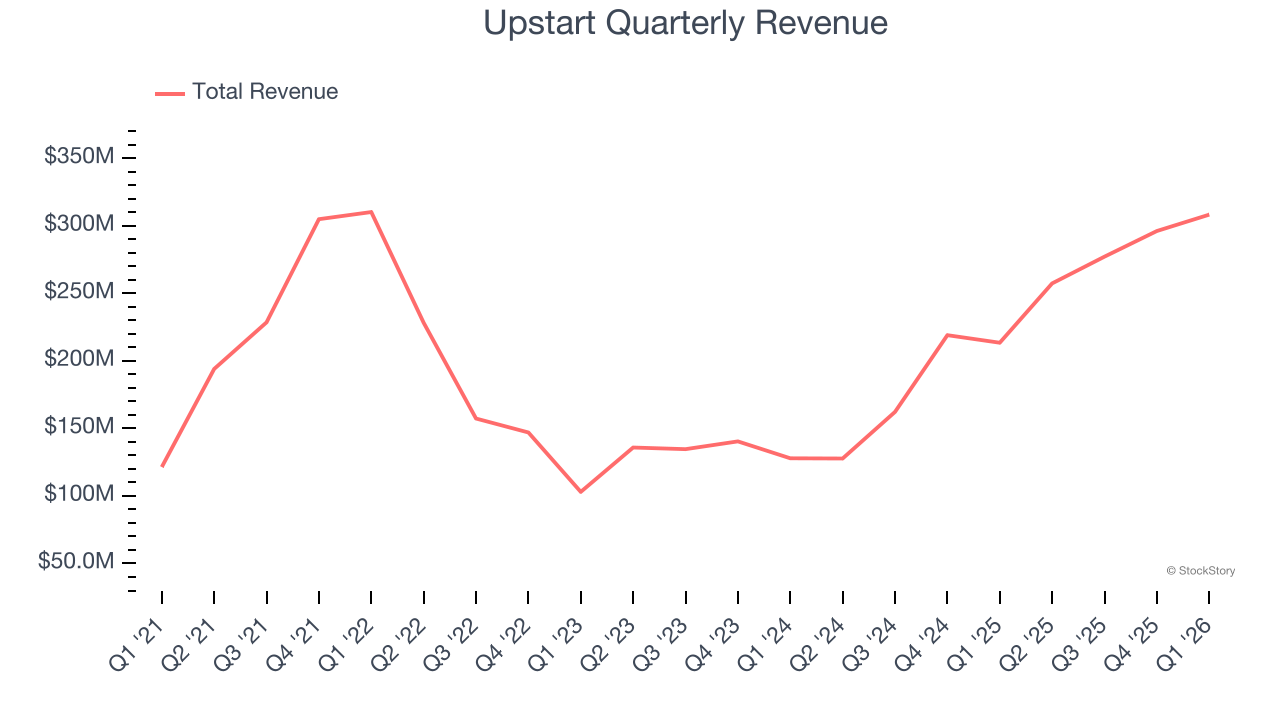

AI lending platform Upstart (NASDAQ:UPST) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 44.4% year on year to $308.2 million. On the other hand, the company’s full-year revenue guidance of $1.4 billion at the midpoint came in 0.9% below analysts’ estimates. Its GAAP loss of $0.07 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Upstart? Find out by accessing our full research report, it’s free.

Upstart (UPST) Q1 CY2026 Highlights:

- Revenue: $308.2 million vs analyst estimates of $303.1 million (44.4% year-on-year growth, 1.7% beat)

- EPS (GAAP): -$0.07 vs analyst estimates of $0.12 (significant miss)

- Adjusted Operating Income: $27.29 million vs analyst estimates of $12.76 million (8.9% margin, significant beat)

- The company reconfirmed its revenue guidance for the full year of $1.4 billion at the midpoint

- Operating Margin: -2.4%, in line with the same quarter last year

- Free Cash Flow was -$140.3 million, down from $96.83 million in the previous quarter

- Market Capitalization: $3.07 billion

Company Overview

Using over 2,500 data variables and trained on nearly 82 million repayment events, Upstart (NASDAQ:UPST) is an AI-powered lending platform that uses machine learning to help banks and credit unions more accurately assess borrower risk for personal loans, auto loans, and home equity lines of credit.

Revenue Growth

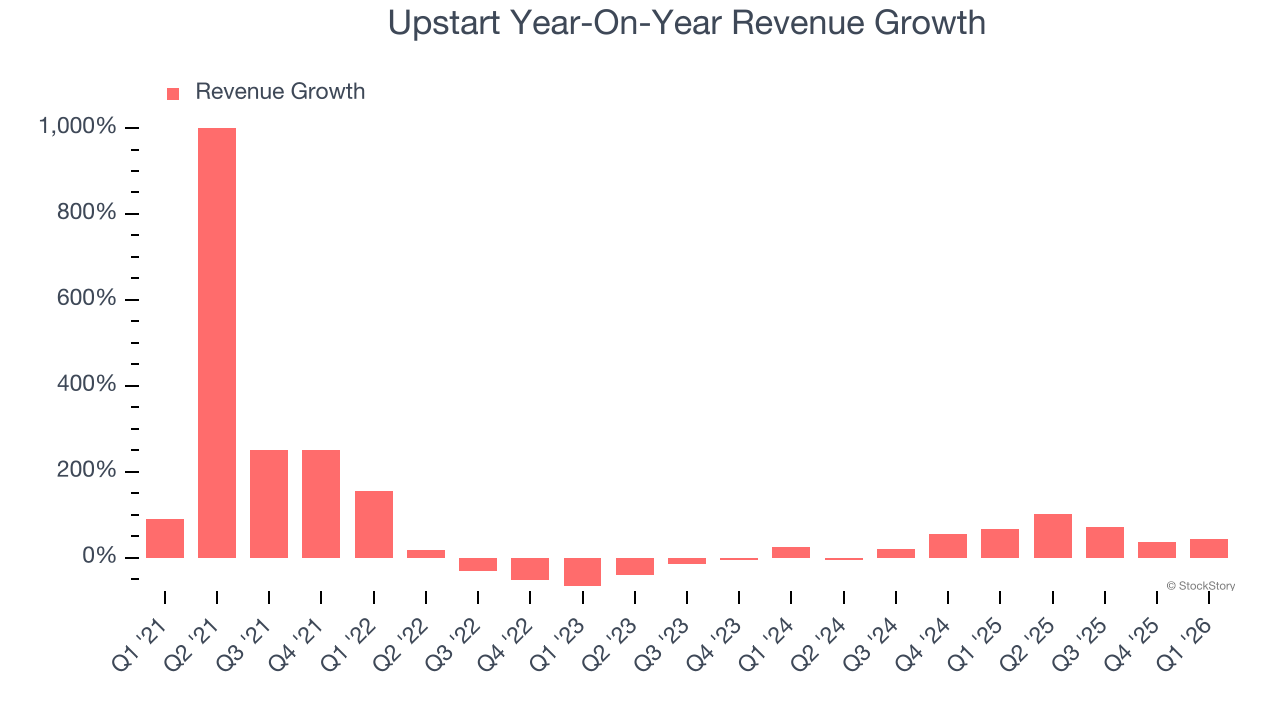

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Upstart’s 31.4% annualized revenue growth over the last five years was excellent. Its growth beat the average software company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Upstart’s annualized revenue growth of 45.4% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, Upstart reported magnificent year-on-year revenue growth of 44.4%, and its $308.2 million of revenue beat Wall Street’s estimates by 1.7%.

Looking ahead, sell-side analysts expect revenue to grow 33.4% over the next 12 months, a deceleration versus the last two years. Still, this projection is admirable and suggests the market is forecasting success for its products and services.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

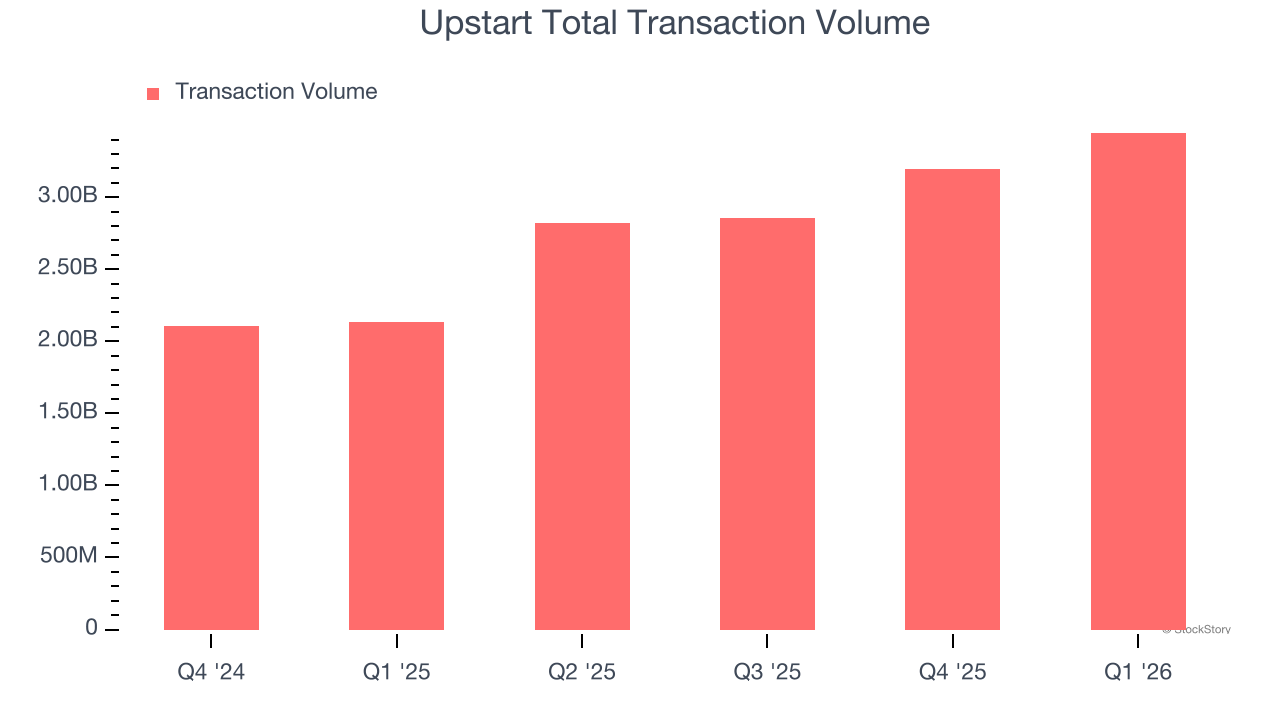

Total Transaction Volume

Total transaction volumes show the aggregate dollar value of loans processed on Upstart’s platform. This is the number from which the company will ultimately collect fees, and the higher it is, the more accurate its software becomes at assessing credit risk.

Upstart’s transaction volume punched in at $3.45 billion in Q1, and over the last four quarters, its growth was fantastic as it averaged 56.6% year-on-year increases. This performance aligned with its total sales growth and shows the company is capturing significant demand. It also indicates that customers are increasingly using Upstart’s platform to process loans, enabling it to collect more fees and expand into new markets (like credit cards).

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Upstart is extremely efficient at acquiring new customers, and its CAC payback period checked in at 11.2 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Upstart more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

Key Takeaways from Upstart’s Q1 Results

It was encouraging to see Upstart beat analysts’ revenue and adjusted operating profit expectations this quarter. On the other hand, its full-year revenue guidance fell slightly short of Wall Street’s estimates. This outlook is weighing on shares. The stock traded down 13.3% to $27.06 immediately following the results.

Upstart underperformed this quarter, but does that create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).