/Apple%20Inc%20logo%20on%20Apple%20store-by%20PhillDanze%20via%20iStock.jpg)

A lot of noise surrounds Apple (AAPL) at the moment. First of all, the company is set to undergo a massive leadership change, as Tim Cook steps down as CEO this September after leading the company for 15 years.

Meanwhile, the company is going through a memory supply crunch, which is not exclusive to Apple. Cook believes memory costs will drive “increasing impact” on Apple’s business. He assured that the company was exploring possible solutions, ranging from raising prices to signing longer supply agreements.

Despite this, Apple reported solid Q2 FY26 earnings and increased its cash dividend by 4% to $0.27 per share (translating to an annual dividend rate of $1.08 and yielding 0.38% on current prices). Shareholders of record at the close of business on May 11 will receive the dividend payable on May 14. Further, the company declared an additional program to repurchase up to $100 billion of its common stock.

We take a deeper look at Apple at this juncture.

About Apple Stock

A global technology titan, Apple operates seamlessly across hardware, software, and services to deliver innovative products like iPhones, Macs, and its booming Services ecosystem to billions of active devices worldwide. It dominates consumer tech.

Apple's AI ambitions shine through Apple Intelligence, pioneering on-device processing for privacy-focused features in Siri and apps, positioning it as a leader in edge AI innovation. Headquartered in Cupertino, California, Apple commands a massive market capitalization of $4.17 trillion, making it the third-largest company in the world.

The company’s stock has held strong on Wall Street, on the backs of strong iPhone demand, especially the iPhone 17 series, and robust Services revenue, combined with expanding Mac sales. Over the past 52 weeks. Apple’s stock has been up 44.88%. It has gained modestly by 5.79% year-to-date (YTD) amid tariff-related pressures, which have fueled volatility and investor skepticism.

On a forward-adjusted basis, its price-to-earnings (non-GAAP) ratio of 31.76 times is higher than the industry average of 24.08 times.

Apple Crushed Q2 FY26 on iPhone Surge and Services Strength

Fueled by a swelling demand for its iPhone 17 lineup, Apple reported the best second-quarter results (the quarter ended in March). The company’s revenue increased by 16.6% year-over-year (YOY) to $111.18 billion, which was higher than the $109.48 billion that Wall Street analysts had expected. The majority of this growth was driven by a 21.7% YOY surge in iPhone sales to $56.99 billion and a 16.3% growth in Services revenue to $30.98 billion.

Apple is also recognizing higher profitability as its Services business grows (as the business is high-margin). The company’s EPS for the second fiscal quarter was $2.01, up 21.8% YOY, and higher than the $1.92 that Street analysts had expected.

Apple’s stock surged 3.24% intraday on May 1 after the company’s solid Q2 results rolled in. This was also aided by the company’s robust guidance. For the third quarter (ending in June), Apple expects its revenue to grow between 14% and 17% YOY, topping analysts’ projections of a 9.5% growth.

Wall Street analysts are robustly optimistic about Apple’s future earnings. For the current fiscal year, EPS is projected to surge 17% annually to $8.73, followed by a 9.2% growth to $9.53 in the next fiscal year. Analysts also expect the company’s EPS to grow by 18.5% YOY to $1.86 for the third quarter of fiscal 2026.

What Do Analysts Think About Apple’s Stock?

Following Apple’s blockbuster Q2 earnings, Wall Street analysts have reiterated their stances, though they now favor larger upside than before. Wells Fargo analyst Aaron Rakers maintained an “Overweight” rating on the stock and raised the price target from $300 to $310, citing the company’s better-than-expected results and guidance.

TD Cowen analysts also maintained a “Buy” rating and hiked the price target from $325 to $335, citing Apple’s solid guidance that reflected strong underlying demand for its iPhone and Mac products. The firm’s analysts also believed that while the company faces a chip supply drought and memory cost inflation, it has the option to absorb some near-term costs, increase future product prices, and put its balance sheet to strategic use.

On the other hand, Barclays analysts maintained an “Underweight” rating on Apple’s stock but raised the price target from $248 to $253, citing an improved revenue outlook. Analysts at the firm also expressed concern about the supply constraints and increasing memory prices, which are expected to affect Apple’s results. UBS analyst David Vogt kept a “Neutral” rating on the stock, while raising the price target from $287 to $296.

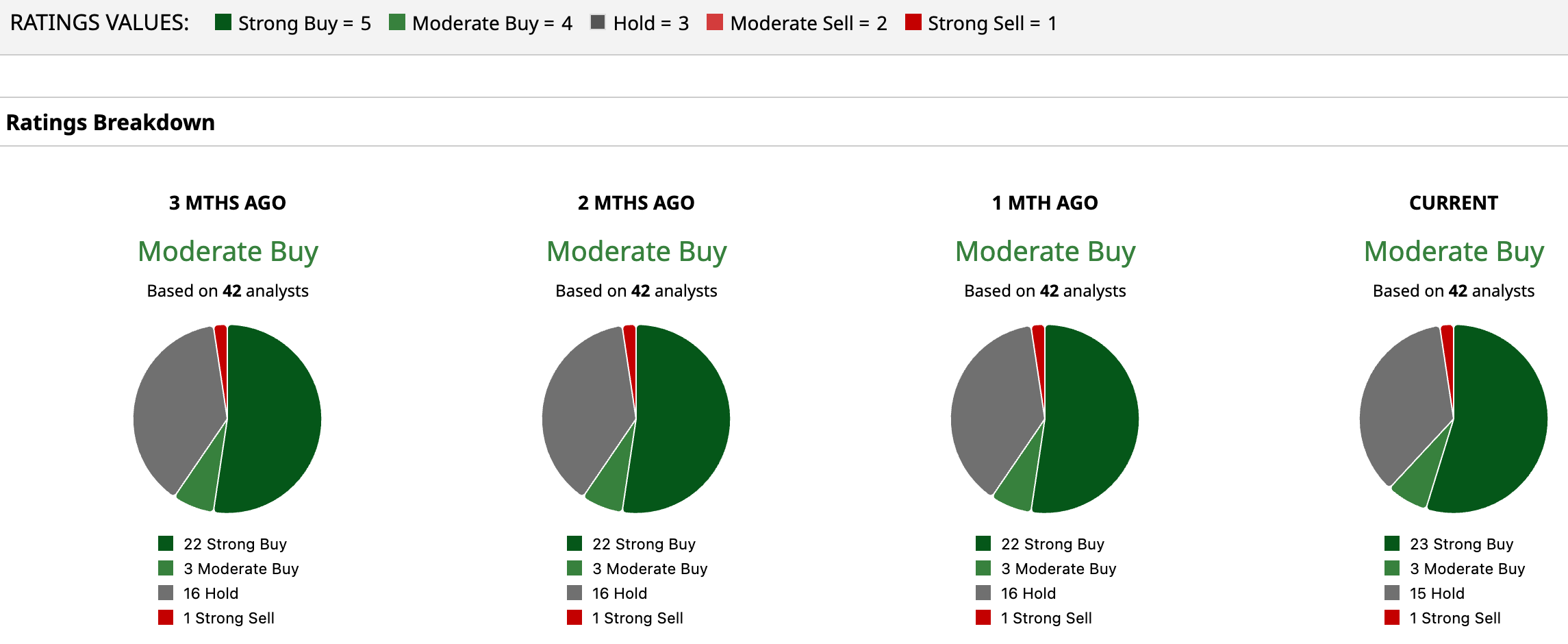

Apple has long been a popular name on Wall Street, with analysts awarding it a consensus “Moderate Buy” rating overall. Of the 42 analysts rating the stock, 23 have given it a “Strong Buy” rating, three a “Moderate Buy,” 15 a “Hold,” and one a “Strong Sell.” The consensus price target of $300.46 represents a 4.4% upside from current levels. Moreover, the Street-high price target of $350 implies a 21.6% upside.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Intel%20Corp_%20logo%20on%20mobile%20phone-by%20Piotr%20Swat%20via%20Shutterstock.jpg)

/Starbucks%20Corp_%20logo%20by-%20eyewave%20via%20iStock.jpg)