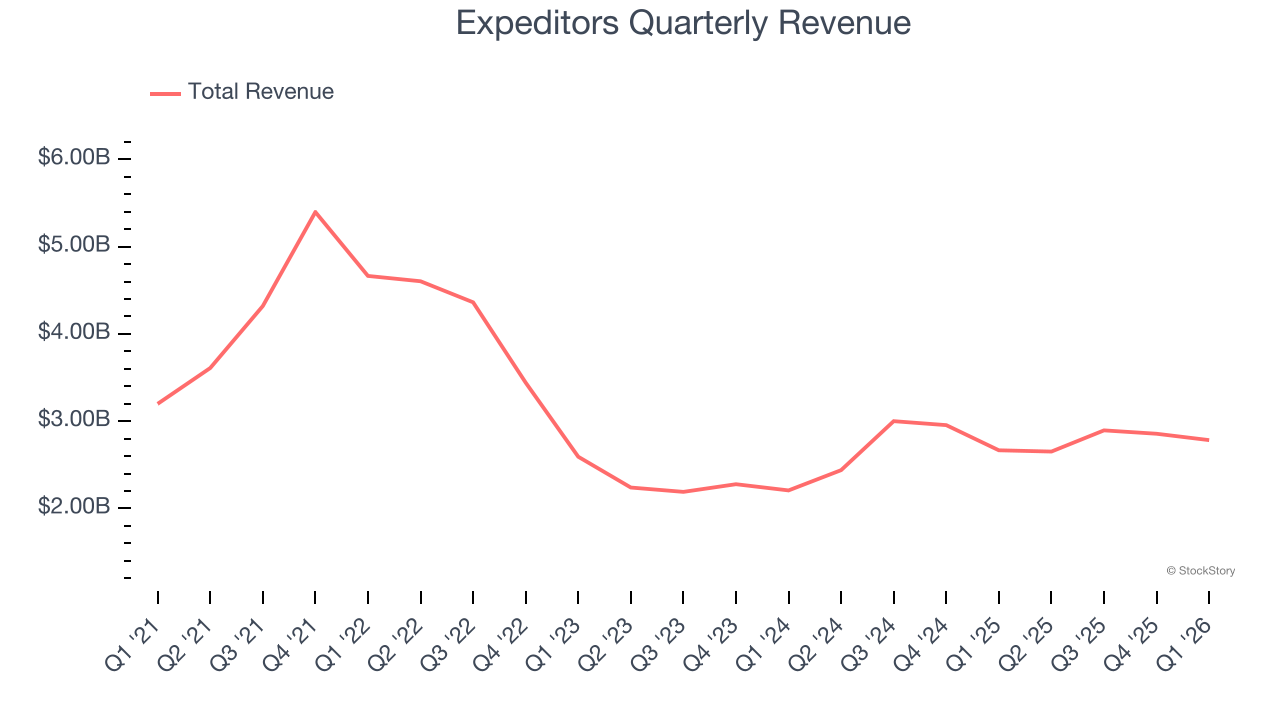

Logistics and freight forwarding company Expeditors (NYSE:EXPD) announced better-than-expected revenue in Q1 CY2026, with sales up 4.4% year on year to $2.78 billion. Its non-GAAP profit of $1.71 per share was 28.7% above analysts’ consensus estimates.

Is now the time to buy Expeditors? Find out by accessing our full research report, it’s free.

Expeditors (EXPD) Q1 CY2026 Highlights:

- Revenue: $2.78 billion vs analyst estimates of $2.61 billion (4.4% year-on-year growth, 6.5% beat)

- Adjusted EPS: $1.71 vs analyst estimates of $1.33 (28.7% beat)

- Adjusted EBITDA: $308.7 million vs analyst estimates of $246.5 million (11.1% margin, 25.2% beat)

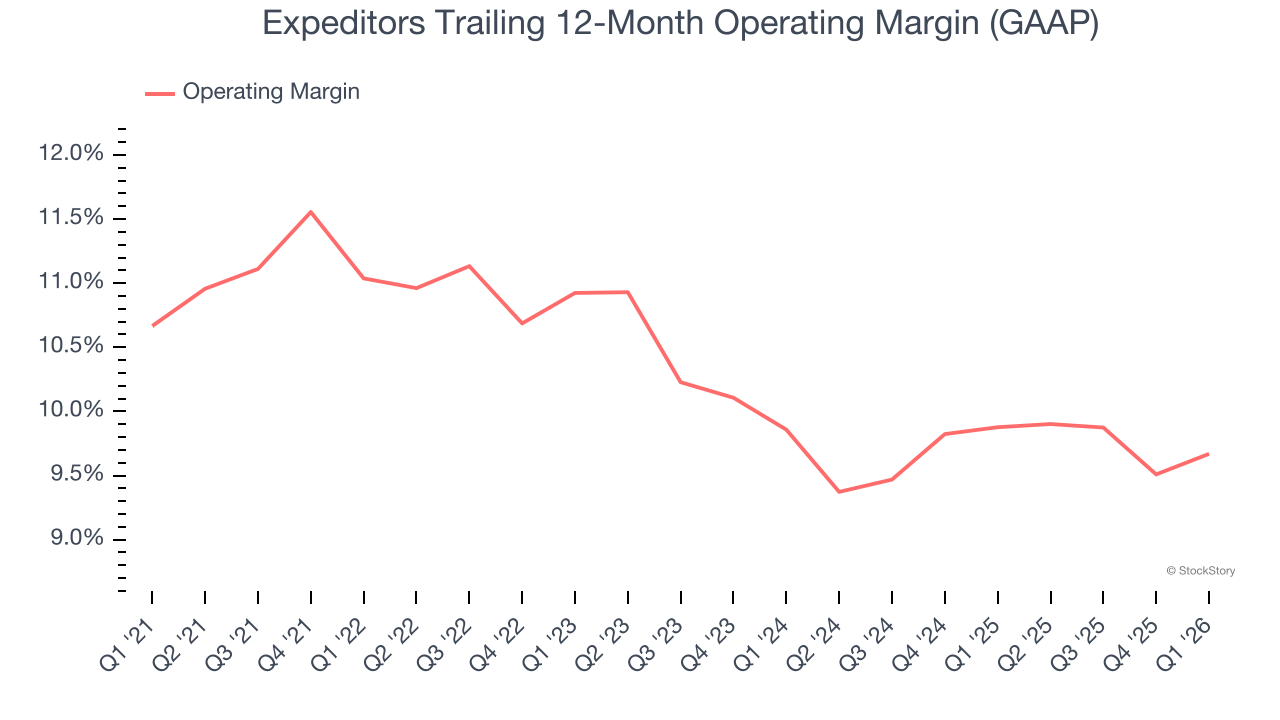

- Operating Margin: 10.6%, in line with the same quarter last year

- Free Cash Flow Margin: 10.7%, down from 12.4% in the same quarter last year

- Market Capitalization: $18.58 billion

BELLEVUE, Wash.--(BUSINESS WIRE)--Expeditors International of Washington, Inc. (NYSE:EXPD) today announced that on May 4, 2026 its Board of Directors declared a semi-annual cash dividend of $0.81 per share, payable on June 15, 2026 to shareholders of record as of June 1, 2026. “Since 2024, we have returned nearly $2 billion to shareholders in dividends and share repurchases,” said David A. Hackett, Senior Vice President and Chief Financial Officer.

Company Overview

Expeditors (NYSE:EXPD) offers air and ocean freight as well as brokerage services.

Revenue Growth

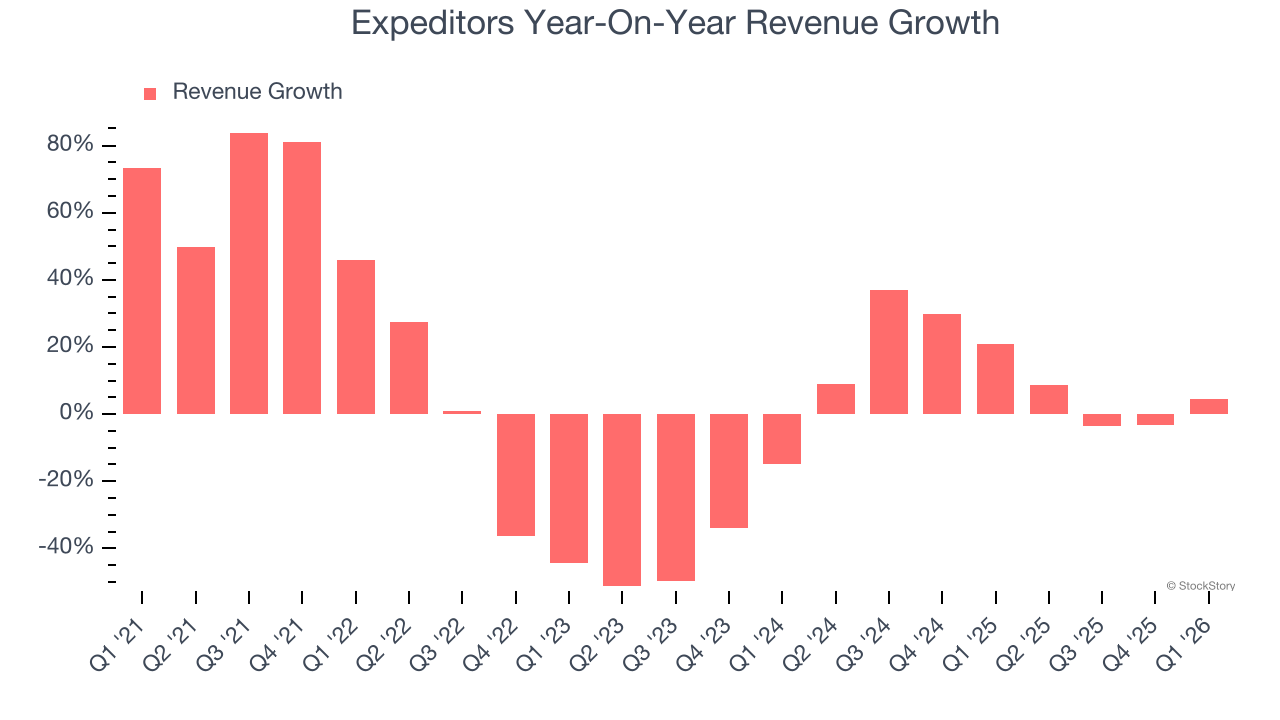

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Unfortunately, Expeditors struggled to consistently increase demand as its $11.19 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and suggests it’s a lower quality business.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Expeditors’s annualized revenue growth of 12% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

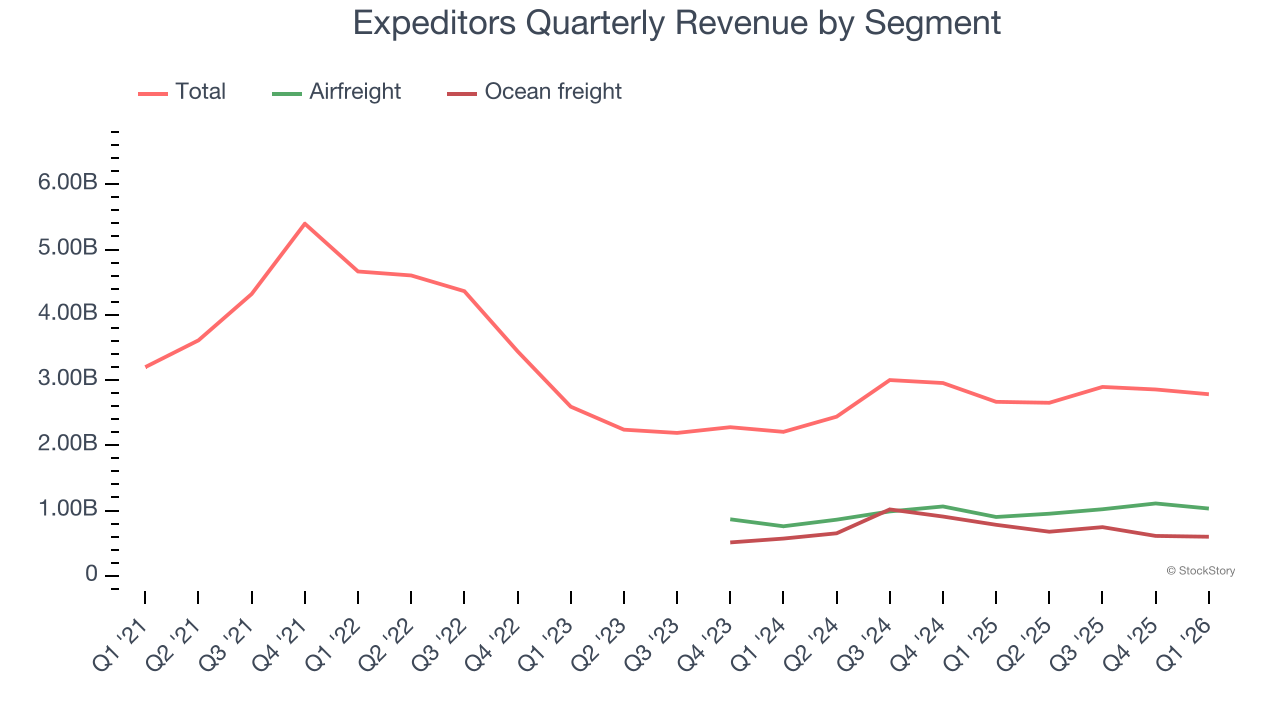

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Airfreight and Ocean freight, which are 37% and 21.5% of revenue. Over the last two years, Expeditors’s Airfreight revenue (transport by plane) averaged 12.4% year-on-year growth while its Ocean freight revenue (transport by sea) averaged 5.9% growth.

This quarter, Expeditors reported modest year-on-year revenue growth of 4.4% but beat Wall Street’s estimates by 6.5%.

Looking ahead, sell-side analysts expect revenue to grow 5.7% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

Expeditors has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 10.4%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, Expeditors’s operating margin decreased by 1.4 percentage points over the last five years. Even though its historical margin was healthy, shareholders will want to see Expeditors become more profitable in the future.

This quarter, Expeditors generated an operating margin profit margin of 10.6%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

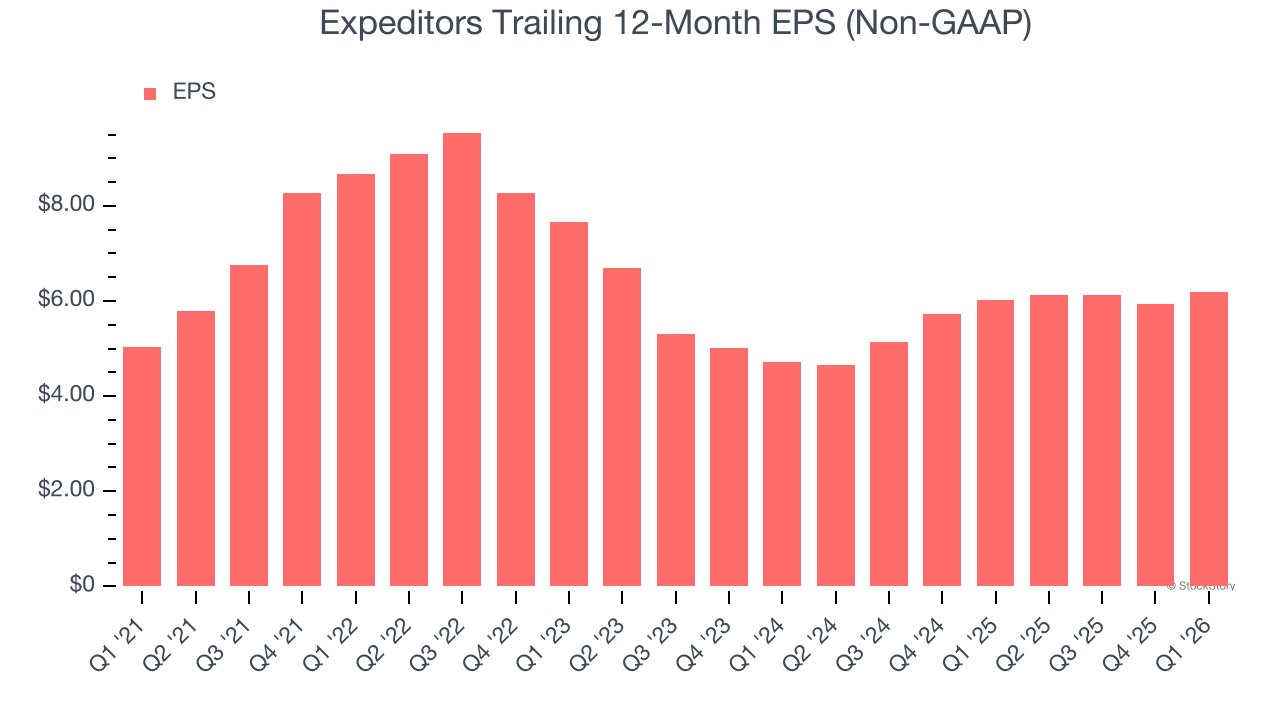

Expeditors’s EPS grew at 4.2% compounded annual growth rate over the last five years. This performance was better than its flat revenue but doesn’t tell us much about its business quality because its operating margin didn’t improve.

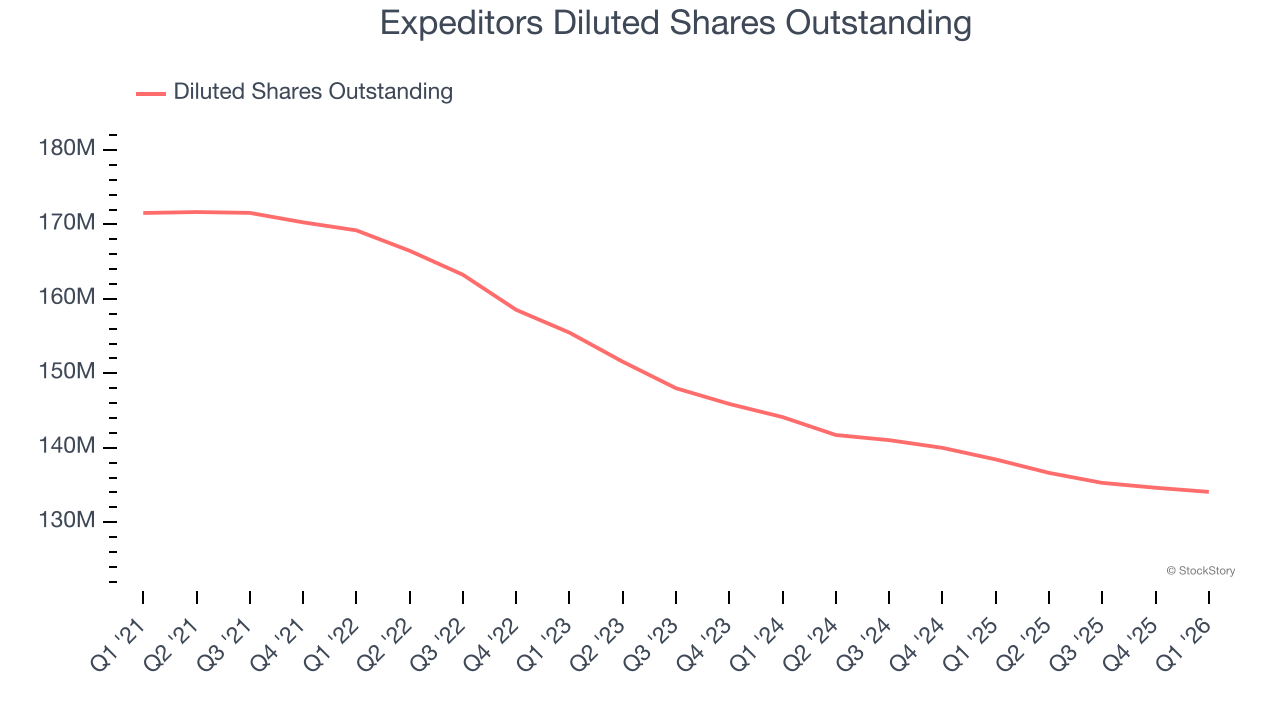

Diving into the nuances of Expeditors’s earnings can give us a better understanding of its performance. A five-year view shows that Expeditors has repurchased its stock, shrinking its share count by 21.8%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Expeditors, its two-year annual EPS growth of 14.4% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q1, Expeditors reported adjusted EPS of $1.71, up from $1.47 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Expeditors’s full-year EPS of $6.18 to grow 3.8%.

Key Takeaways from Expeditors’s Q1 Results

It was good to see Expeditors beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. Investors were likely hoping for more, and shares traded down 2% to $150 immediately following the results.

Should you buy the stock or not? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

/Microsoft%20sign%20at%20the%20headquarters%20by%20VDB%20Photos%20via%20Shutterstock.jpg)

/Space/Cargo%20spacecraft%20in%20low-Earth%20orbit%20by%20Paopano%20via%20Shutterstock.jpg)