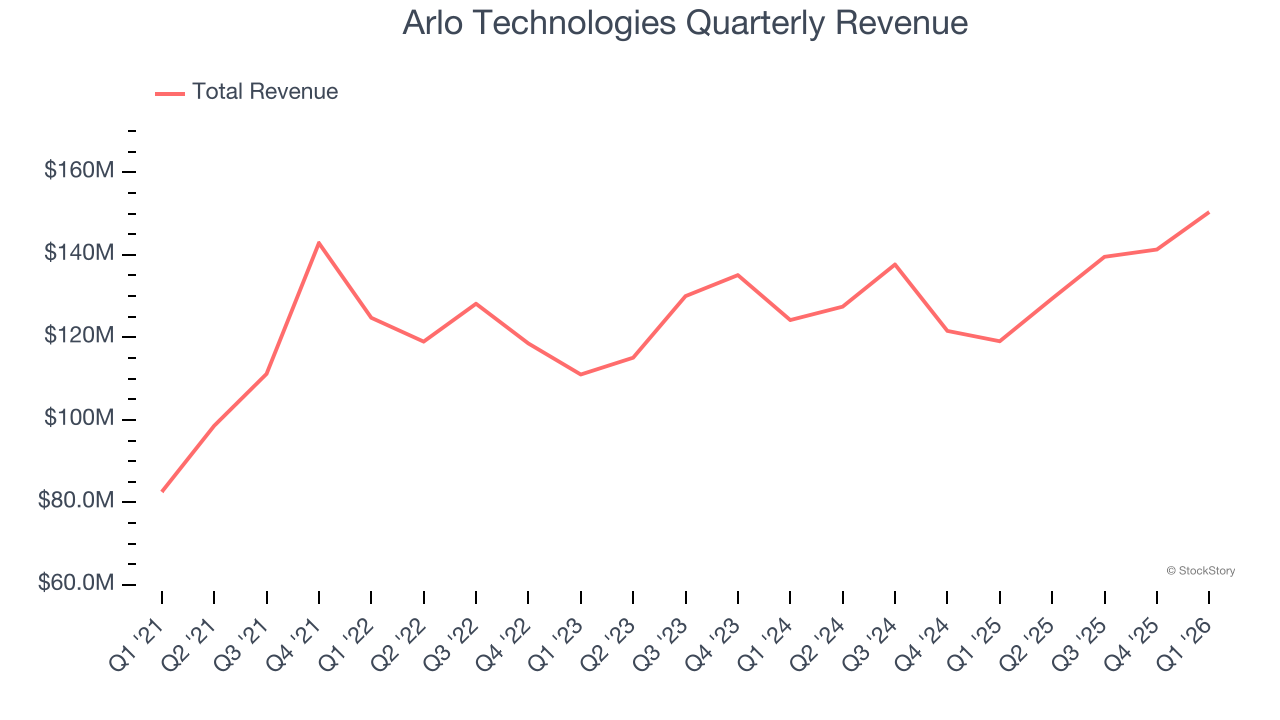

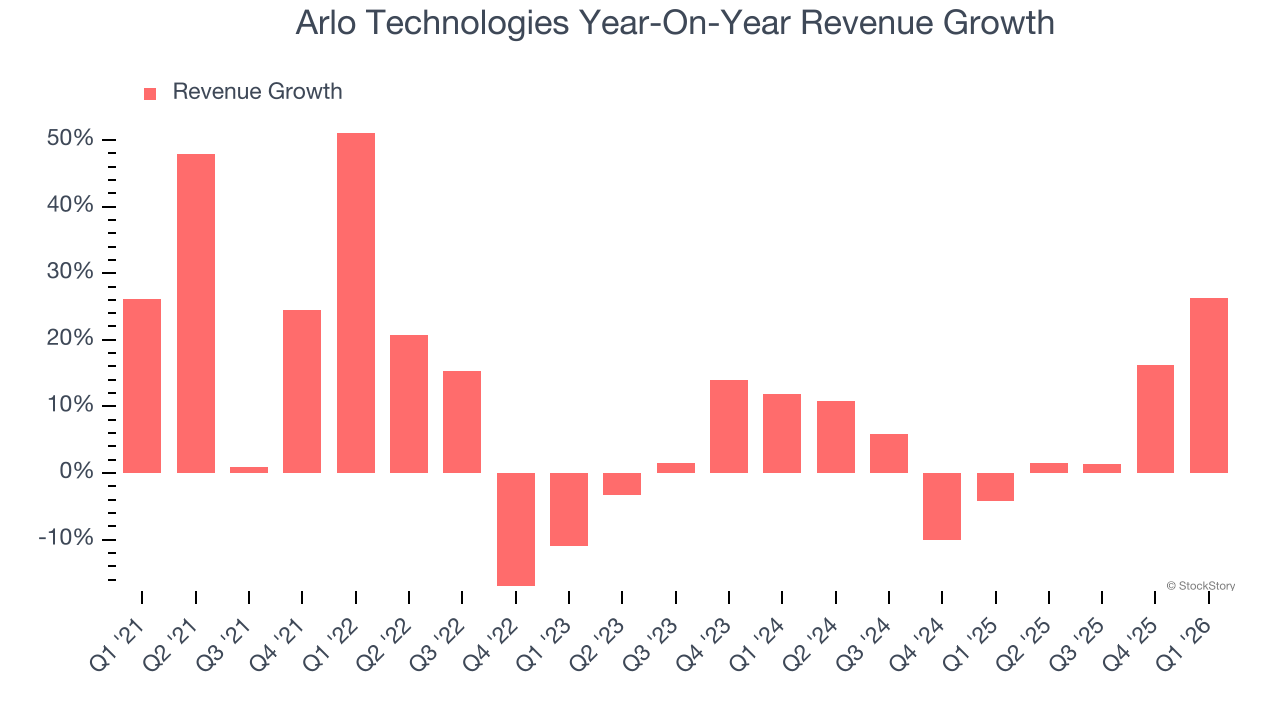

Smart security company Arlo (NYSE:ARLO) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 26.3% year on year to $150.4 million. Guidance for next quarter’s revenue was better than expected at $150 million at the midpoint, 1.8% above analysts’ estimates. Its non-GAAP profit of $0.28 per share was 45.5% above analysts’ consensus estimates.

Is now the time to buy Arlo Technologies? Find out by accessing our full research report, it’s free.

Arlo Technologies (ARLO) Q1 CY2026 Highlights:

- Revenue: $150.4 million vs analyst estimates of $139.7 million (26.3% year-on-year growth, 7.6% beat)

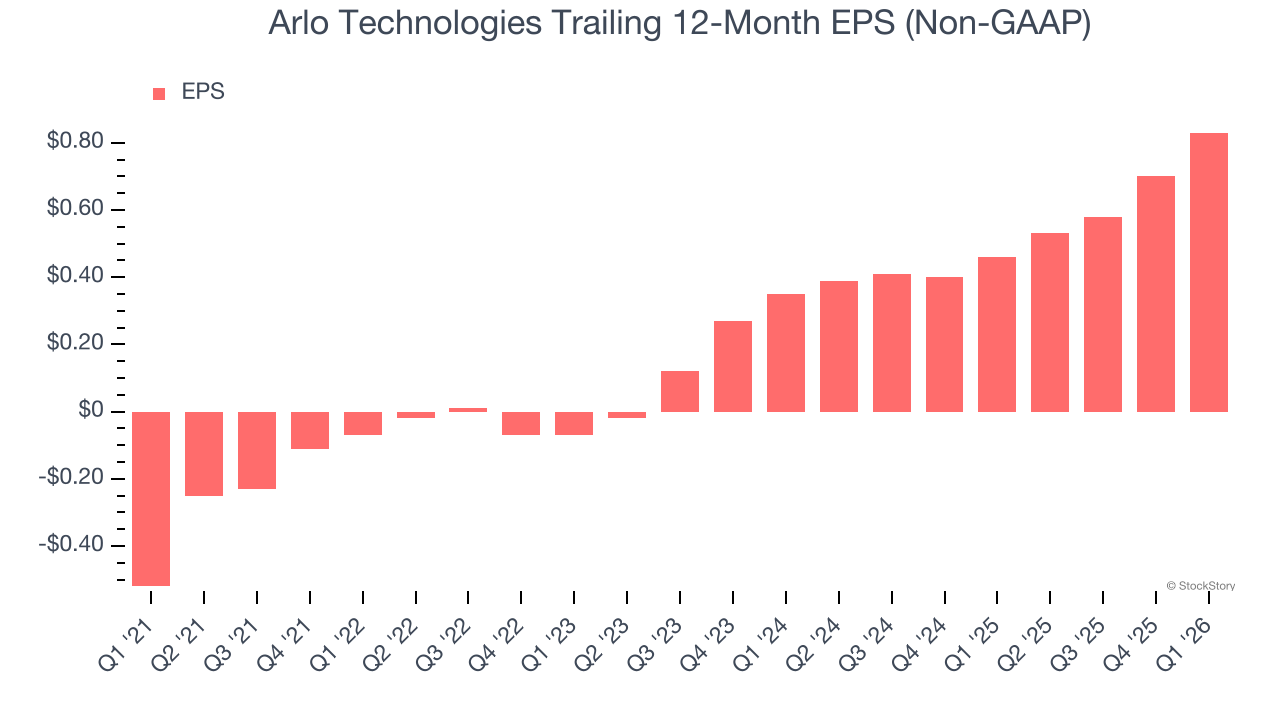

- Adjusted EPS: $0.28 vs analyst estimates of $0.19 (45.5% beat)

- Adjusted EBITDA: $30.42 million vs analyst estimates of $21.03 million (20.2% margin, 44.6% beat)

- Revenue Guidance for Q2 CY2026 is $150 million at the midpoint, above analyst estimates of $147.4 million

- Adjusted EPS guidance for Q2 CY2026 is $0.20 at the midpoint, roughly in line with what analysts were expecting

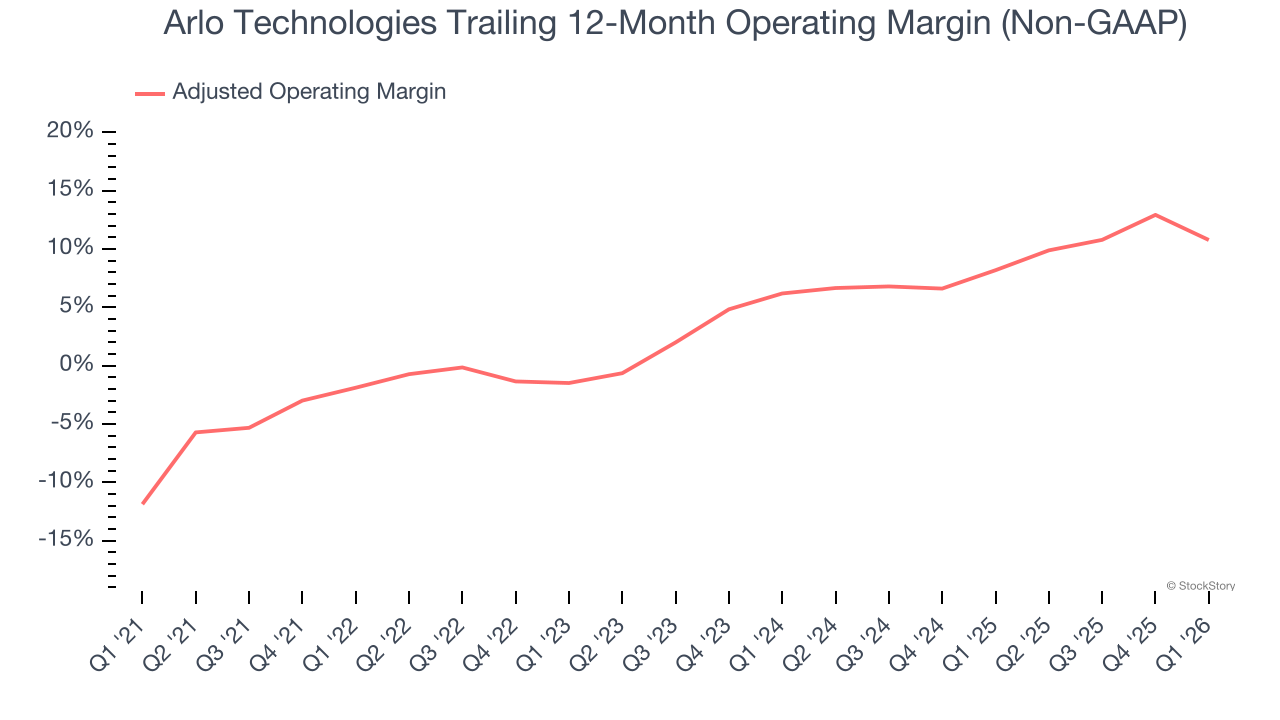

- Operating Margin: 5%, up from -1.2% in the same quarter last year

- Free Cash Flow Margin: 16.9%, down from 23.6% in the same quarter last year

- Market Capitalization: $1.59 billion

Company Overview

Originally spun off from networking equipment maker Netgear in 2018, Arlo Technologies (NYSE:ARLO) provides cloud-based smart security devices and subscription services that help consumers and businesses monitor and protect their homes, properties, and loved ones.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $560.6 million in revenue over the past 12 months, Arlo Technologies is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

As you can see below, Arlo Technologies’s 8.4% annualized revenue growth over the last five years was solid. This is a good starting point for our analysis because it shows Arlo Technologies’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Arlo Technologies’s annualized revenue growth of 5.4% over the last two years is below its five-year trend, but we still think the results were respectable.

This quarter, Arlo Technologies reported robust year-on-year revenue growth of 26.3%, and its $150.4 million of revenue topped Wall Street estimates by 7.6%. Company management is currently guiding for a 15.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.8% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

Arlo Technologies was profitable over the last five years but held back by its large cost base. Its average adjusted operating margin of 4.6% was weak for a business services business.

On the plus side, Arlo Technologies’s adjusted operating margin rose by 12.7 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, Arlo Technologies generated an adjusted operating margin profit margin of 5%, down 8 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Arlo Technologies’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Arlo Technologies’s EPS grew at an astounding 54% compounded annual growth rate over the last two years, higher than its 5.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q1, Arlo Technologies reported adjusted EPS of $0.28, up from $0.15 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Arlo Technologies’s full-year EPS of $0.83 to shrink by 1.9%. This is unusual as its revenue and operating margin are anticipated to increase, signaling the fall likely stems from "below-the-line" items such as taxes.

Key Takeaways from Arlo Technologies’s Q1 Results

It was good to see Arlo Technologies beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 11.6% to $16.64 immediately following the results.

Indeed, Arlo Technologies had a rock-solid quarterly earnings result, but is this stock a good investment here? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

/AI%20(artificial%20intelligence)/AI%20engineer%20working%20on%20laptop%20by%20ART%20STOCK%20CREATIVE%20via%20Shutterstock.jpg)

/Qualcomm%2C%20Inc_%20logo%20on%20phone-by%20viewimage%20via%20Shutterstock.jpg)

/Advanced%20Micro%20Devices%20Inc_%20logo%20and%20chart%20data-by%20Poetra_%20RH%20via%20Shutterstock.jpg)

/Micron%20Technology%20Inc_billboard-by%20Poetra_RH%20via%20Shutterstock.jpg)