/CPU%20Chip.jpg)

ACM Research (ACMR) is a premier developer and manufacturer of wet processing equipment for the global semiconductor industry. The company specializes in single-water wet cleaning technology to remove contaminants and defects, resulting in an improved product yield for integrated circuit (IC) manufacturers. The company operates primarily through its subsidiary, ACM Research Shanghai, serving logic foundries across North America and the Asian subcontinent.

Founded in 1998, the company is headquartered in Fremont, California.

ACM Research Stock

ACM Research's stock has demonstrated remarkable resilience and growth, delivering a 175% total return over the past year. However, recent performance has been characterized by high volatility. While the shares have surged 29% in the last month leading up to their Q1 earnings, they remain about 25% down from their 52-week high of $71.65.

Compared with the Nasdaq Composite ($NASX), ACM Research has delivered significant alpha for growth-oriented investors. While the tech-heavy Nasdaq Composite gained roughly 42% over the last twelve months, ACMR’s 175% surge outperformed the index by more than fourfold. While the Nasdaq faced headwinds from fluctuating interest rates in early 2026, ACM's specialized focus on the semiconductor capital equipment cycle allowed it to decouple from the index during periods of sector-specific expansion.

ACM Research Q1 Preliminary Results Set the Tone

ACM Research is scheduled to release its full first-quarter 2026 financial results on May 7, 2026, but preliminary data released on April 27 has already set a bullish tone. The company expects Q1 revenue between $225 million and $230 million, representing a robust year-over-year growth of 31% to 33%. This projection comfortably exceeds the prior analyst consensus of $216 million.

Even more impressive is the shipment data, with total first-quarter shipments anticipated to reach between $233 million and $238 million, a massive 49% to 52% increase compared to the same period in 2025. These figures suggest that the company is successfully navigating the transition from older cleaning nodes to advanced AI-compatible hardware.

Management has reaffirmed its full-year 2026 revenue guidance of $1.08 billion to $1.175 billion, projecting annual growth of 20% to 30%. Despite a disappointing Q4 2025 where EPS of $0.25 missed expectations, the company is doubling down on its "total system solutions" strategy, including new shipments of PECVD systems and advanced furnace tools. As the company prepares for a potential Hong Kong listing of its Shanghai subsidiary, investors will be watching for updates on margin stabilization amidst rising R&D costs associated with their new AI-native equipment lines.

ACMR Receives Fresh Coverage

Seaport Research Partners recently initiated coverage on the wafer fabrication equipment (WFE) sector with a "Buy" rating for ACM Research, assigning it a $75 price target, signaling an upside of 42% from the market price. Senior analyst Jay Goldberg highlighted that the industry is currently experiencing one of its strongest cycles in history, driven by an insatiable demand for AI compute capacity and trailing-edge fab expansion. While hyperscalers scramble for GPUs, the underlying bottleneck remains fab capacity, leading to record-breaking capital expenditure budgets for WFE tools.

Specifically for ACM Research, Seaport notes the company’s strategic advantage in the rapidly growing Chinese semiconductor market. Although headquartered in Fremont, California, ACM Research sells over 90% of its products in the PRC and has established significant local operations that may shield it from escalating geopolitical export controls.

The firm is well-positioned to leverage its dominant domestic share and current profitability to fund global export ambitions, having already begun winning orders for fabs in other countries. Seaport expects this robust growth cycle, bolstered by sectors like robotics and automotive alongside AI, to persist for several more years before any significant downturn occurs.

Should You Bet on ACMR Stock?

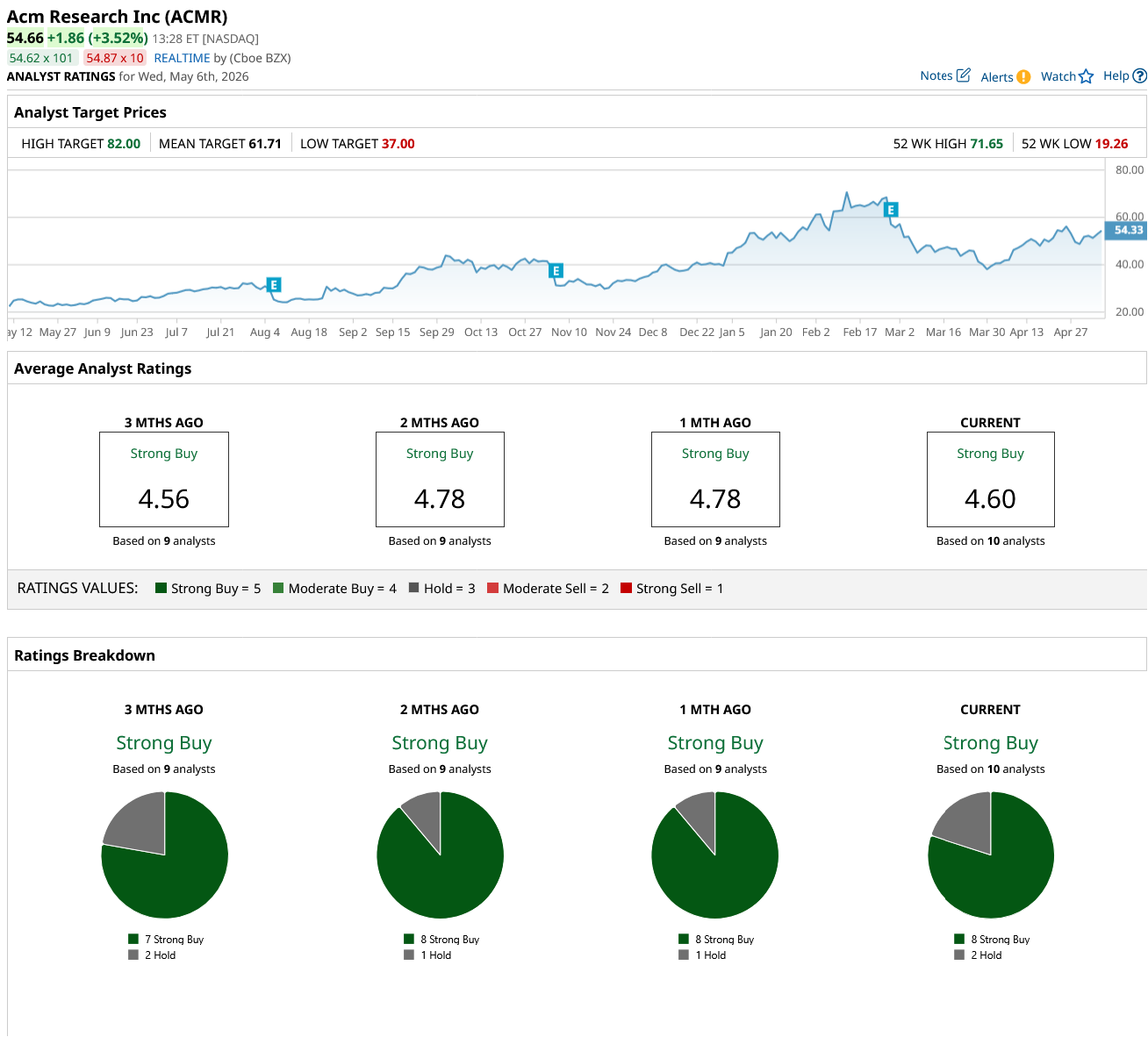

Despite the geopolitical complexities highlighted by Seaport Research, ACM Research remains a high-conviction growth play within the semiconductor cleaning sector. The stock currently holds a consensus "Strong Buy" rating, supported by eight "Strong Buy" ratings and two "Holds" from ten analysts. With a mean price target of $61.71, ACMR offers a projected 13% upside from its current market price.

As the company leverages its strong PRC presence to fund global expansion, Seaport’s aggressive $75 target further underscores the significant alpha potential for investors looking to capitalize on the ongoing AI-driven fab expansion cycle.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

/Uber%20Technologies%20Inc%20logo%20outside%20offices-by%20Sundry%20Photography%20via%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Space%20Technology%20by%20Rini_%20com%20via%20Shutterstock.jpg)