Infrastructure construction company Primoris (NYSE:PRIM) fell short of the market’s revenue expectations in Q1 CY2026, with sales falling 5.4% year on year to $1.56 billion. Its non-GAAP profit of $0.59 per share was 30.1% below analysts’ consensus estimates.

Is now the time to buy Primoris? Find out by accessing our full research report, it’s free.

Primoris (PRIM) Q1 CY2026 Highlights:

- Revenue: $1.56 billion vs analyst estimates of $1.74 billion (5.4% year-on-year decline, 10.3% miss)

- Adjusted EPS: $0.59 vs analyst expectations of $0.84 (30.1% miss)

- Adjusted EBITDA: $60.5 million vs analyst estimates of $92.93 million (3.9% margin, 34.9% miss)

- Management lowered its full-year Adjusted EPS guidance to $4.90 at the midpoint, a 16.9% decrease

- EBITDA guidance for the full year is $490 million at the midpoint, below analyst estimates of $569.3 million

- Operating Margin: 1.6%, down from 4.3% in the same quarter last year

- Free Cash Flow was -$150,400, down from $25.58 million in the same quarter last year

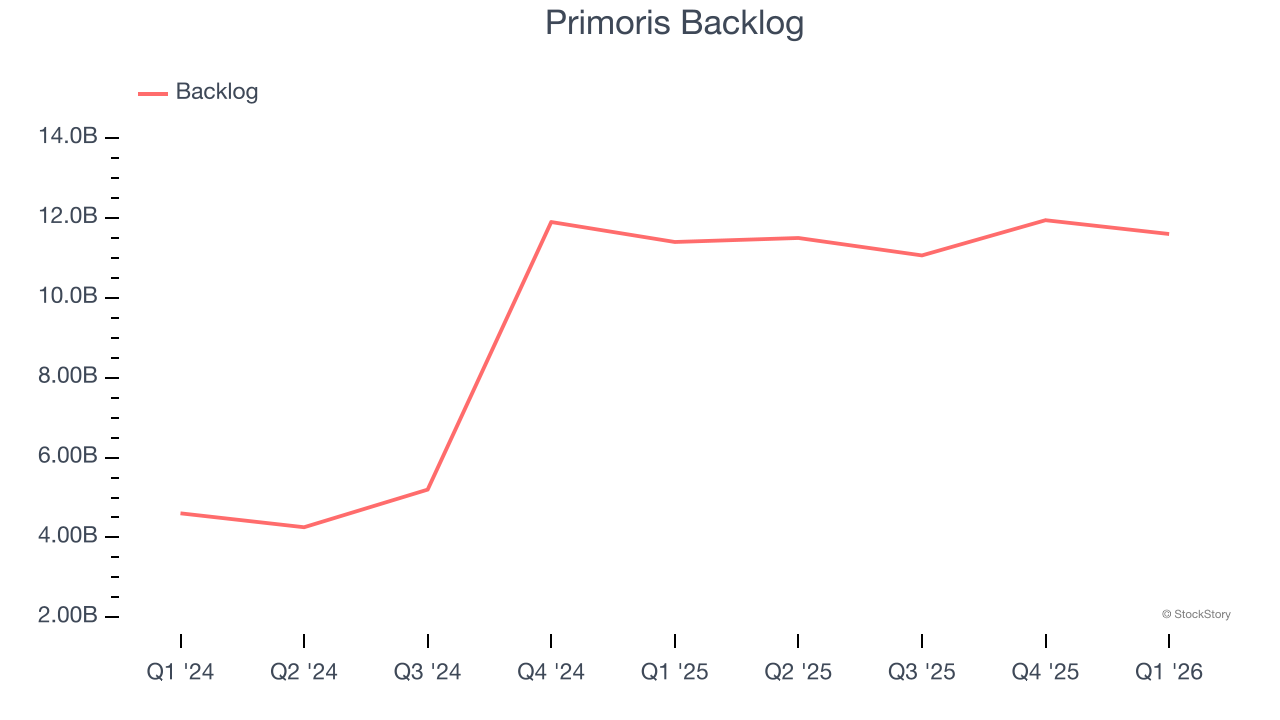

- Backlog: $11.6 billion at quarter end, up 1.8% year on year

- Market Capitalization: $11 billion

Company Overview

Listed on the NASDAQ in 2008, Primoris (NYSE:PRIM) builds, maintains, and upgrades infrastructure in the utility, energy, and civil construction industries.

Revenue Growth

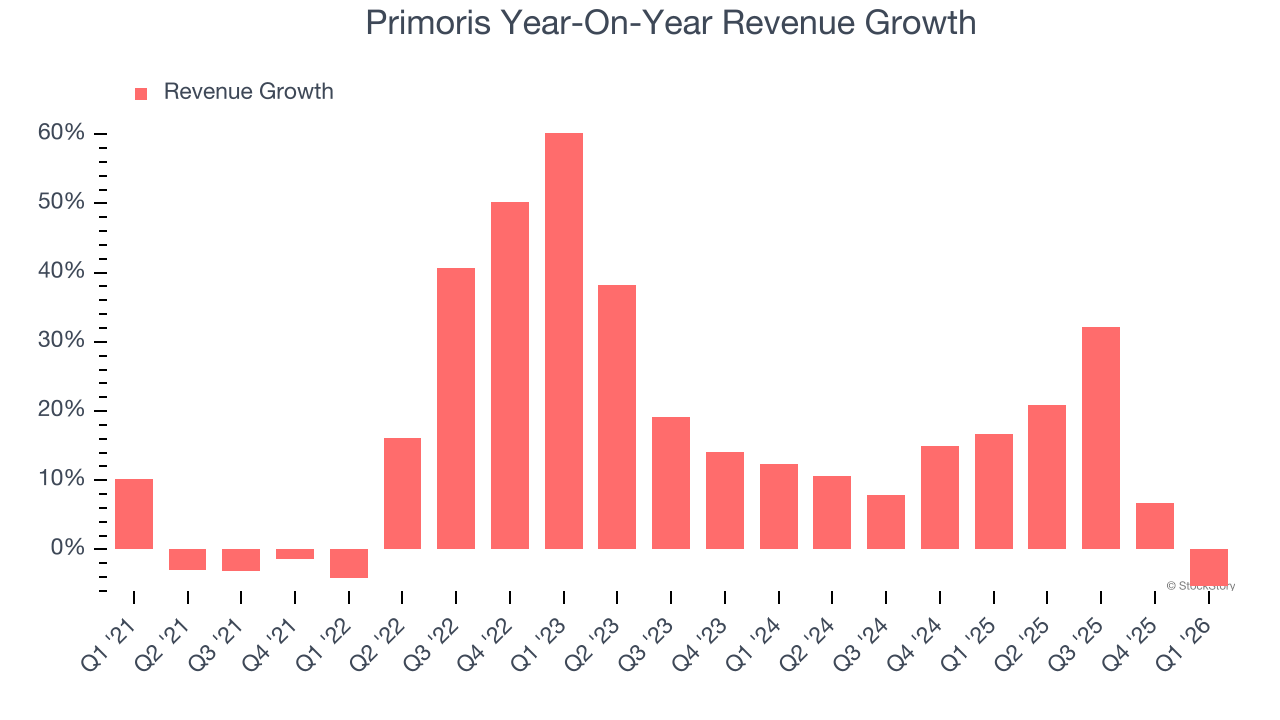

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Primoris’s 16% annualized revenue growth over the last five years was incredible. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Primoris’s annualized revenue growth of 12.9% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Primoris’s backlog reached $11.6 billion in the latest quarter and averaged 86.5% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Primoris’s products and services but raises concerns about capacity constraints.

This quarter, Primoris missed Wall Street’s estimates and reported a rather uninspiring 5.4% year-on-year revenue decline, generating $1.56 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 11.5% over the next 12 months, similar to its two-year rate. Still, this projection is admirable and indicates the market is baking in success for its products and services.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

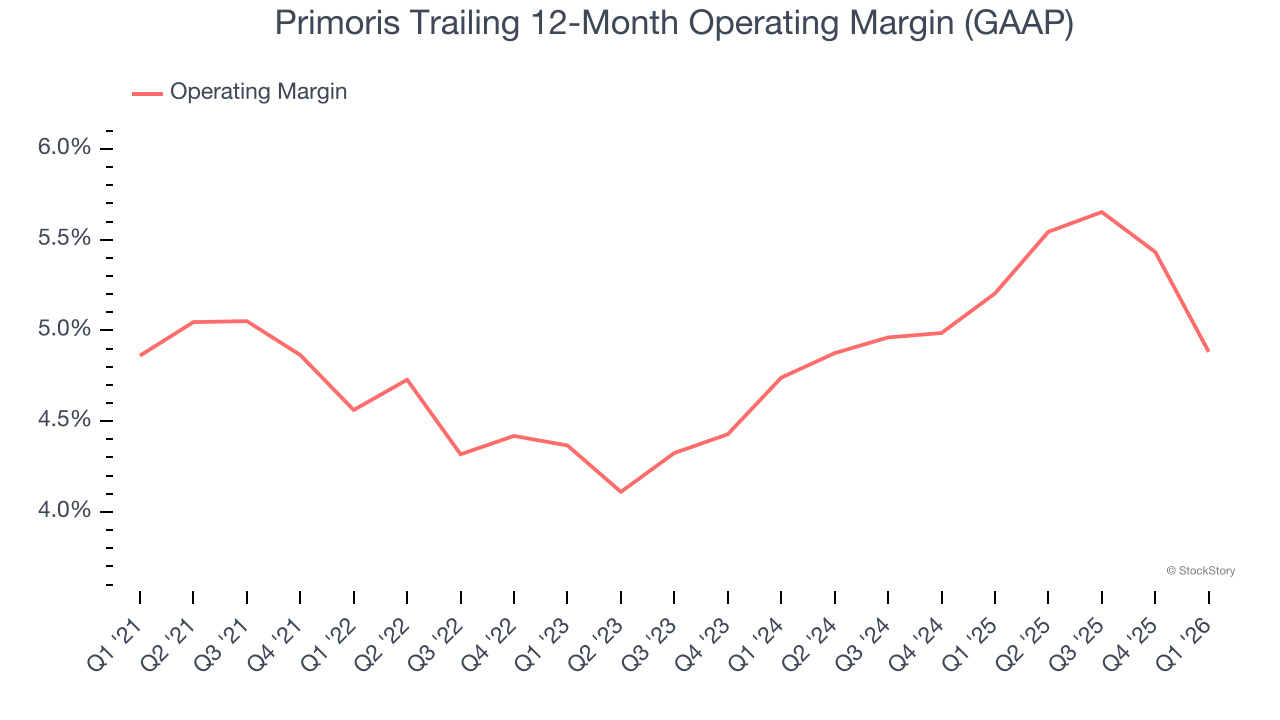

Primoris’s operating margin has generally stayed the same over the last 12 months, averaging 4.8% over the last five years. This profitability was lousy for an industrials business and caused by its suboptimal cost structureand low gross margin.

Analyzing the trend in its profitability, Primoris’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Primoris generated an operating margin profit margin of 1.6%, down 2.7 percentage points year on year. Since Primoris’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

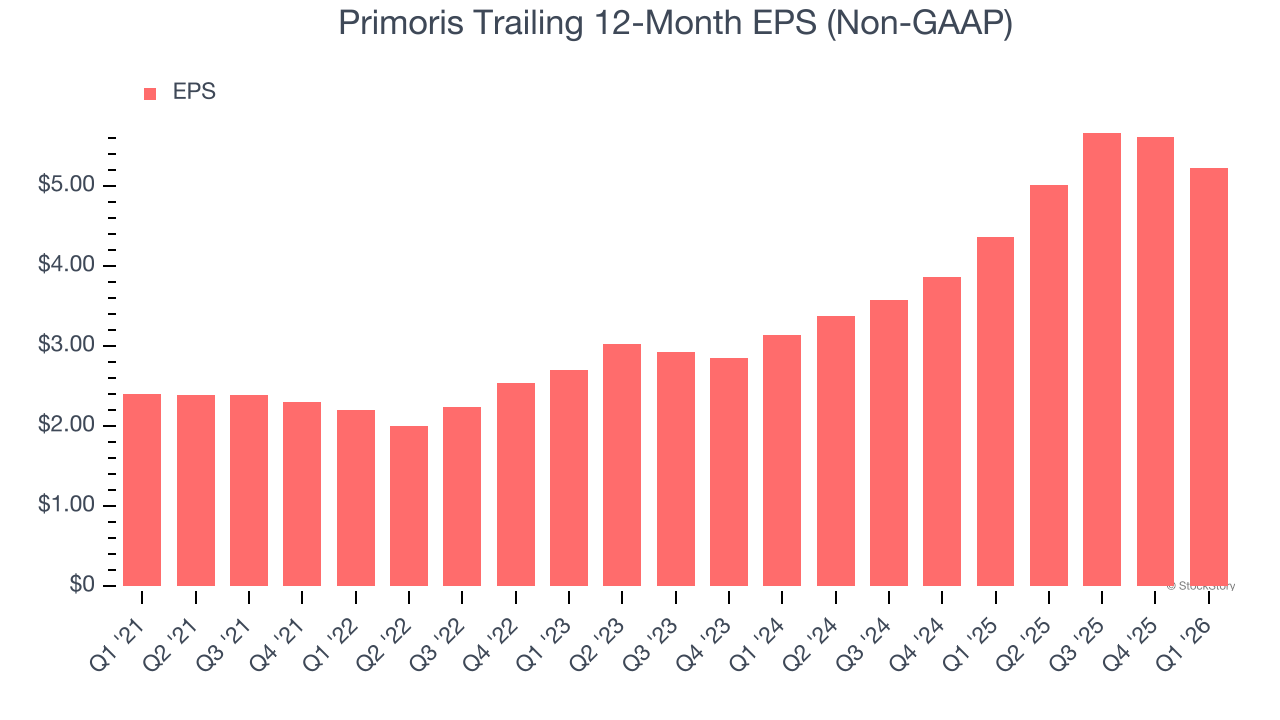

Primoris’s spectacular 16.8% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Primoris, its two-year annual EPS growth of 29.1% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q1, Primoris reported adjusted EPS of $0.59, down from $0.98 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Primoris’s full-year EPS of $5.23 to grow 17.9%.

Key Takeaways from Primoris’s Q1 Results

We struggled to find many positives in these results. Its full-year EBITDA guidance missed and its revenue fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 29.2% to $143.70 immediately following the results.

The latest quarter from Primoris’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).