While the recent first-quarter earnings report for DoorDash (DASH) wouldn’t exactly be classified as stellar, there were arguably enough positives to justify a sustained rally in DASH stock. However, the market felt otherwise, deeming the underlying competitive pressures and challenging macro environment to be a net drag. Subsequently, the Barchart Technical Opinion indicator still rates DASH as a 56% Sell.

On paper, the delivery service posted mixed results, with adjusted earnings per share of $1.14 beating the consensus estimate of $1.07. However, revenue of $4.04 billion fell a bit short of the $4.15 billion target. Still, for a brief moment, DASH stock ripped higher thanks in large part to the profit beat and an unexpectedly strong guidance for Q2.

Unfortunately, the good vibes didn’t last long. Predominantly, DoorDash faces many headwinds, with investors remaining skeptical about the forward prospects of DASH stock. In particular, the company’s acquisition of Deliveroo, while creating a global delivery giant operating in over 40 countries, has presented many challenges. These include integration risks, where the merging of operations has been a complex process, along with leadership transitions.

Another issue that impacts discretionary players is fee fatigue, a phenomenon where consumers cut back on ordering due to elevated service fees, delivery charges and inflated menu prices. That’s especially problematic for single, routine customers, where a $15 order can easily run up to $35 or higher. At some point, the convenience factor is severely diminished by the economics.

As it turns out, the smart money is especially concerned about the math not mathing.

Premiums Rise for Protection Against DASH Stock

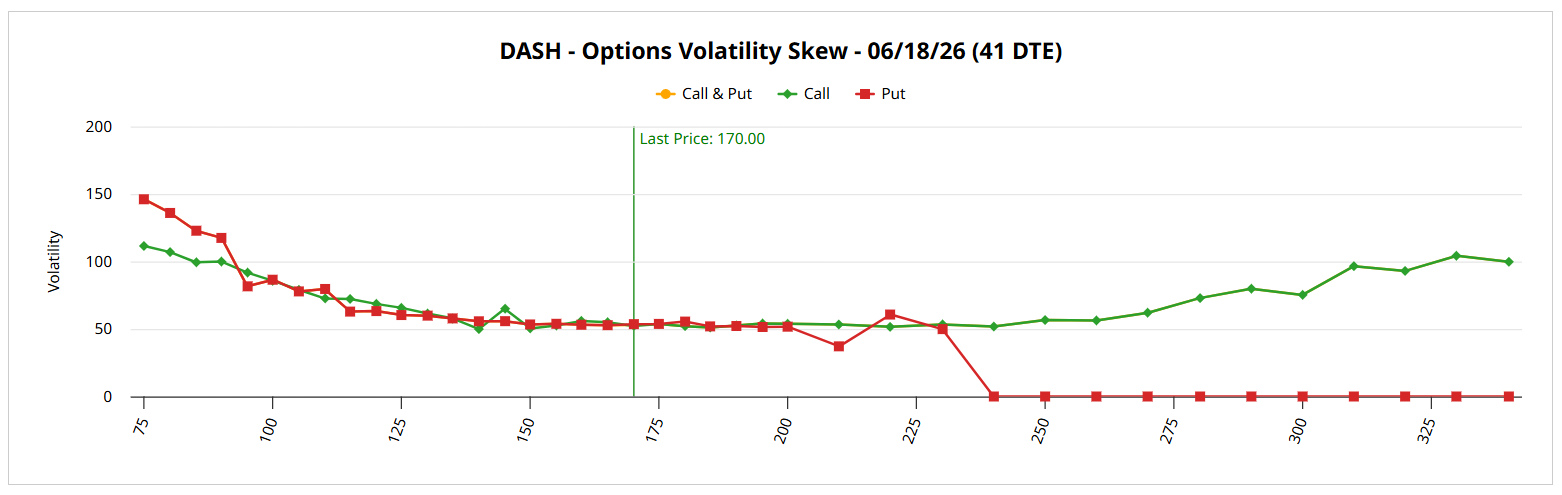

Perhaps the clearest example of sophisticated traders’ apprehensions toward DoorDash stock comes from the volatility skew. By definition, the skew identifies the implied volatility (IV) across the strike price spectrum of a given options chain. By noting the relative elevation and velocity of IV for put and call options, we can gain a better understanding of how the smart money is hedging the target security.

While you can always nerd out to your heart’s delight with options data streams, it’s best to think of the volatility skew as an insurance market. If drivers are concerned about getting into a car wreck, they can choose to buy more coverage. If other drivers collectively acquire the same coverage, we can graph out the demand profile, essentially observing what areas are making people apprehensive.

It’s a similar principle to options skew, and in the case of DASH stock (for the June 18 expiration date), the priority is downside protection. Specifically, put IV soars to around 150% at the $75 strike, implying a heightened premium for out-the-money (OTM) puts relative to the same unit-wise distance for OTM calls.

In other words, the smart money believes that a sharp move in either direction is a low-probability event. However, in the case that such a tail risk materializes, the priority is to defend against catastrophic loss on the left (bearish) tail.

I would say that it’s a reasonable hedge but this action is also underweighting the positives of DASH stock. In addition to the strong Q2 guidance, DoorDash’s monthly active user count hit an all-time high. Despite a challenging economy, the delivery service is clearly generating new sign-ups and retentions.

Plus, the company has made vertical integration a priority, enjoying robust momentum in grocery and retail orders. Therefore, while the year-to-date loss of over 24% is admittedly distracting, fundamental positives exist that could jumpstart a meaningful recovery.

Quantitative Picture is Worth Another Look

Finally, it’s a good reminder that relevant organizations don’t just erode in linear fashion; instead, there’s usually an ebb and flow. In particular, when bearish pressure is sustained for a long time, it takes more “energy” to justify a continued downtrend. As such, buying the dips can be a shrewd means of extracting near-term profits.

Of course, the million-dollar question is, how do we know when a dip is objectively a good buying opportunity? We can attempt to answer this question through inductive probabilities under a Markovian state transition framework. Simply, we observe forward tendencies based on conditioned, quantifiable signals.

Typically, a random 10-week long position in DASH stock (using data since its public debut) would be expected to range between $165 and $195 (assuming a starting price of $171.35). Further, the exceedance ratio — or the percentage of times DASH generates a positive return — stands at 65%.

However, we’re not interested in trading DoorDash stock at random. Instead, we’re looking at the current signal. In the last 10 weeks, DASH printed only three up weeks, leading to an overall downward slope. Under this specific signal, the forward 10-week distribution would be expected to land between $160 and $210, with an exceedance ratio of 69.2%. Further, DASH tends to bounce higher five weeks after a prolonged downturn.

With that in mind, I’m tempted with the 185/190 bull call spread expiring June 18. This trade requires DoorDash stock to rise through the $190 strike at expiration. If it does, the maximum payout stands at 100%.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/Ai%20chip%20by%20Quality%20Stock%20Arts%20via%20Shutterstock.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/Seagate%20sign%20on%20the%20building%20atits%20operational%20headquarters%20By%20JHVEPhoto.jpeg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)