/Fortinet%20Inc%20Silicon%20Valley%20office%20sign-by%20Sundry%20Photography%20via%20Shutterstock.jpg)

Shares of cybersecurity company Fortinet (FTNT) were on a roll, rallying more than 20% after it posted strong Q1 results and solid guidance. Putting fears of AI disruption to bed (for now), the company's top and bottom lines handily beat Street expectations.

The "SaaSpocalypse" doom and gloom scenario was not only for traditional SaaS companies, as with Anthropic's Claude Mythos, OpenAI's GPT-5.4 Cyber, and Google's (GOOG) (GOOGL) Big Sleep; agentic AI was supposed to upend the businesses of cybersecurity companies like Fortinet, too. However, the results are singing a different tune.

About Fortinet

Founded in 2000, Fortinet is a cybersecurity company dealing with network security, firewalls, and secure networking. Unlike many cybersecurity firms that are primarily software companies, Fortinet combines proprietary hardware, custom security chips, and software into an integrated platform.

Valued at a market cap of $79 billion, FTNT stock is up 37% on a year-to-date (YTD) basis.

Now, the moot question is: are the fears overblown or worth consideration? And amid this, how do the shares of Fortinet come across as an investment? Let's find out.

Q1: Could Not Have Asked For More

Well, to start with the obvious and to state the obvious, Fortinet's results for the most recent quarter were the reason for its latest strong uptick, and it is justified.

The company grew its revenues by 20% from the previous year to $1.85 billion, with product revenues rising by an even sharper 41% in the same period to $645 million. Further, earnings soared by an even sharper 41.4% to $0.82 per share, coming in much higher than the consensus estimate of $0.62 per share. Impressively, this was the ninth consecutive quarter of earnings beats from the company.

And it is not like this is a recent phenomenon. Fortinet has been growing its revenue and earnings at a healthy clip over the past decade. Its revenue and earnings have demonstrated CAGRs of 21.02% and 72.41%, respectively.

Additionally, Fortinet expects revenue in Q2 2026 to be in the range of $1.83 billion and $1.93 billion, while the Street estimates it to be $1.88 billion. Similarly, EPS is forecasted to be between $0.72 and $0.76; the forecast for the same is $0.74 per share.

Billings, a key indicator of product and services demand for a company, moved up by 31% year-over-year (YoY) to $2.09 billion. With an increasing order book and revenues, the operating margins also expanded to 31.4% from 29.5% in the year-ago period.

Meanwhile, the company was able to transform all of this into growth in cash flows as well. Net cash from operating activities for the quarter rose to $1.1 billion from $863.3 million in the year-ago period. Overall, the company closed the quarter with a cash balance of $2.2 billion, with no short-term debt on its books.

Now, coming to valuation, the stock may seem overvalued. However, it is not trading at unreasonable levels. FTNT is trading at a forward P/E, P/S, and P/CF of 29.89, 8.63, and 24.50, all within the range of sector medians of 24.07, 3.28, and 18.55, respectively.

Fortified Fortinet

Fortinet is a highly diversified company in both products and customers, with a presence across the hardware and software spectrum of the cybersecurity realm. This gives the company an undeniable advantage.

Built on the three verticals of proprietary silicon, owned infrastructure, and a unified operating system, Fortinet has carved out a structural advantage that most competitors simply cannot replicate. The company designs its own purpose-built chips from the ground up, a decision that separates it from the rest of the field and translates directly into products that deliver superior performance at a price point that undercuts rivals, all while sustaining margins that hold above 30%.

Further, the infrastructure story is equally compelling. Fortinet does not rent its network from third parties. It owns it outright, operating across about 200 locations worldwide and controlling in excess of five million square feet of data center space. That ownership structure removes the layer of external markup that weighs on competitors, gives the company precise authority over how its network performs, and creates a cost profile cheaper than competitors.

However, it is in the operating system dimension of this model that the efficiency gains become most visible. Every solution Fortinet has ever brought to market, whether a physical firewall, a cloud SASE node, or an endpoint agent, runs on FortiOS. With this, a capability developed once can be deployed across the entire product portfolio, keeping R&D costs contained and aiding margins. For customers, the result is a tightly integrated ecosystem deepening the relationship between the company and the organizations that rely on it.

Fortinet has also built a recurring revenue dynamic into its business model that deserves recognition. When a client announces the end of support for its most widely used legacy products, a firewall no longer receives critical security patches. This leads to the decision to upgrade being an operational necessity. Fortinet moves through that transition period with an active upselling motion, resulting in the revenue base replenishing itself with a regularity that pure product sales alone could never guarantee.

In terms of competition, with the likes of Palo Alto Networks (PANW) and CrowdStrike (CRWD), Fortinet is ahead on some key aspects. For starters, Fortinet's crown jewel is its FortiGate firewall lineup, which runs on the proprietary FortiOS operating system and is powered by its own custom ASICs. CrowdStrike, by contrast, is built almost entirely around cloud-native endpoint detection and response and largely lacks traditional firewall capabilities, while Palo Alto offers the broadest platform coverage across network, cloud, and endpoint but at a considerably steeper price point. Overall, Fortinet offers a unique combination of custom silicon, a unified operating system, and a sensor grid pulling telemetry from over 5.6 million deployed devices worldwide.

Notably, Fortinet's most significant recent move was the March 2026 launch of FortiOS 8.0, which the company describes as a watershed for its platform strategy. FortiOS 8.0 introduces AI-driven security, next-generation SASE, and quantum-safe protection across three core innovation areas, helping organizations simplify security architecture while preparing for post-quantum threats.

Finally, on the AI front specifically, FortiAI now handles about 90% of routine security alerts for enterprise customers, meaningfully cutting mean time to resolution. The company is also previewing FortiSOC, a cloud-delivered offering that consolidates FortiAnalyzer, FortiSIEM, FortiSOAR, and FortiTIP into a single integrated service with unified log ingestion, correlation, automation, case management, and behavioral analytics.

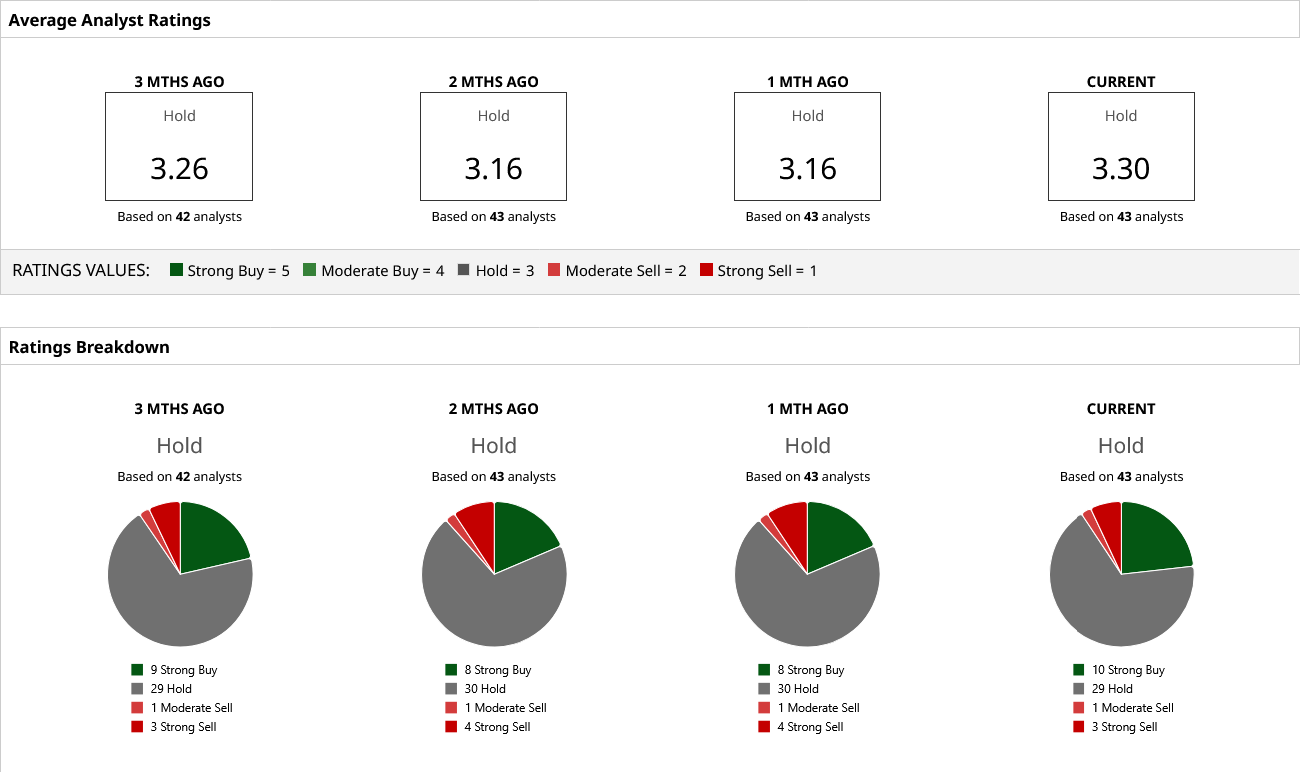

Analyst Opinion of FTNT Stock

Overall, analysts have earmarked a consensus rating of “Hold” for FTNT stock. The mean target price has already been surpassed, and the high target price of $120 indicates an upside potential of about 8% from current levels. Out of 43 analysts covering the stock, 10 have a “Strong Buy” rating, 29 have a “Hold” rating, one has a “Moderate Sell” rating, and three have a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)