/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

Palantir (PLTR) has become one of the most closely watched AI stocks on Wall Street. Over the past two years, investors have poured into companies tied to artificial intelligence infrastructure, and Palantir has emerged as one of the biggest winners thanks to explosive growth in both government and commercial demand.

However, unlike many software companies that are still struggling with slowing enterprise spending, Palantir continues to post staggering numbers quarter after quarter. That trend continued in Q1 2026, when the company delivered another massive earnings beat and raised guidance once again.

Even Argus Research described Palantir’s situation as a “high-class problem,” noting that customer demand is growing faster than the company can deploy its AI software.

Still, despite the strong fundamentals, PLTR stock has pulled back from its highs as investors question whether the valuation has become too stretched.

Palantir’s AI Business Is Booming

Palantir is best known for its AI-powered platforms, including Gotham, Foundry, Apollo, and AIP, which help governments and corporations analyze massive amounts of data. The company originally built its reputation through defense and intelligence work, but commercial demand has accelerated sharply during the AI boom.

The company’s momentum has also been fueled by major contract wins. Its Maven AI platform became an official U.S. military program of record, strengthening Palantir’s long-term defense positioning. Meanwhile, a new $300 million Department of Agriculture contract expanded the company’s reach beyond military applications.

CEO Alex Karp has repeatedly emphasized that U.S. demand is "erupting," particularly as government agencies and corporations rush to integrate generative AI into their operations.

PLTR Stock Has Pulled Back Despite Massive Growth

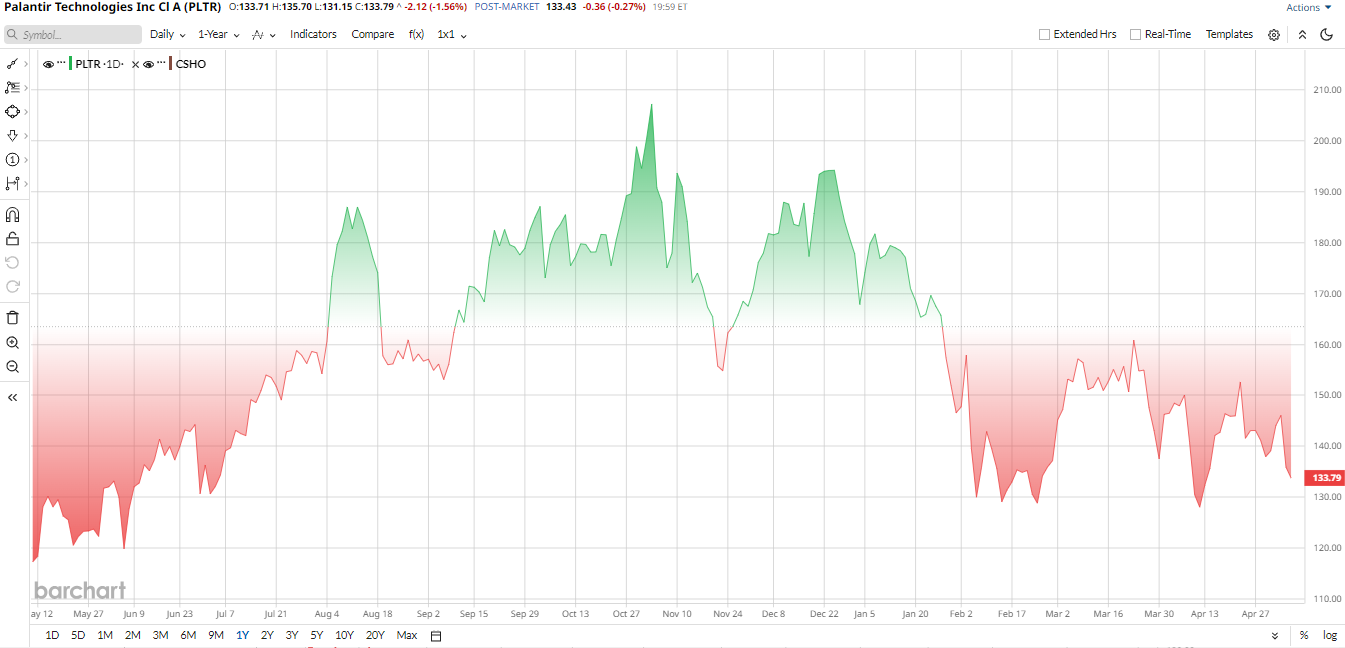

Despite the optimism, PLTR stock has been volatile. Shares surged to around $207 in late 2025 before retreating sharply earlier this year. By May 2026, the stock was down 23% year-to-date (YTD), trading near the mid-$130 range, well below its highs.

The recent pullback came even after Palantir delivered another blockbuster quarter. In fact, shares fell roughly 7% after earnings as traders appeared concerned that expectations had already become too elevated.

The business continues to outperform, but the stock already reflects enormous future growth assumptions.

Palantir Tops Q1 Earnings Estimate

Palantir’s Q1 2026 numbers were difficult to ignore. Revenue jumped 85% year-over-year (YoY) to $1.63 billion, driven primarily by surging U.S. demand.

U.S. commercial revenue climbed 133% to $595 million, while U.S. government revenue increased 84% to $687 million. The company also signed $2.41 billion worth of contracts during the quarter, while its U.S. commercial pipeline approached $5 billion.

Profitability was equally impressive. Net income reached $871 million, translating into a 53% profit margin. Adjusted free cash flow totaled $925 million, or 57% of revenue.

Management also raised its full-year forecast aggressively. Palantir now expects 2026 revenue of roughly $7.65 billion, implying growth of about 71% YoY.

Valuation Remains the Biggest Concern

Even with those growth numbers, valuation remains difficult to justify for some investors.

Palantir currently trades at well above 100 times forward earnings and roughly 77 times sales. Those multiples sit far above the broader software sector and even exceed many fast-growing AI peers.

The market is effectively pricing Palantir as one of the dominant long-term AI software platforms. That leaves little room for execution mistakes or slowing growth.

Still, bulls argue that Palantir’s margins, government positioning, and accelerating commercial adoption may justify premium pricing in the current AI cycle.

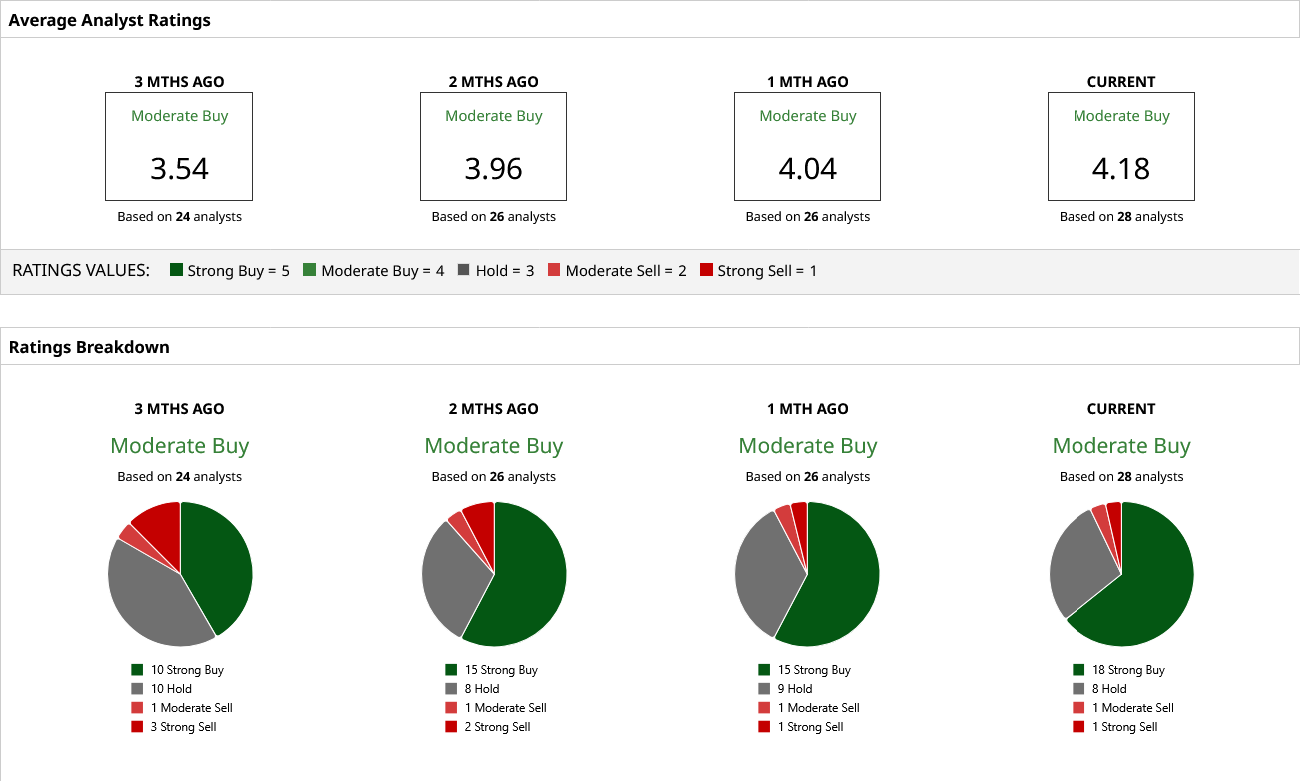

Analysts Remain Cautiously Optimistic on PLTR Stock

Wall Street remains relatively confident in Palantir after the strong results.

Argus Research recently upgraded the stock to “Buy” with a $190 target, citing overwhelming AI demand. UBS also turned bullish with a $180 target, arguing the recent pullback improved the risk-reward setup.

Rosenblatt has been even more optimistic, assigning a $200 target while pointing to rising global defense spending and growing AI adoption.

However, not everyone is convinced. Morgan Stanley maintained an “Equal Weight” rating and warned that much of Palantir’s growth may already be reflected in the stock price. Goldman Sachs has also remained cautious, highlighting the company’s elevated valuation multiples.

Overall, analysts have a consensus "Moderate Buy" rating and continue to praise Palantir’s growth trajectory and cash generation, but many believe the valuation debate will remain the biggest issue surrounding PLTR stock in 2026.

Moreover, analysts set a mean price target of $190.88, suggesting a decent 39% upside run for PLTR from the current level.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/2d%20illustration%20of%20Cloud%20computing%20by%20Blackboard%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)