/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)

For years, SoFi Technologies (SOFI) has wrestled with an identity problem in the eyes of investors. Is it a digital bank that should be valued like a traditional financial institution — with modest multiples and cyclical sensitivity — or is it a technology-driven platform that deserves to trade more like a high-growth software company? CEO Anthony Noto recently made it clear where he stands on that debate.

On the latest earnings call, Noto once again highlighted SoFi’s performance against Wall Street’s famed “Rule of 40,” a benchmark most commonly associated with software companies. The metric, which combines revenue growth and profit margin, is widely used to assess whether a company is balancing expansion and profitability efficiently. By drawing attention to the Rule of 40, Noto is effectively signaling how he believes investors should value SoFi: not as a slow-growth lender, but as a diversified, tech-enabled financial services platform.

The question for investors now is whether the market will ultimately embrace that framing. With that, let’s take a closer look at what the numbers and the narrative are really telling us.

About SoFi Technologies Stock

SoFi Technologies is a financial services platform operating as a one-stop shop for digital financial products. It operates through its Lending, Technology Platform, and Financial Services segments, targeting high-credit-score consumers. The Lending segment is the foundation of its business, providing personal loans, student loan refinancing, and home loans. The Financial Services segment offers a suite of consumer products, including SoFi Checking and Savings, SoFi Invest (stock and robo-investing), and SoFi Credit Card. Finally, the Technology Platform segment provides B2B banking infrastructure through Galileo (payment processing) and Technisys (cloud-based core banking) to other financial institutions globally. SoFi's market capitalization currently stands at $20.9 billion.

Shares of the financial services company have slumped 38% on a year-to-date (YTD) basis. SOFI stock rallied last year, fueled by a string of strong quarterly earnings reports. However, the stock has failed to sustain that momentum this year due to a number of headwinds.

In March, short seller Muddy Waters Research issued a sharply critical report alleging that the company engaged in accounting manipulation. A lofty valuation and broader weakness across the fintech sector have also weighed on SOFI stock. Last week, shares cratered after the company issued below-consensus second-quarter revenue growth guidance and refrained from raising its full-year outlook.

Noto Argues SoFi Deserves Software-Like Valuation

Management used the recent earnings call to address at least one of the issues that has weighed on SOFI stock this year — its elevated valuation. CEO Anthony Noto highlighted that SoFi has now outperformed Wall Street’s well-known Rule of 40 benchmark for 18 consecutive quarters. By doing so, Noto signaled his belief that the market should value SoFi like a high-margin tech firm rather than a traditional, slower-growth bank.

The Rule of 40 is a software-as-a-service (SaaS) and venture capital principle stating that a company’s combined revenue growth rate and profit margin should exceed 40% to be considered “healthy.” It balances the trade-off between growing quickly and being profitable, with higher combined scores signaling premium valuation potential. Companies that consistently exceed the 40% threshold often command significantly higher revenue multiples, in some cases trading at roughly twice the sector’s median multiple.

In the latest quarter, SoFi posted a Rule of 40 score of 72%, underscoring the strength of its diversified business model and solid execution. The figure was calculated by combining 41% revenue growth with 31% adjusted EBITDA margins. Noto also pointed out that, while many companies are struggling, SoFi’s revenue growth continues to gain momentum. Overall, highlighting this metric is a deliberate effort to pivot investor focus toward SoFi’s operating leverage and scalable growth, which are more characteristic of technology stocks.

At this point, though, invesors should also consider SoFi’s valuation. Because the Rule of 40 is most closely tied to revenue-based valuation metrics, let’s take a look at SoFi’s forward price-to-sales (P/S) ratio, which currently stands at 5.6 times. Of course, that represents a premium of more than 50% to the sector median of 2.9 times, but as noted earlier, companies that consistently exceed the Rule of 40 can have valuation multiples approaching twice the sector median. In that context, SOFI stock doesn’t appear overvalued. The picture becomes more complicated when we consider the forward price-to-earnings (P/E) ratio, which for SoFi stands at 26.9 times, more than double the sector median of 10 times. Still, tech companies typically trade at P/E multiples between 20 times and 40 times, which suggests SOFI could be seen as fairly valued — or even undervalued — if investors embrace Noto’s positioning of the company as a high-margin tech firm.

SoFi’s Guidance Overshadows Record Results

SoFi Technologies recently reported Q1 results, with key performance metrics meeting or surpassing Wall Street’s expectations. Still, SOFI stock plunged more than 15% after the company issued below-consensus Q2 revenue growth guidance and refrained from raising its full-year outlook.

SoFi reported record adjusted net revenue of $1.1 billion, up 41% year-over-year (YOY) and exceeding Wall Street’s $1.05 billion consensus estimate. Revenue increased across each of SoFi’s core business segments. Adjusted net revenue in the Lending segment, which remains SoFi’s main growth driver, climbed 53% YOY to $629 million, fueled by higher net interest income. The company generated more than $1 billion in cash revenue, including roughly $690 million from net interest income and about $390 million from interchange, brokerage, technology and loan platform, and loan origination fees.

Meanwhile, total loan originations climbed to $12.2 billion in the quarter, with the neobanking company citing “record originations” across all three of its lending segments. That compares with $7.2 billion reported in the same period a year earlier. The company also added a record 1.1 million new members during the quarter, increasing total members by 35% YOY to 14.7 million.

Beyond delivering durable growth, SoFi achieved solid profitability. Adjusted EBITDA grew 62% YOY to $340 million in Q1. Adjusted earnings came in at $0.12 per share, in line with expectations.

Still, these record results were overshadowed by the company’s guidance. First, SoFi said it anticipates adjusted revenue growth of 30% in Q2, slightly below the 31% growth analysts had expected. Second, investors were disappointed that the company kept its 2026 revenue forecast unchanged, despite achieving multiple performance milestones across its lending business.

In an interview with Jim Cramer, Noto noted that the company refrained from raising its full-year outlook because of macroeconomic uncertainty. “We did not raise the full-year guidance because when we originally gave the full-year guidance, we were anticipating at least two Federal Reserve rate cuts,” he said. “And now we’re assuming that there will be no rate cuts.”

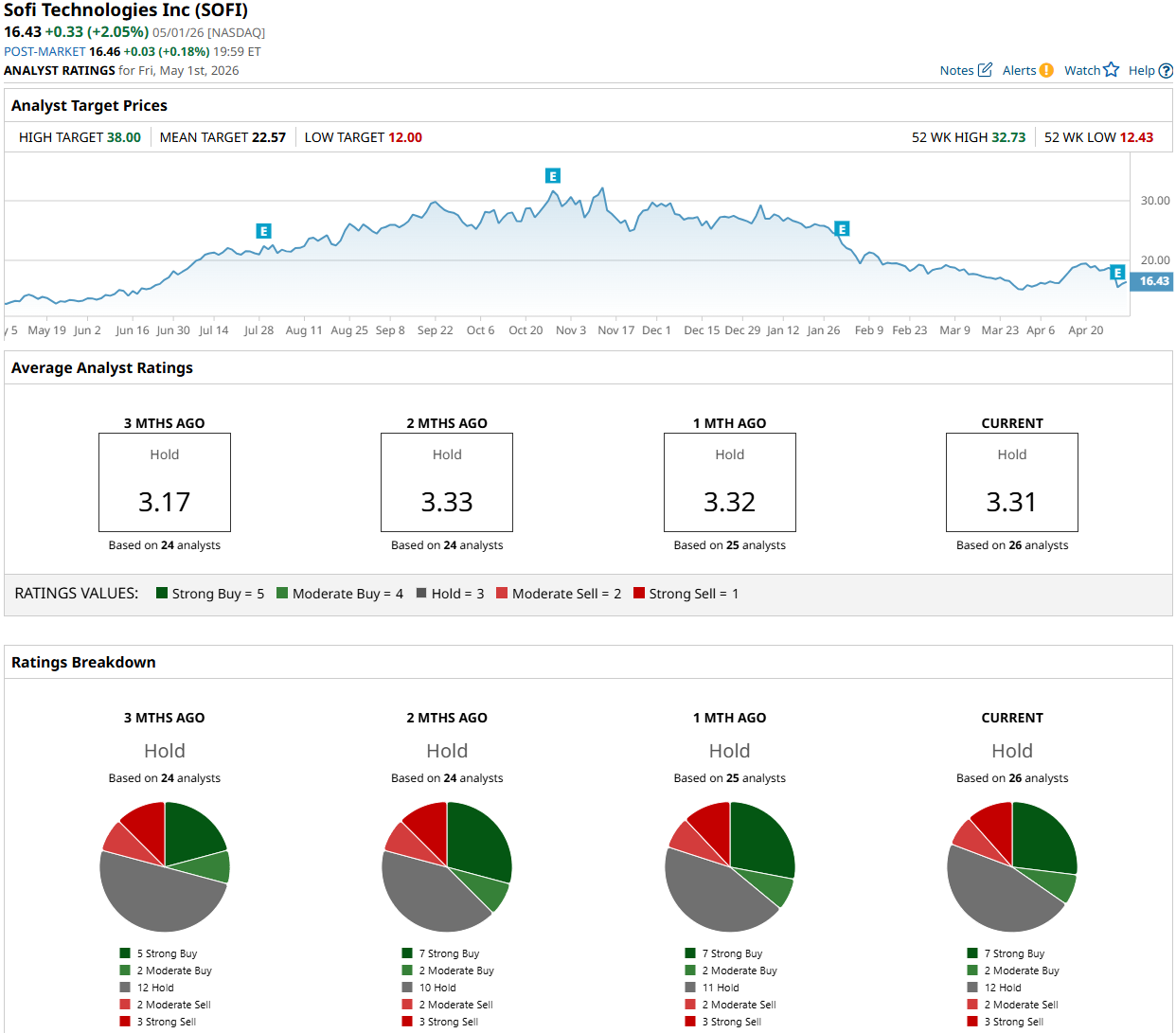

What Do Analysts Expect for SOFI Stock?

Wall Street analysts are taking a cautious stance on SOFI stock, as reflected in the consensus “Hold” rating. Of the 26 analysts covering the stock, seven rate it a “Strong Buy,” two have a “Moderate Buy,” 12 advise a “Hold” rating, two suggest a “Moderate Sell,” and three assign a “Strong Sell” rating. The average price target for SOFI stock is $22.57, implying 39% potential upside from current levels.

On the date of publication, Oleksandr Pylypenko did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)