/Amazon%20pickup%20%26%20returns%20building%20by%20Bryan%20Angelo%20via%20Unsplash.jpg)

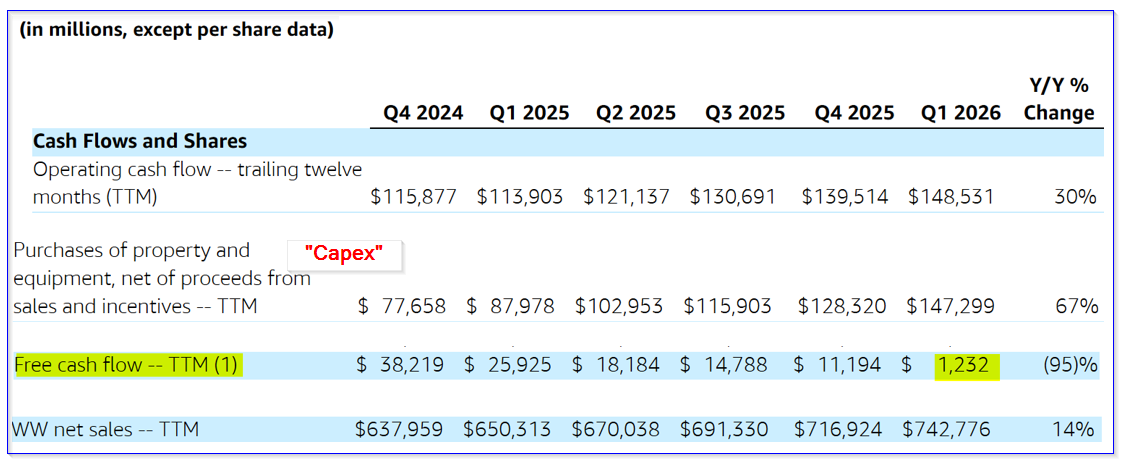

Amazon Inc. (AMZN) produced just $1.232 billion in free cash flow (FCF) on a trailing 12-month (TTM) basis in Q1. That's barely 0.17% of its TTM sales, despite a 19.8% operating cash flow (OCF) margin. But does the market care? Apparently not, as AMZN stock has been rising.

AMZN closed at $268.26 on Friday, May 1, up 2% from April 29 ($257.70) when Amazon released its Q1 earnings after the market close. In fact, it's now at a 6-month high.

This is so interesting, since a year ago, Amazon generated $25.9 billion in FCF, representing a 4% FCF margin on lower sales. But AMZN stock a year ago was just $190.20.

In other words, AMZN stock has risen 41% over the last year, even though FCF has dwindled to a trickle. This can be seen in the supplemental data table Amazon provided:

Massive Capex Spending Will Pay Off

It shows that even though sales have risen 14% on a trailing 12 months (TTM) basis, and operating cash flow (OCF) has grown 30% YoY, capex spending has increased 67%.

That has led to a huge drop in FCF - a 95% YoY decline.

Andrew Jassy, Amazon's CEO, made it clear that most of this increase is due to its AWS division's growth and AI-related spending that will benefit the company over the long term.

He pointed out on the conference call that the faster AWS grows, the more short-term capex Amazon will spend on land, power, buildings, chips, servers, etc.

For example, it typically takes 6 to 24 months before they can bill clients, but the capex funds assets with 30-year useful lives for data centers and 5-6 years for chips, servers, and networking gear. As a result, it takes a couple of years for FCF to begin generating returns. It takes time for the initial capex tranches to convert into FCF that exceeds ongoing capex as revenue rises.

In other words, investors need to take a long view on the capex growth. Amazon has had a long history of turning it into FCF with great success. That is why investors seem to be willing to go along.

Let's look at some numbers to show how that might work.

Projecting Future Cash Flow

Analysts now project that revenue this year will increase to $820.4 billion, from $716.92 billion in 2025 (i.e., up +14.4%). That's equal to its TTM growth rate as seen above. But next year, 2027, they project sales of $921.5 billion, another 12.3% gain.

So, if operating cash flow comes in at 20% of sales, as it did in the TTM period seen above, 2027 operating cash flow (OCF) could be:

$921.88 x 0.20 = $184.3 billion OCF

So, if capex spending rises another 15% from the $147.3 billion in the TTM period, it will reach $169.4 billion. As a result, 2027 FCF could be:

$184.3 billion OCF - $169.4 capex = $14.9 billion FCF

That would represent 1.6% of the $921.5 billion in sales.

Let's project out further. Assuming sales exceed $1 trillion by 2028 and hit 1.166 trillion by 2029 (i.e., 12.5% growth each year), and assuming a 20% OCF margin with $200 billion in capex:

2029 sales $1,166 billion x 0.20 OCF margin = $233 billion OCF

$233 b OCF - $200 billion capex = $33 billion FCF 2029

This shows that Amazon could be a run rate to return to substantial FCF levels. That could be why AMZN stock is not falling.

However, that does not necessarily mean AMZN stock is cheap here.

AMZN Price Targets

If AMZN can make $33 billion in FCF in 3 years, and assuming a 1% FCF yield, here is how the market might value the stock:

$33b / 0.01 = $3.3 trillion

That is only 14.3% higher than its existing $2.885 trillion market capitalization.

However, this future valuation, when discounted to the present at a 5% discount rate, would result in a valuation that is 86.38% of the $3.3 trillion market cap:

$3.3 trillion x 0.8638 = $2.850.5 billion (i.e., -1% from today's valuation).

In other words, AMZN stock would be worth about 1.1% less than $268.26, or $265.00 per share.

Not everyone agrees. For example, the average of 64 analysts' price targets surveyed by Yahoo! Finance is $304.66. That's +13.6% higher than Friday's close. Similarly, Barchart's mean survey price is $310.09, and AnaChart's survey of 43 analysts is $311.51.

Clearly, other analysts believe that Amazon's future free cash flow will be even stronger than before and better than my calculations.

Next week, I will write about some ways that investors can play AMZN stock. This is even though it's at a peak price and has higher analyst price targets, but fundamentals might not support this.

That will involve using probability theory to set an expected return (ER) and using long/short options plays that fit with this ER investment method.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)

/AI%20(artificial%20intelligence)/Data%20Center%20by%20Caureem%20via%20Shutterstock%20(2).jpg)