It’s not difficult to understand why many investors are enthused about uranium specialist NexGen Energy (NXE). With the Iran conflict imposing massive uncertainties regarding economic stability and reliable supply chains, there’s a vested interest in securing critical resources from western partners. Not surprisingly, NXE stock has gained about 32% on a year-to-date basis while also attracting an 88% Strong Buy rating from the Barchart Technical Opinion indicator.

Fundamentally, one of the biggest catalysts centers on regulatory clearance. According to NexGen’s website, on March 5 of this year, the Canadian Nuclear Safety Commission (CNSC) granted the final federal license required to begin site preparation and construction. As such, NexGen has officially entered a 48-month construction cycle, aiming to become a major global uranium producer by the end of this decade.

Further, the above development has come at a rather fortuitous time. As stated earlier, geopolitical tensions have shined a bright spotlight on secure, reliable energy sources, thus increasing the strategic value of the underlying Canadian uranium asset. In addition, governments in China, India and Europe are aggressively accelerating nuclear energy capacity to enhance energy security, along with key environmental, social and governance (ESG) metrics.

By reasonable inference, it appears that it’s a green light to buy NXE stock without reservation. The problem? The smart money seems to have other ideas.

Volatility Skew Suggests Structural Fear Toward NXE Stock

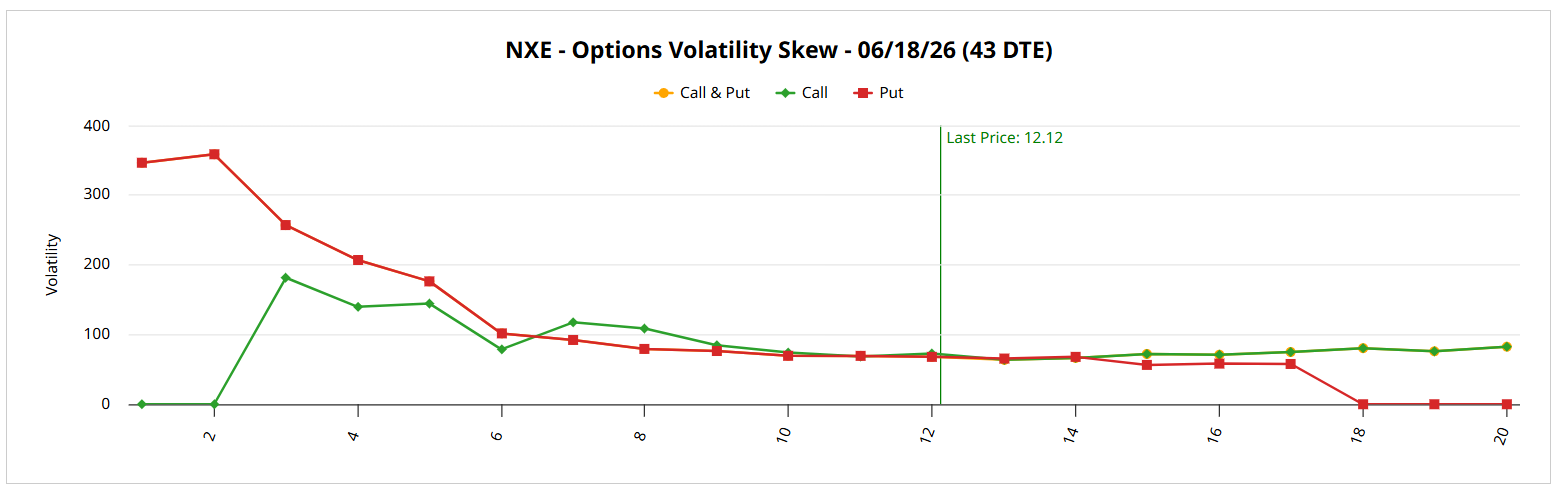

While there’s no one indicator that answers all questions regarding the equities market, the volatility skew represents one of the most important gauges of smart money sentiment. By definition, the skew reveals the implied volatility (IV) of the entire strike price spectrum of a specific options chain.

In simple terms, this screener acts as an insurance market. Sophisticated market participants may hedge their bets or acquire greater leverage for upside wagers. By understanding where the insurance premium is hottest, so to speak, we can better assess the main concern among smart money traders.

For the June 18 expiration date, the predominant expression of the volatility skew appears to be downside protection. Essentially, the left tail (south of the current spot price) swings sharply higher for put IV, suggesting that the market is pricing for a severe devaluation event as a possible tail risk scenario.

It raises the question: why would Wall Street be so worried about a meltdown in NXE stock? If I had to guess, investors may be fretting about the coming financial sledgehammer.

Sure, it’s fantastic news that NexGen is transitioning to a 48-month construction phase. However, this cycle will almost certainly require massive capital, perhaps running into the billions. As such, the skew’s bearish hedge may be focused on a massive equity dilution. If the company needs to raise more cash than expected at a lower stock price, current shareholders will likely get crushed.

We’ve seen these types of moves happen before — and it’s never pretty. Therefore, the slanted skew may very well be a common-sense tactic.

Why Bearishness Might Not Be a Great Idea Here

At this point, followers of the smart money may be thinking of placing a debit-side bearish bet against NXE stock — and frankly, that’s not an unreasonable proposition. However, there are two caveats to consider. First, the smart money isn’t automatically prescient. Just because these traders are buying more auto insurance doesn’t mean a car crash is necessarily imminent.

The second caveat? With the skew being tilted bearishly, the premiums for buying out-the-money (OTM) puts will be relatively higher than their OTM call counterparts on a volatility basis. Thus, if you have a reason to be contrarian (bullish), the calls would theoretically be discounted.

For me, the contrarian reason comes down to conditional probabilities. Using historical price data going back to January 2019, the chance that a random long position over a 10-week period will yield a positive return is 55.5%. Further, the median distribution over this period would be estimated to be around $11.80 to $13 (assuming a starting price of $12.12).

However, the distinct signal I’m looking at is the current 10-week setup. In the last 10 weeks, NXE stock printed only three up weeks, leading to an overall downward slope across the period. Under this specific circumstance, the exceedance ratio jumps to 69.6%. Additionally, the forward 10-week distribution would be estimated to land between $11 and $14.

It’s a probabilistic stretch but I’m looking at the speculative 13/14 bull call spread expiring June 18. Should NXE stock rise through the $14 strike at expiration, the maximum payout clocks in at nearly 186%. But the key point here is that the nominal cost per spread is only $35.

Because the smart money is clearly angling for downside protection, the opposite side of the trade offers an arguably tempting proposition.

On the date of publication, Josh Enomoto did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)