/Snapchat%20button%20by%20Alexander%20Shatov%20via%20Unsplash.jpg)

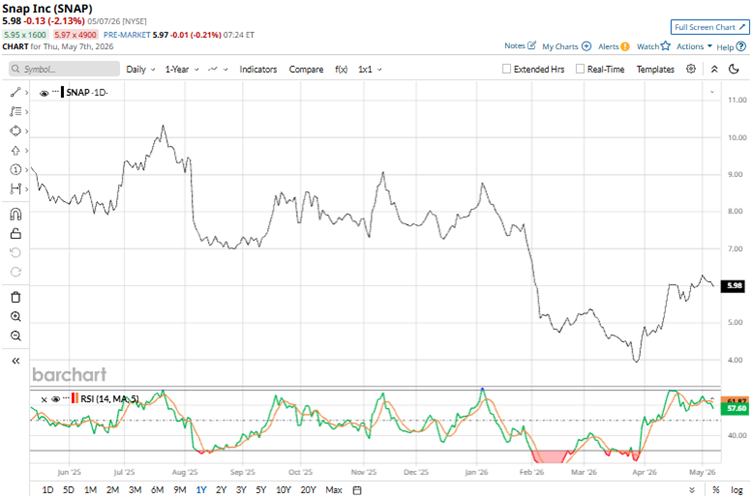

Despite reporting a double-digit revenue growth in Q1, Snap (SNAP) faced pessimistic investor sentiments, dropping 2.13% intraday on May 7, as the U.S.-Iran war took center stage in its results. As a result, the company faced pressure on its advertising revenue and softer growth in key regions, such as North America.

Snap’s advertising revenue increased 3% compared to the prior-year period to $1.24 billion, as growth in direct response advertising revenue was partially offset by continued headwinds in the North America large client advertising business, and about $20 to $25 million impact from the geopolitical headwinds in the Middle East during March, as brand advertisements are more sensitive to geopolitical turmoil.

At this juncture, we take a deeper look at this stock.

About Snap Stock

Tech company Snap is well-known globally for its innovative visual messaging platform, Snapchat, which lets users communicate through photos and videos that disappear quickly.

Beyond Snapchat, Snap extends its ecosystem through developer platforms like Lens Studio for custom AR experiences, hardware innovations such as Spectacles for hands-free capture, and advertising products that connect brands with engaged audiences in immersive, contextually relevant ways. It also offers subscription services, such as Snapchat+, Lens+, and Snapchat Platinum. Headquartered in Santa Monica, California, Snap has a market capitalization of $10.1 billion.

The stock has been under pressure for quite some time, stemming from issues such as Snap's struggles to turn a profit despite revenue growth, high stock-based compensation, and heightened competition from Meta Platforms (META). Over the past 52 weeks, the stock has dropped 27.44%, while it has been down 26.1% year-to-date (YTD). Snap’s shares reached a 52-week low of $3.81 on March 27, but are up 58.3% from that level.

Snap’s 14-day RSI of 57.14 indicates that it's closer to the overbought territory than the oversold territory. Its forward price-to-sales ratio of 1.52 times is higher than the industry average of 1.22 times.

Snap Grappled with User Growth Headwinds in Q1 Despite Revenue Resilience

For the first quarter of 2026, Snap, while recording growth in overall daily active user (DAU) count, is facing some headwinds in key markets. Its total DAU increased 5% year-over-year (YOY) to 483 million. However, its North American DAU decreased 7% YOY to 92 million, while Europe’s DAU dropped 2% to 97 million.

Snap has reported a resilient revenue growth, despite these headwinds. The company’s top line increased 12% YOY to $1.53 billion, which was higher than the $1.52 billion that Wall Street analysts had expected. Moreover, the company’s profitability scenario improved compared to the prior-year period. Its GAAP-based attributable net loss decreased 38% YOY to $0.05 per share, while its adjusted EBITDA increased 115% to $233.33 million.

High stock-based compensation has been a thorn in Snap’s side for quite some time. Last year, the company’s stock-based compensation totaled around $1 billion. In the first quarter of 2026, Snap recorded around $250 million in SBC expenses, slightly higher than the prior year's figure. This has raised concerns about the dilution of existing shareholder value.

The company no longer has the $400 million deal with Perplexity, which was supposed to contribute to its financials in 2026. Snap reported that it has ended the partnership amicably and no longer assumes its contribution to its upcoming sales figures. Last month, it announced cutting 1,000 jobs or 16% of its workforce, citing rapid AI advancements.

However, Wall Street analysts are optimistic about Snap’s ability to lower its bottom-line losses. For the current year, the company is expected to report a loss of $0.12 per diluted share, down 55.6% YOY, while analysts expect an 83.3% improvement to a $0.02 loss per share in the next year.

What Analysts Think About Snap’s Stock

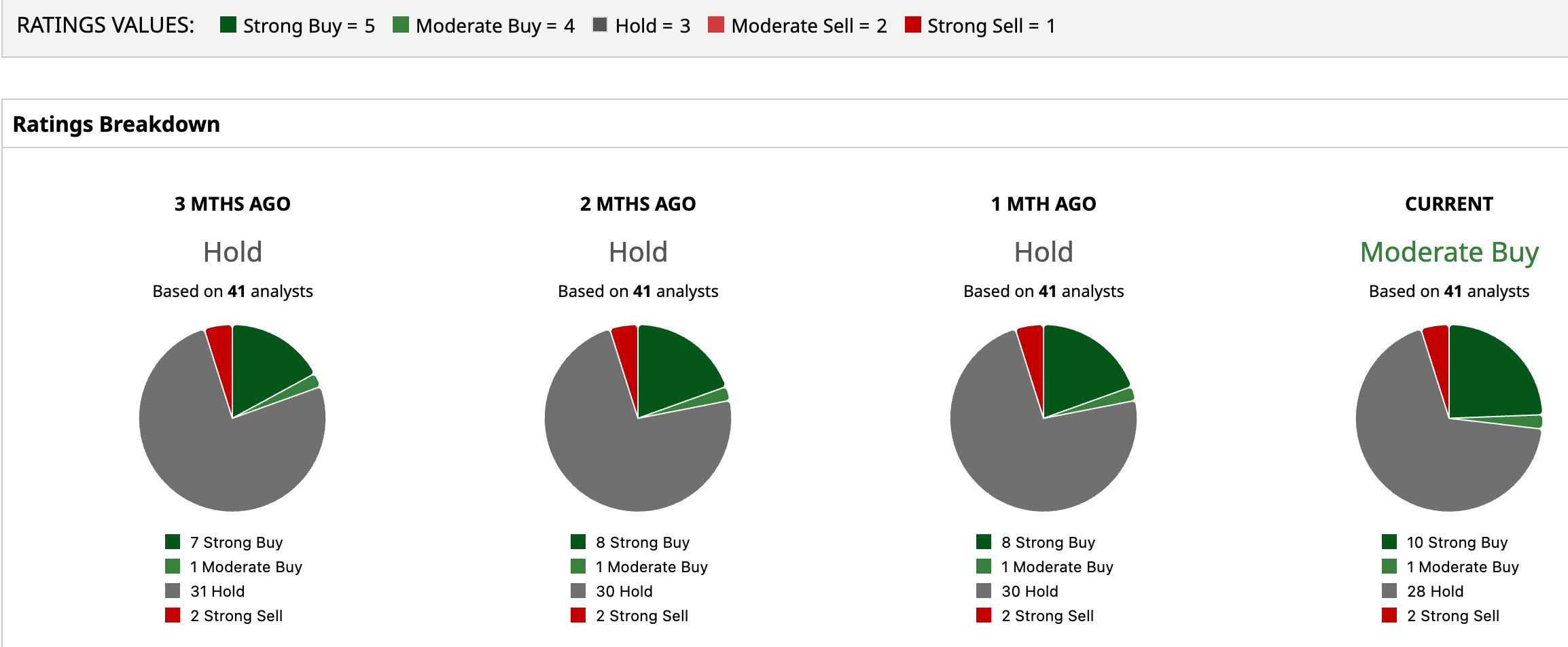

Post Snap’s Q1 results, RBC Capital analysts maintained a “Sector Perform” rating, while lowering the price target from $10 to $8. The analysts at the firm noted the company’s mixed quarterly results, as strong subscription growth and improvements in its advertising platform were somewhat offset by customer headwinds. Goldman Sachs analyst Eric Sheridan also kept a “Neutral” rating on Snap’s stock, but lowered the price target from $8 to $7. On the other hand, Wells Fargo analysts raised the price target from $6 to $7, while maintaining an “Equal Weight” rating.

Snap is still liked on Wall Street, with analysts awarding it a consensus “Moderate Buy” rating overall. Of the 41 analysts rating the stock, 10 have given it a “Strong Buy” rating, one a “Moderate Buy,” 28 a “Hold,” and two a “Strong Sell.” The consensus price target of $8.16 represents a 34.2% upside from current levels. Moreover, the Street-high price target of $15 implies a 146.7% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/A%20close-up%20of%20the%20Broadcom%20logo%20on%20a%20smartphone%20by%20Timon%20via%20Adobe%20Stock.jpeg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)

/Chipset%20held%20over%20rush%20hour%20traffic%20by%20Jae%20Young%20Ju%20via%20iStock.jpg)