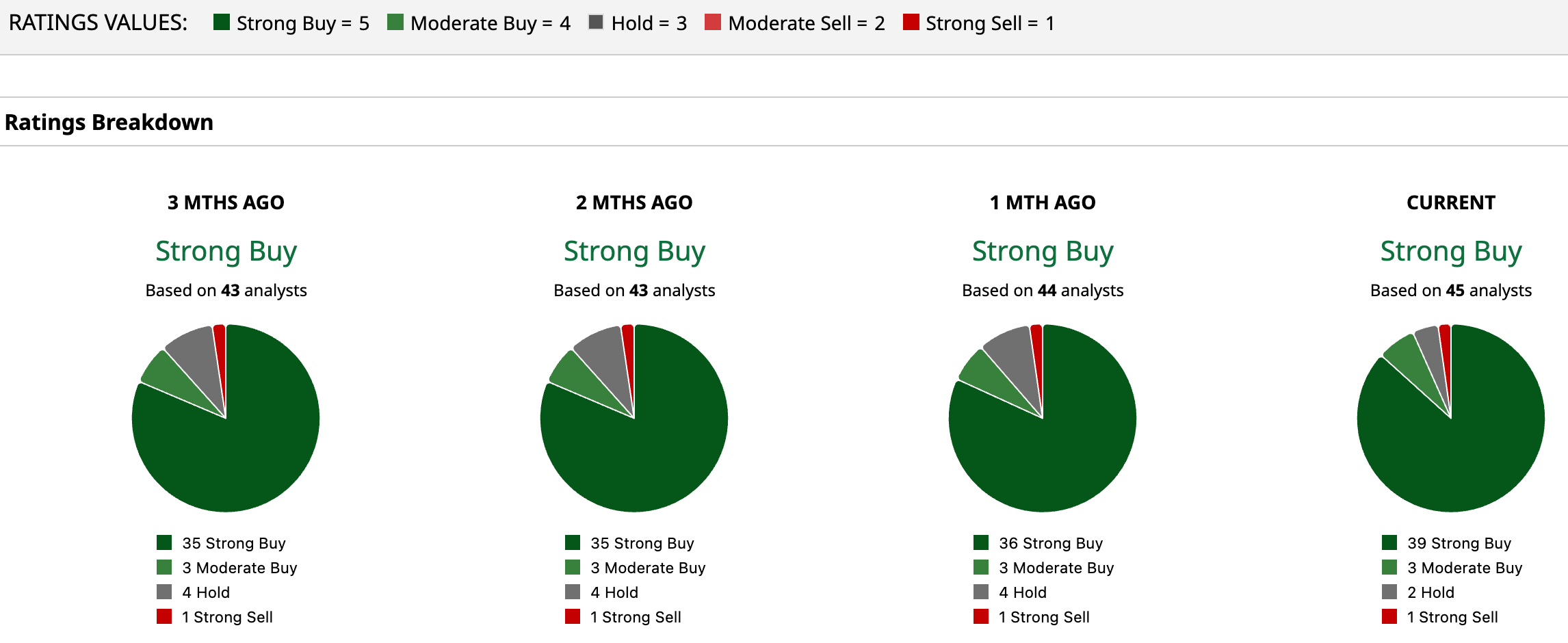

Datadog has a consensus “Strong Buy” rating overall. Of the 45 analysts covering the stock, 39 advise a “Strong Buy,” three recommend a “Moderate Buy,” two suggest a “Hold,” and the remaining one gives a “Strong Sell” rating. While DDOG stock has rallied past its mean price target of $190.56, the Street-high target price of $305 for DDOG implies the stock could rally as much as 52.67%.

Conclusion

The real story around Datadog is that AI may be creating more problems for companies to manage, and that is turning into a pretty big opportunity for Datadog. The more businesses roll out AI agents and automate tasks, the messier their systems become behind the scenes. More workloads, more data, more moving parts, and naturally, more things that can go wrong. And when companies are pouring billions into AI infrastructure, “hoping for the best” is not exactly a strategy.

That is where Datadog keeps showing up. The company is seeing larger enterprise expansions, rising adoption of its AI-focused tools, and growing demand from customers trying to keep increasingly complex systems under control.

In its latest Q1 report, management highlighted strong momentum across both AI-native and traditional customers, including large AI-related contracts tied to model training and GPU optimization. CEO Olivier Pomel also noted that enterprises “can’t afford to be late” in the AI race, which is pushing companies to prioritize deployment speed over building internal monitoring tools from scratch. Even major hyperscalers, which usually prefer building tools themselves, are now leaning on Datadog because the AI race is moving too fast to waste time reinventing the wheel.

Sure, risks are still on the table. AI spending could cool, enterprise budgets could tighten, and competition is not going away. But right now, Datadog does not look like a company getting disrupted by AI. It looks like one of the companies helping hold the entire AI boom together behind the curtain.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)