Gold (GCM26) has always had a way of stepping into the spotlight just when the world starts feeling uncertain. From central banks quietly building reserves to everyday investors looking for safety, the yellow metal’s appeal tends to rise when confidence in currencies and markets begins to wobble.

That script played out once again over the past year. A mix of aggressive rate cuts from the Federal Reserve through 2024 and 2025 weakened the U.S. dollar, while persistent inflation, trade tensions, and geopolitical flashpoints pushed investors toward assets that can hold value when everything else feels shaky.

The result was a powerful rally. Gold surged to an all-time high near $5,600 per ounce in January before cooling off to slightly over $4,500. Gold slipped despite ongoing conflict as rising oil-driven inflation and higher yields strengthened the dollar, while stalled U.S.-Iran talks made investors cautious and trimmed safe-haven demand. Even with that pullback, the metal remains up roughly 39% over the past 52 weeks, underlining just how strong the underlying demand has been.

Against that backdrop, gold miners are quietly entering a sweet spot. Higher prices expand margins, improve cash flows, and strengthen balance sheets. While the big names have already caught attention, a few under-the-radar players — like Equinox Gold (EQX), SSR Mining (SSRM), and IAMGOLD (IAG) — are starting to stand out, with analysts seeing meaningful upside still ahead.

Gold Mining Stock #1: Equinox Gold (EQX)

Equinox Gold has steadily built its presence in the mining sector since its incorporation in 2007. Based in Vancouver, Canada, the company is engaged in acquiring, exploring, developing, and operating mineral properties across the Americas, with a primary focus on gold and a secondary exposure to silver.

With a market capitalization of $11 billion, Equinox is supported by a portfolio of high-quality, long-life operations and a pipeline of expansion projects. Founded and chaired by Ross Beaty, and led by an experienced team, the company emphasizes disciplined execution and operational efficiency. Its diversified asset base offers investors a structured path to long-term growth within the gold space.

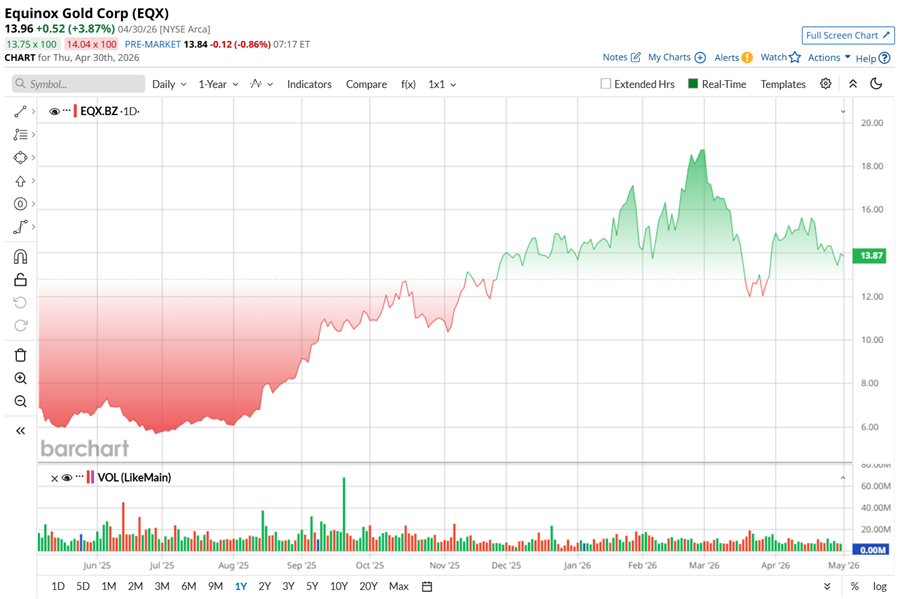

Shares of this gold mining stock have risen 122% over the past 52 weeks, riding the broader strength in gold. Even in the last six months, the momentum has held with a 34% gain. EQX stock hit a 52-week peak of $18.96 in February.

That rally did not hold, however. Since then, the stock has pulled back roughly 27% as volatility in precious metal prices, shaped partly by Middle East tensions, weigh on sentiment. The company’s first-quarter 2026 update in April added to the pressure, with lower production raising questions around its ability to meet full-year guidance.

Layering in analyst concerns about stretched valuations, and the story shifts. What was once a strong outperformer has recently lagged other materials names, as investors reassess both execution risks and the broader commodity backdrop.

Looking at the valuation, EQX stock starts to look a bit more interesting at these levels. The stock is currently trading at around 12 times forward earnings, which sits below the broader sector average. This discount suggests the recent pullback may have already priced in a fair bit of the near-term uncertainty. So, while sentiment has cooled, the valuation quietly hints at a more balanced risk-reward setup for investors willing to look past the short-term noise.

Equinox Gold closed 2025 on a strong note, with its Q4 earnings report in February reflecting both scale and momentum. Revenue amounted to $681.4 million, surging 90% year-over-year (YOY), while adjusted EPS doubled to $0.35. The bottom line outpaced expectations, though revenue fell slightly short of the Street’s estimates. Operational strength was evident as income from mine operations jumped 257% to $342.3 million, and adjusted EBITDA climbed sharply to $579 million.

Production told a similar story. The company delivered a record 247,024 ounces of gold in Q4, led by standout performances at key assets. Greenstone crossed 70,000 ounces, up 29% sequentially on improved mining and milling rates. Meanwhile, Valentine marked a milestone, achieving commercial production ahead of schedule in November and contributing over 23,000 ounces during the quarter.

What’s more impressive is that the company introduced its first dividend of $0.015 per share in February, paid on March 26, and now intends to maintain a quarterly payout at the same level, or $0.06 on an annualized basis.

As the calendar turned, the pace moderated. In Q1 2026, Equinox produced 197,628 ounces of gold, a 20% sequential decline, reflecting the typical transition phase after a strong year-end. Greenstone produced 60,338 ounces, Valentine produced 27,064 ounces, Mesquite saw 13,174 ounces, Nicaragua saw 81,280 ounces, Brazil produced 13,473 ounces, and Castle Mountain produced 2,299 ounces.

Even so, the underlying trajectory remains intact. Canadian production is expected to be second-half weighted as newer assets continue ramping up, complemented by steady output from Nicaragua and Mesquite. At Greenstone, optimization efforts are gaining traction — winter mining rates averaged 180,248 tonnes per day (tpd), while mill throughput reached 24,544 tpd, “with 51% of days exceeding nameplate capacity,” a clear improvement from Q4.

Valentine is building rhythm, too. The plant averaged 6,192 tpd for the quarter, touching full capacity in the latter months, while ongoing exploration adds further depth.

Looking ahead, Equinox sees Canadian production averaging 543,000 ounces annually from 2026 through 2036. Greenstone is expected to contribute around 320,000 ounces per year, while Valentine could deliver 223,000 ounces, supported by a planned Phase 2 expansion. Backed by strong gold prices and cash flow, the company is positioning itself to fund growth while returning capital, quietly setting the stage for its next phase.

The company is anticipated to release its full Q1 report on May 6, after the market closes. Analysts tracking the company anticipate Q1 EPS growth of 462% YOY to $0.29. Looking ahead to fiscal 2026, EPS is expected to rise 283% YOY to $1.15 before surging by another 15% YOY to $1.32 in fiscal 2027.

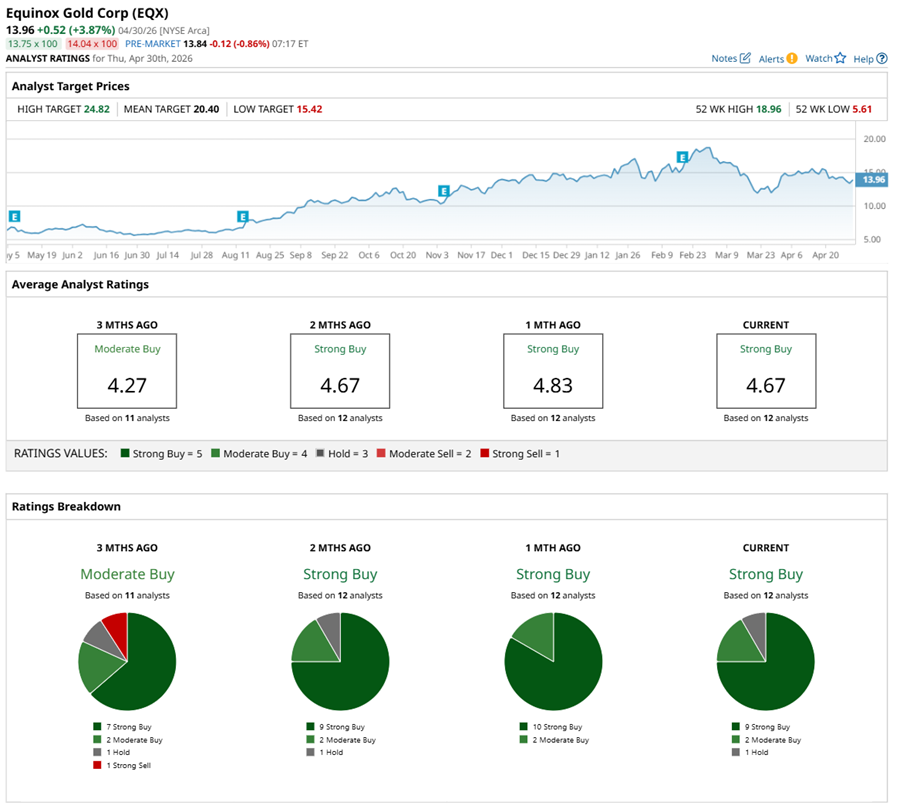

Sentiment around EQX stock remains positive. Stifel analyst Ingrid Rico recently reiterated a “Buy” rating, setting a price target of C$31. Josh Wolfson from RBC Capital Markets also maintained a “Buy” with a $23 target. Adding to the chorus, ATB Cormark Capital Markets analyst Richard Gray kept his “Buy” rating intact as well, alongside a C$29 target. Taken together, despite near-term fluctuations, analysts broadly see meaningful room for EQX stock to climb.

Wall Street is majorly bullish on EQX stock. Overall, the stock has a consensus “Strong Buy” rating. Of the 12 analysts covering shares, nine advise a “Strong Buy,” two suggest a “Moderate Buy” rating, and one analyst has a “Hold” rating.

EQX stock’s average analyst price target of $20.40 suggests potential upside of 47% from here. Meanwhile, the Street-high target of $24.82 suggests that the stock could rally as much as 79%.

Gold Mining Stock #2: SSR Mining (SSRM)

Next up, SSR Mining has been shaping its place in the mining sector since its incorporation in 1946, operating today from Denver, Colorado, with a market cap of $6.3 billion. The company focuses on acquiring, exploring, and developing precious metal assets across the United States, Turkey, Canada, and Argentina, targeting gold doré alongside copper, silver, lead, and zinc.

SSR's portfolio spans prolific districts — from Çöpler in Turkey and Marigold in Nevada to Seabee in Saskatchewan and Puna in Argentina, among others. Backed by an experienced team, the firm blends technical expertise with a strong balance sheet and consistent cash flow, positioning itself to fund disciplined, long-term growth.

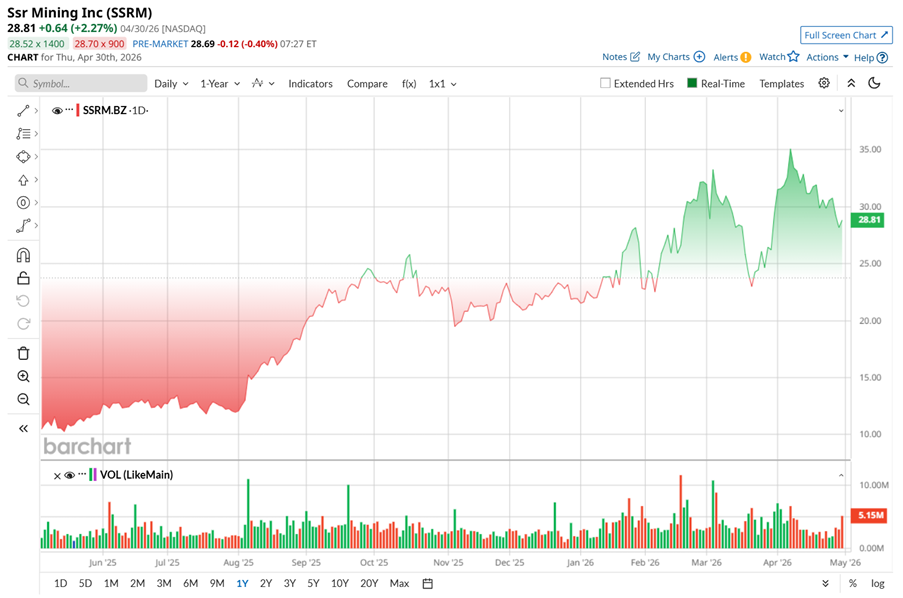

SSRM stock has been on a run that’s tough to overlook. Over the past two years, the stock has surged an eye-catching 436%, reflecting a broader shift in sentiment toward precious metals. The momentum really picked up in the last year, with shares rallying roughly 186% in the past 52-week stretch and up 32% in just the past six months.

Even in 2026, the climb has not slowed. Shares are up 31% year-to-date (YTD), hitting a high of $36.51 on April 9. Along the way, the stock has recorded multiple new highs over the past year, underlining the strength of the trend. Much of SSRM stock's rally has been fueled by the sharp upswing in precious metal prices, which has lifted sentiment and valuations across the sector.

Valuation-wise, SSR Mining still looks reasonably priced despite the rally, trading at 7.3 times forward adjusted earnings — comfortably below both the sector average and its own historical median, suggesting room for upside if momentum in metals holds.

SSR Mining delivered a strong fourth quarter fiscal 2025 report on Feb. 17, comfortably beating Wall Street’s projections. Revenue grew 61% YOY to $521.7 million, while adjusted EPS jumped sharply from $0.10 in Q4 2024 to $0.88.

Cash generation stood out. Operating cash flow reached $172.1 million, and free cash flow came in at $106.4 million for the quarter. For the full year, those figures expanded to $471.9 million and $241.6 million, respectively, helping lift cash and cash equivalents to $534.8 million by year-end.

Operationally, SSR Mining produced 91,031 ounces of gold in Q4, while its reserve base strengthened meaningfully. Proven and probable reserves climbed to 11 million gold equivalent ounces, marking a near 40% YOY increase — an important signal of long-term depth. Looking ahead, management is guiding for 2026 production in the range of 450,000 to 535,000 gold equivalent ounces across its core operations.

SSR Mining also announced a $300 million share buyback program in February, reinforcing confidence in its valuation and future trajectory.

The company is projected to release its first quarter 2026 financial results after markets close on May 5. Analysts project Q1 EPS to be around $0.81, up 179% YOY. Looking ahead, fiscal 2026 EPS is expected to climb 96% YOY to $3.93, followed by another 8% annual increase to $4.24 in fiscal 2027.

SSR Mining made a decisive move in early March, announcing a $1.5 billion all-cash sale of its 80% stake in the Çöpler mine. The decision comes in the wake of a tragic 2024 accident that had already forced operations to a halt, turning the asset into more of a burden than a contributor. By exiting Çöpler, the company is effectively cleaning up its portfolio, shedding risk while converting a stalled operation into immediate liquidity. Expected to close in Q3 2026, the deal could significantly strengthen the balance sheet.

What stands out is how this reshapes the story. The cash boost, alongside a projected 10% rise in gold-equivalent production for 2026, adds a fresh layer of momentum. That said, the path is not entirely clear just yet as regulatory approvals around the Çöpler transaction remain a key factor to watch.

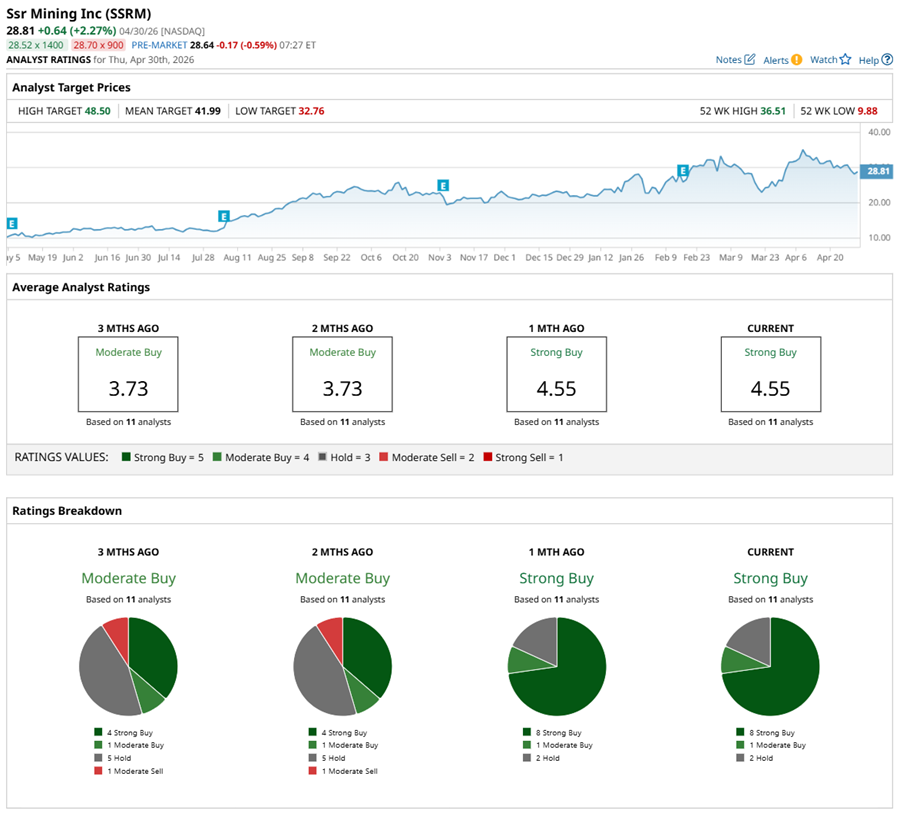

Analysts appear confident, with SSRM stock having an overall “Strong Buy” rating, which is an upgrade from its consensus “Moderate Buy” rating two months back. Of the 11 analysts tracking the stock, nine have a “Strong Buy” rating, one analyst has a “Moderate Buy,” and one has a “Hold” rating.

The average price target of $41.45 implies potential upside of 44% from here. Meanwhile, the Street-high target of $48 hints that the stock could rally as much as 67%.

Gold Mining Stock #3: IAMGOLD (IAG)

IAMGOLD has built its identity as a focused gold producer and developer with operations spanning both Canada and Burkina Faso. Founded in 1990 and headquartered in Toronto, Canada, the company anchors its growth on its flagship Côté Gold project in Ontario, a large-scale asset spread across 59,600 hectares. IAMGOLD's market cap currently stands at $9.6 billion.

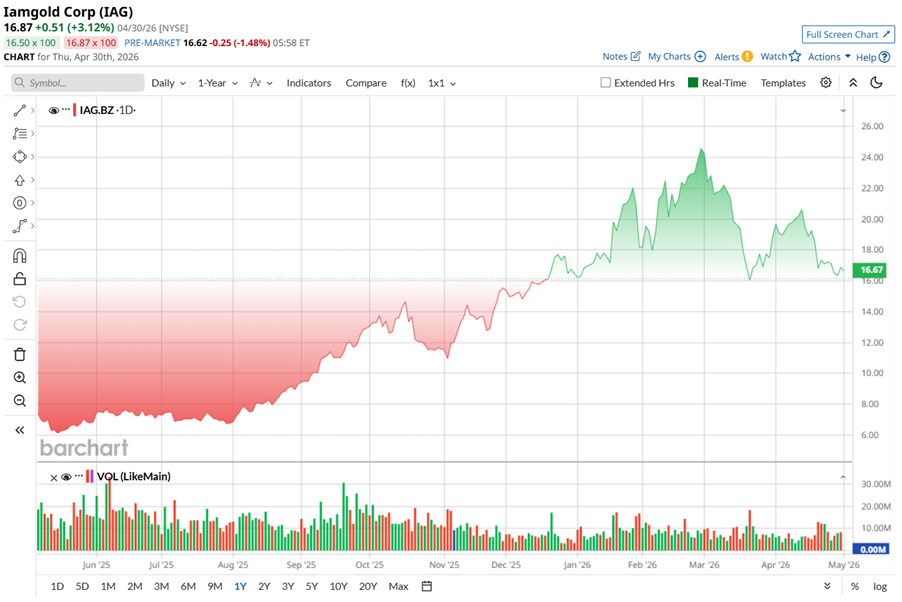

Shares of the gold mining company have had a stellar run in the past year, up by 143% over the past 52 weeks and even hitting an all-time high of $24.87 in March, marking a period where momentum clearly favored gold names.

That said, the near-term picture has softened a bit. Over the past three months, IAG stock has slipped 15%, reflecting a broader risk-off sentiment across gold equities. Volatility in bullion prices, along with some pressure on mining margins, appears to have weighed on investor confidence.

Even with this pullback, the broader trend has not completely faded. In 2026 so far, the stock is only down marginally on a YTD basis, suggesting that while momentum has cooled, underlying interest in the name is not completely disappearing.

From a valuation standpoint, IAG stock is priced attractively. IAG trades at around 7.7 times forward earnings, sitting below the sector average and its own historical median.

IAMGOLD closed out 2025 with impressive Q4 and fiscal 2025 results in February. Operations hit their stride during the year, translating into record margins and cash flow. In Q4, revenue surged 132% YOY to $1.09 billion, while adjusted EPS jumped to $0.70 from just $0.10 a year ago. For the full year, revenue reached $2.85 billion, and adjusted EPS more than doubled to $1.23, underscoring the scale-up across its assets.

IAMGOLD reported attributable gold output of 242,400 ounces in Q4 and 765,900 ounces for the year, landing right at the midpoint of its 735,000 ounce to 820,000 ounce guidance. This was supported by record quarterly production across all operations, with Côté Gold hitting the top end of its target.

Cash generation stood out as a key highlight. Mine-site free cash flow reached a record $626.6 million in Q4 and $1.19 billion for the full year. Liquidity remained solid at $868.6 million, including $421.9 million in cash and cash equivalents. Net debt dropped significantly by $514.9 million to $344.4 million by year-end.

Looking ahead, the company expects 2026 production to come in between 720,000 and 820,000 ounces, suggesting a steady continuation of current operating momentum. The mining company is set to announce its Q1 2026 earnings report after the market closes on May 5.

Analysts are optimistic, forecasting EPS for the quarter to rise 420% YOY to $0.52. Meanwhile, profit is expected to climb 77% annually to $2.18 per share in fiscal 2026, followed by a slight dip in fiscal 2027 EPS to $1.97.

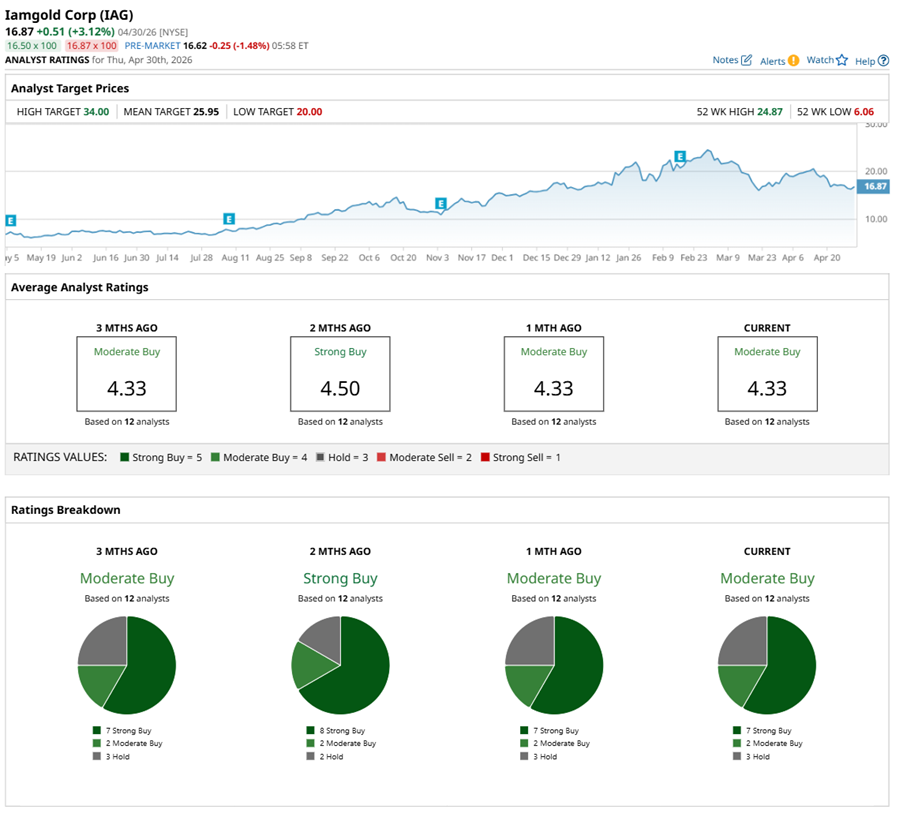

In April, RBC Capital analyst Josh Wolfson kept a “Buy” rating on IAG stock with a price target of $30, implying potential upside of 84% from current levels.

Overall, analysts are bullish on IAMGOLD’s growth potential, giving IAG stock a consensus "Moderate Buy" rating. Of the 12 analysts covering the stock, seven advise a “Strong Buy,” two suggest a “Moderate Buy,” and three analysts recommend a "Hold" rating.

The average price target of $25.49 suggests that IAG stock has potential upside of 56% from here. Meanwhile, the Street-high target price of $34 signals that the stock could rally as much as 108% from current levels.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Microsoft%20headquarters%20By%20Peter.jpeg)

/Micron%20Technology%20Inc_%20logo%20on%20building-by%20vzphotos%20vis%20iStock.jpg)

/NVIDIA%20Corp%20logo%20outside%20building-by%20BING-JHEN_HONG%20via%20iStock.jpg)

/Amazon%20-%20Image%20by%20bluestork%20via%20Shutterstock.jpg)