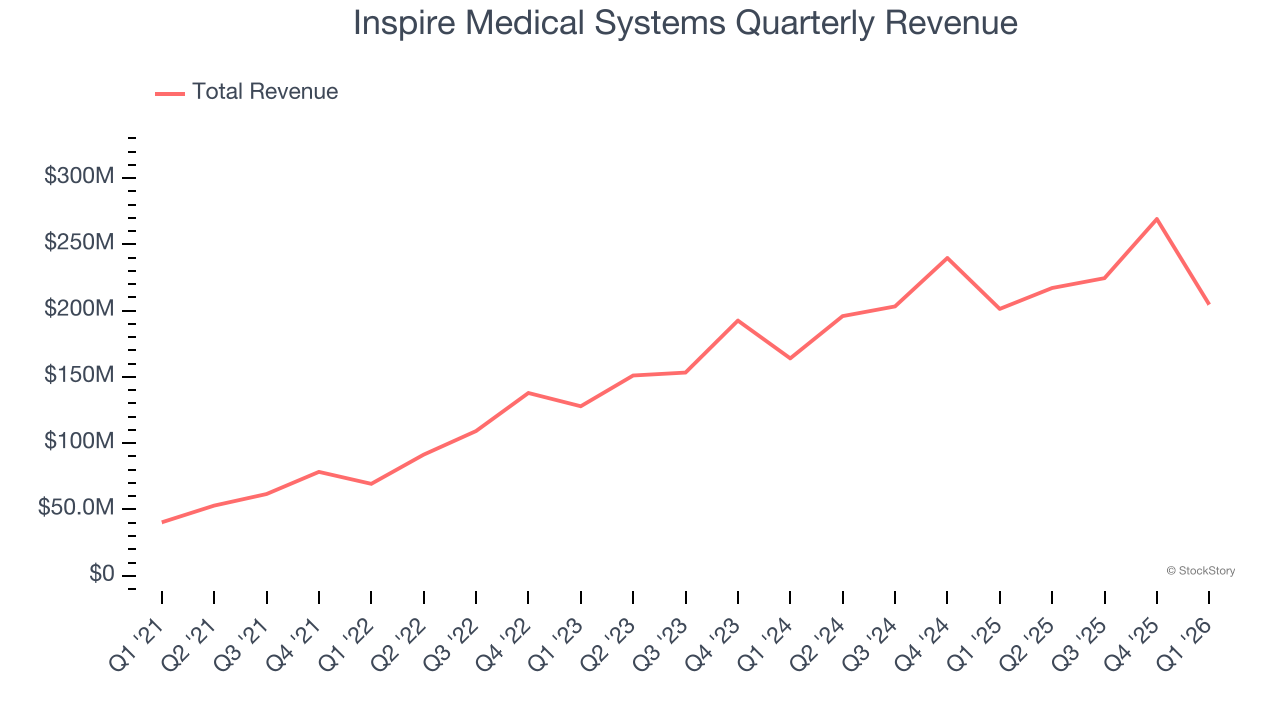

Medical technology company Inspire Medical Systems (NYSE:INSP) beat Wall Street’s revenue expectations in Q1 CY2026, with sales up 1.6% year on year to $204.6 million. On the other hand, the company’s full-year revenue guidance of $850 million at the midpoint came in 11.6% below analysts’ estimates. Its non-GAAP profit of $0.10 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Inspire Medical Systems? Find out by accessing our full research report, it’s free.

Inspire Medical Systems (INSP) Q1 CY2026 Highlights:

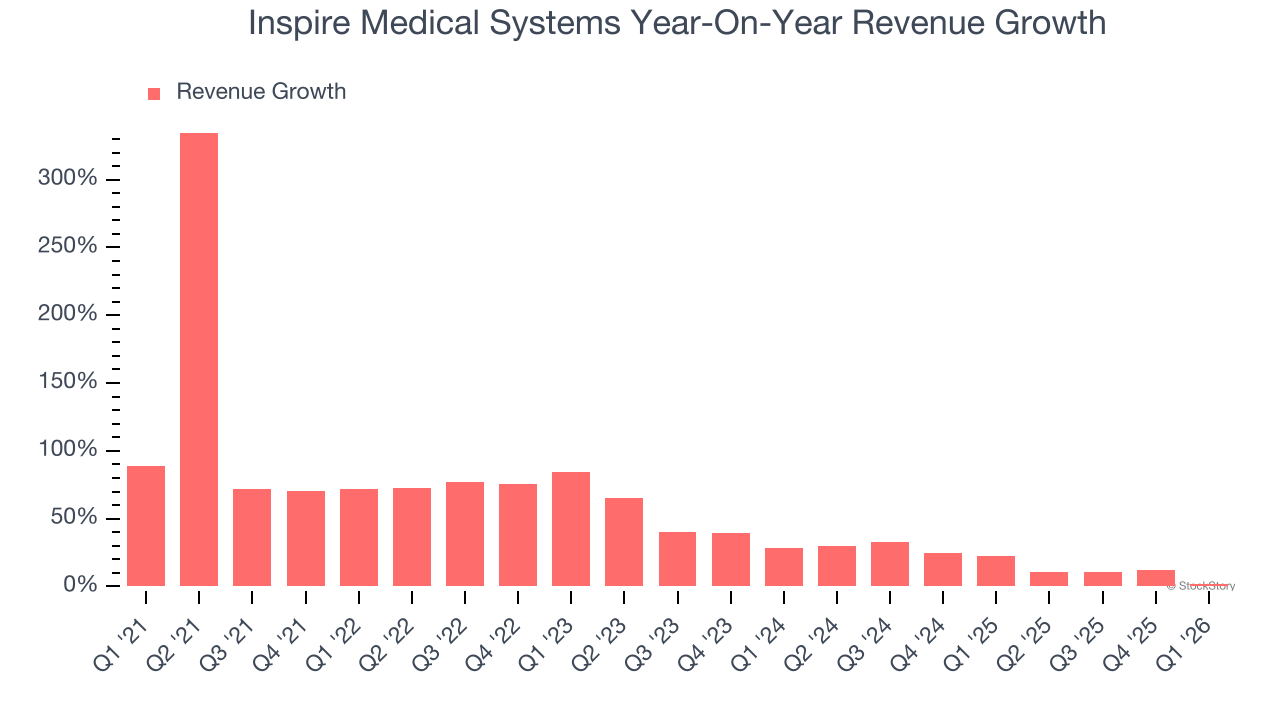

- Revenue: $204.6 million vs analyst estimates of $200.7 million (1.6% year-on-year growth, 1.9% beat)

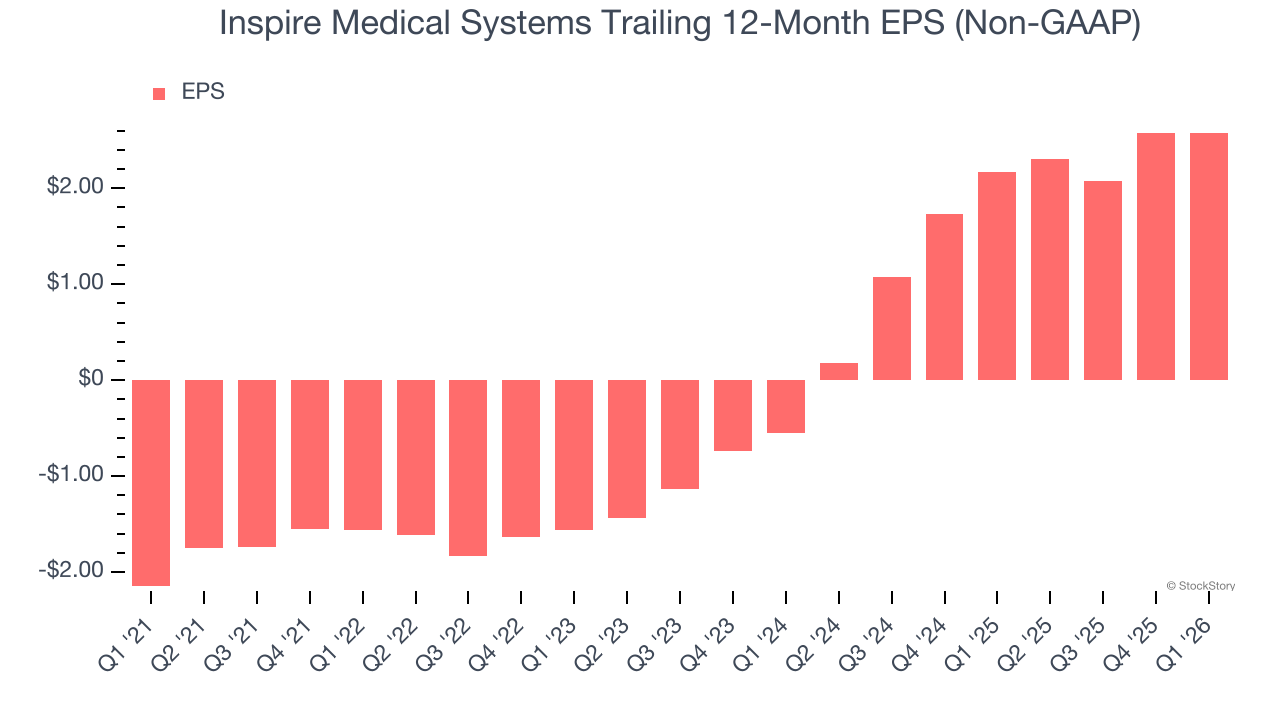

- Adjusted EPS: $0.10 vs analyst estimates of -$0.26 (significant beat)

- Adjusted EBITDA: $35.89 million vs analyst estimates of $19.86 million (17.5% margin, 80.7% beat)

- The company dropped its revenue guidance for the full year to $850 million at the midpoint from $975 million, a 12.8% decrease

- Management lowered its full-year Adjusted EPS guidance to $1 at the midpoint, a 52.4% decrease

- “We are continuing to work with key stakeholders to implement solutions that will resolve the coding and reimbursement uncertainty for Inspire V...We expect the challenges caused by this uncertainty to persist through the balance of 2026."

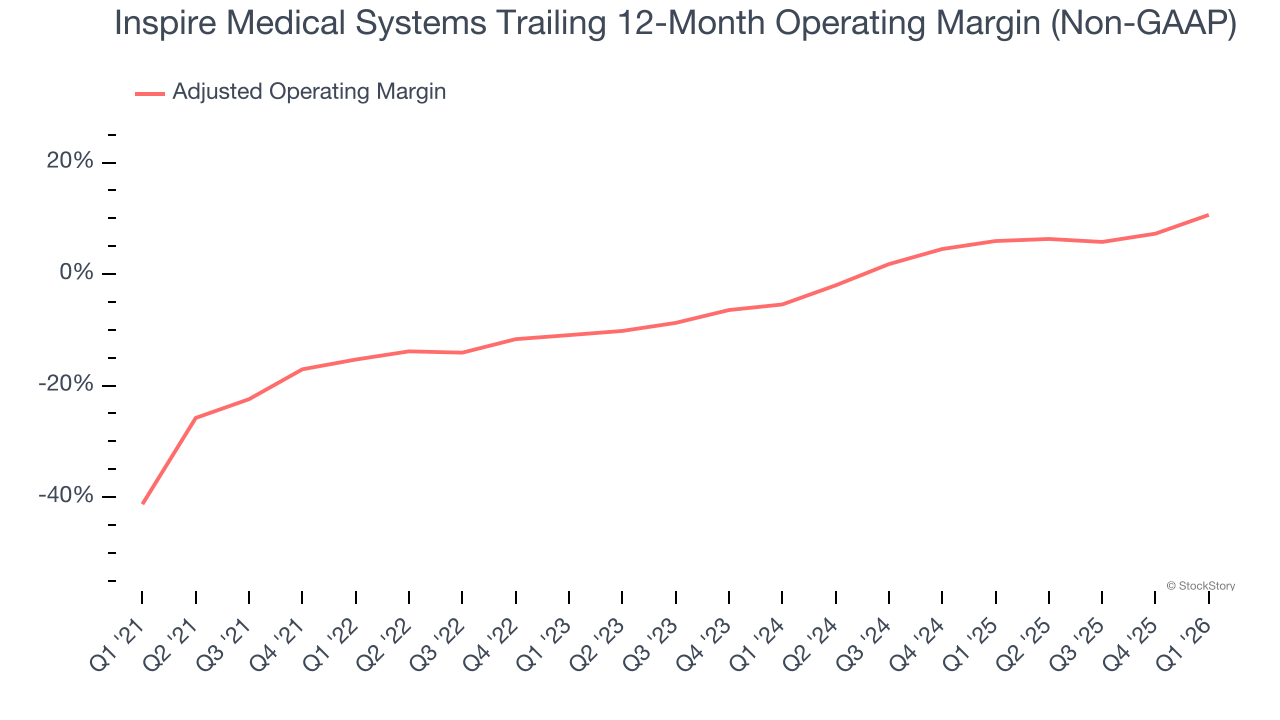

- Operating Margin: -0.5%, in line with the same quarter last year

- Market Capitalization: $1.63 billion

“Our first quarter results reflect revenue growth and improved adjusted operating income and cash flow,” said Tim Herbert, Chairman and CEO of Inspire Medical Systems.

Company Overview

Offering an alternative for the millions who struggle with traditional CPAP machines, Inspire Medical Systems (NYSE:INSP) develops and sells an implantable neurostimulation device that treats obstructive sleep apnea by stimulating nerves to keep airways open during sleep.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Inspire Medical Systems grew its sales at an incredible 46.8% compounded annual growth rate. Its growth beat the average healthcare company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Inspire Medical Systems’s annualized revenue growth of 17.7% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Inspire Medical Systems reported modest year-on-year revenue growth of 1.6% but beat Wall Street’s estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to grow 8.3% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is healthy and implies the market is forecasting success for its products and services.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Adjusted Operating Margin

Inspire Medical Systems was roughly breakeven when averaging the last five years of quarterly operating profits, lousy for a healthcare business.

On the plus side, Inspire Medical Systems’s adjusted operating margin rose by 25.9 percentage points over the last five years, as its sales growth gave it immense operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 16.1 percentage points on a two-year basis. These data points are very encouraging and show momentum is on its side.

This quarter, Inspire Medical Systems generated an adjusted operating margin profit margin of 14.5%, up 15.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Inspire Medical Systems’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

In Q1, Inspire Medical Systems reported adjusted EPS of $0.10, in line with the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Inspire Medical Systems’s full-year EPS of $2.58 to shrink by 1.6%.

Key Takeaways from Inspire Medical Systems’s Q1 Results

It was good to see Inspire Medical Systems beat analysts’ revenue and EPS expectations this quarter. On the other hand, its full-year revenue and EPS guidance both missed after being lowered due to "coding and reimbursement uncertainty" that will continue throughout 2026. The market was hoping that this would be resolved sooner. Overall, this quarter could have been better. The stock traded down 18.8% to $44.50 immediately after reporting.

Inspire Medical Systems may have had a tough quarter, but does that actually create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).

/Amazon%20pickup%20%26%20returns%20building%20by%20Bryan%20Angelo%20via%20Unsplash.jpg)

/Microsoft%20Corporation%20logo%20on%20sign-by%20Jean-Luc%20Ichard%20via%20iStock.jpg)

/Western%20Digital%20Corp_%20logo%20on%20sign-by%20360b%20via%20Shutterstock.jpg)