Howdy market watchers!

The tornado cleanup is underway in Enid, Oklahoma, after the recent EF4 storm that flattened a neighborhood and parts of Vance Airforce Base. It is still miraculous that there were no fatalities in our community nor were any airplanes damaged at the USAF base. God is good!

This has been one of the most active Aprils for severe weather that I can recall. Who knows what that will mean for May, but I guess we’re about to find out!

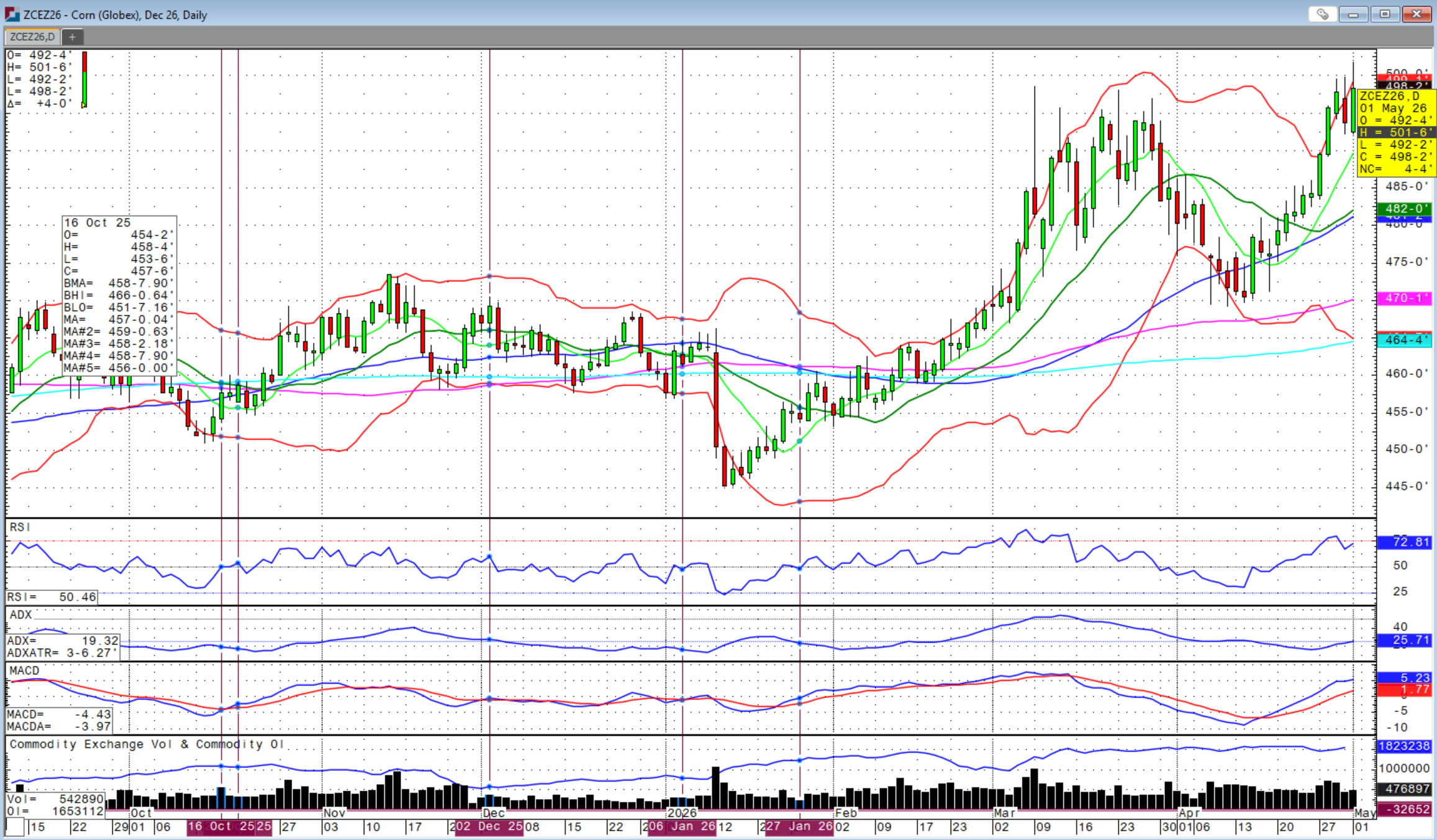

It was an exciting week in the grain markets with the bulls back on top. While wheat has dominated the lead, it was the corn market that finished the week with a bang as December corn trade above $5.00! This followed an outside reversal day lower on the charts on Thursday. However, that also coincided with the end of the month as well as the final day before First Notice Day on May grain futures and so there were other variables at play.

While wheat markets bounced back on Friday, KC wheat finished with an inside day on the charts awaiting weekend rains and fund flows. Eastern Colorado and Western Kansas have and are expected to get some rain over the next 72 hours, but we are hearing that it is largely too little, too late. Overall, winter wheat heading is said to be 34 percent as of this past Monday versus 21 percent last year. However, those figures have been widely criticized as being far lagging reality. Oklahoma and Kansas are both said to be 43 percent headed while Texas is showing 65 percent, but I think all three states are likely between 85-90 percent, especially Texas and Oklahoma.

There are many years where we think we’re going to have an early harvest and then the weather plays out to where it is right on time. This year feels different. Rain chances are limited in the forecast and temperatures are heating back up, especially in the 8-14 day outlook. Wheat is already beginning to turn in areas where it is typically 3 weeks from turning. We could see combines rolling in two weeks in southern areas.

The wheat market is just not so sure yet given this situation is largely isolated to US wheat. With adequate supplies globally, higher US wheat prices can translate to deterioration in competitiveness and therefore, reduced exports, which can tame a market pretty quick. Having said that, higher fertilizer prices are beginning to trim forecasts of wheat planting and topdressing in other parts of the world including Canada and Australia where the USDA Attache in both markets this week made sizable reductions to the coming crop’s forecast.

Fund flow also depends a lot on the value of the US dollar that weakened towards the end of the week with the Fed’s FOMC pausing interest rates in Chair Powell’s likely last meeting at the helm. However, there were 4 dissenting votes, which is the most since the mid 1990’s along with Chair Powell’s announcement that he would remain on the Board of Governors until the legal attacks on the organization from the Trump Administration subside or are resolved. The Trump Administration badly wants interest rates to be lowered to stimulate the economy, but inflation is far from tamed with rising energy prices. The national average gas price on May 1st was $4.39 per gallon. This is higher than it has been, but still manageable.

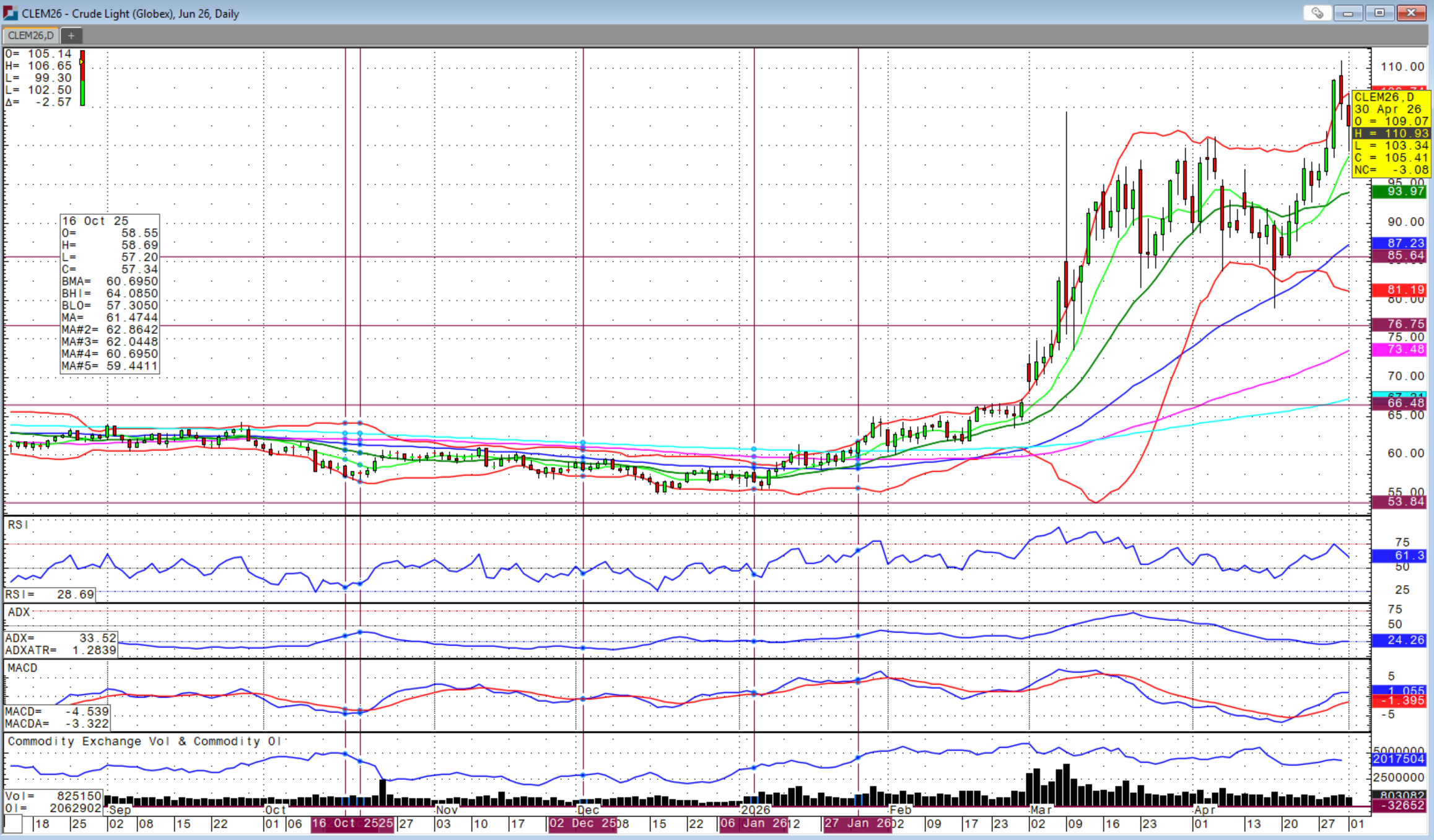

The question on all of our minds is where to from here. Crude oil prices somewhat corrected on Friday with Iran responding to the US proposal for peace, but then President Trump commented that their requests were unreasonable and unagreeable. Oil prices edged back up into the close finishing above $102 on WTI front-month, but the charts still point to higher highs barring any type of meaningful change in the current situation with the US blockade still in place.

The Trump Administration’s ability to act alone is also coming to an end with Congressional approval soon required for further military operations from a budget perspective. That is where the rubber really meets the road as legislators, many up for election in November, are going to be forced to be on record to vote for or against such action in Iran. The window is closing before cards have to be played in the open.

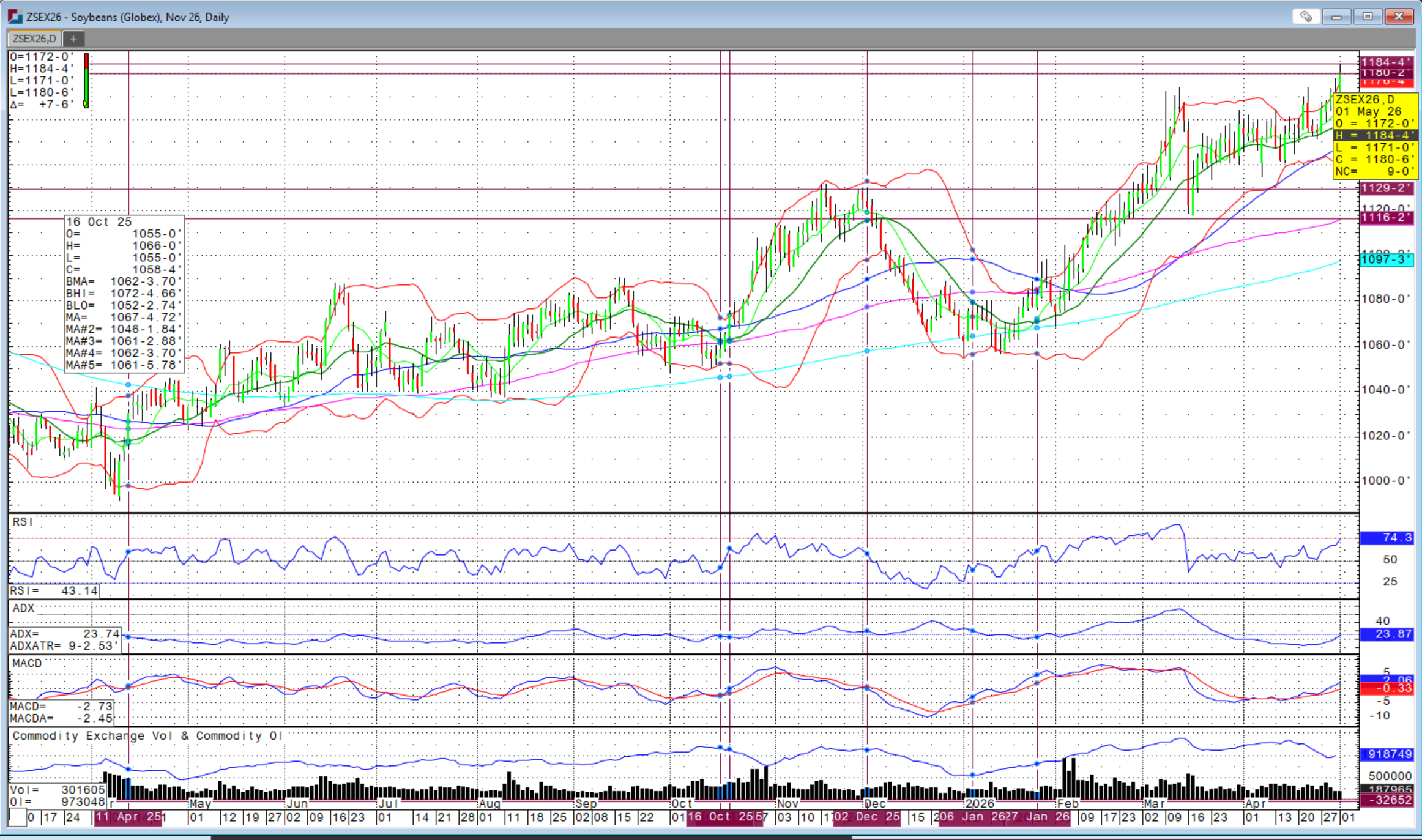

President Trump’s delayed trip to China sounds to be on for next week and all the markets will be watching the rhetoric before, during and after that trip to determine if there is something meaningful to trade from that news. China has purchased 11.5 million metric tons of the 12.0 MMT promised and I fully expect the remaining 500,000 MT to be purchased right ahead of that trip as a peacemaking card. The soybean market is sure optimistic with November new crop soybean futures trading to the highest levels since May 2024.

There are decisions of historic proportions to be made between the US and China that include the Middle East, Taiwan, Ukraine, agriculture, technology chips, among many more. The challenge that the Trump Administration has in terms of leverage is time. There is the short timeframe until the Mid-Term elections for Congress and the time remaining of Trump’s Presidency.

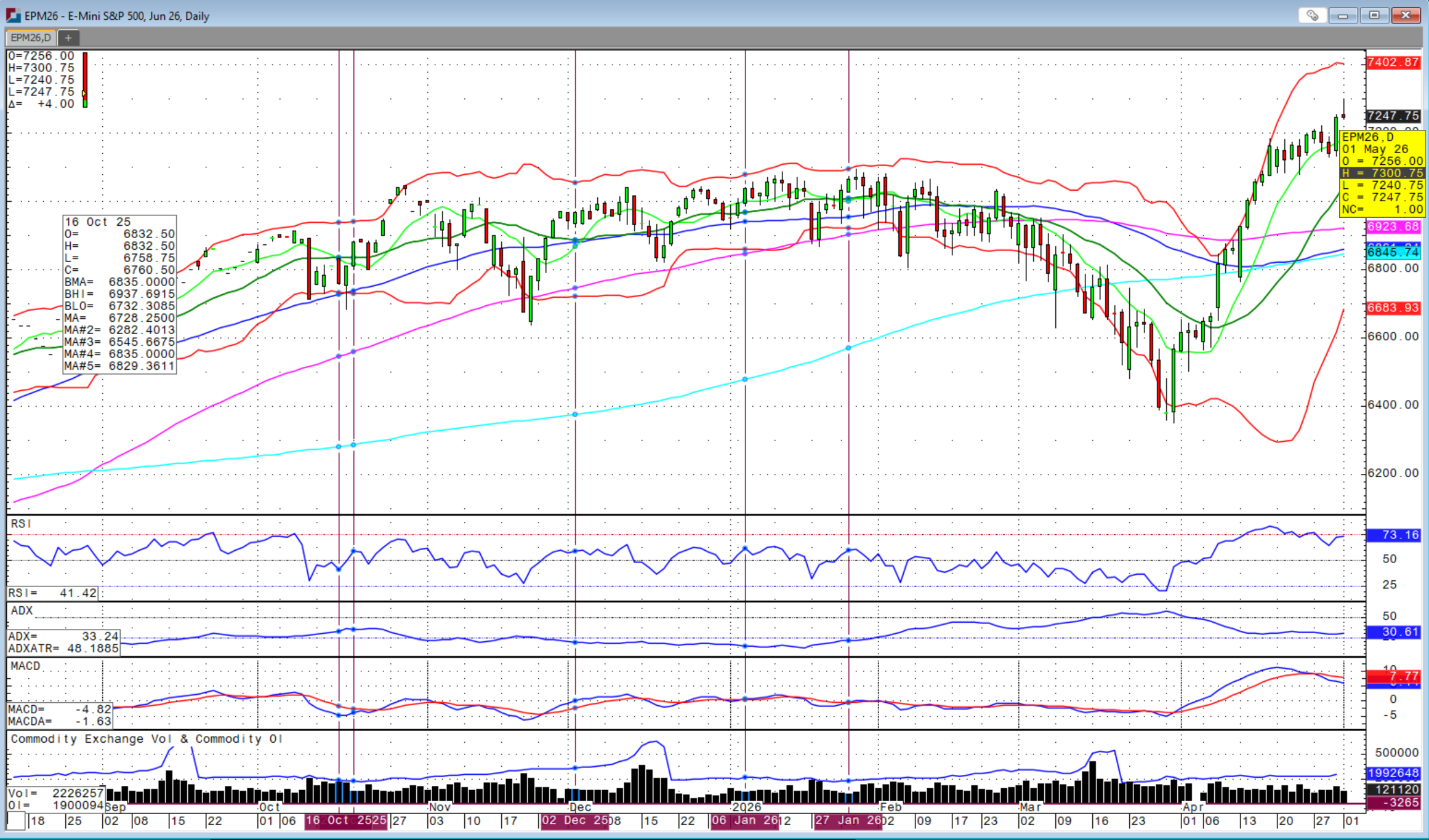

It was also reported this week that, as of March 2026, the national debt of the US held by the public has now surpassed the GDP of the US economy for the first time since World War II! This equates to $114,000 per American citizen. And yet, the stock market continues to surge higher. In fact, the S&P 500 made a new, all-time high above 7,300 on Friday and the Dow Jones traded above 50,000 points, again.

How will this ever end. Most are against raising taxes, everyone is against cutting benefits. There doesn’t seem to be a political outcome of any Party or platform that can solve this growing problem, until it breaks. Most hope that reality will be beyond their time given how complex the solution seems to be at every present time. And all the while, the US consumer continues to buy beef, regardless of its price!

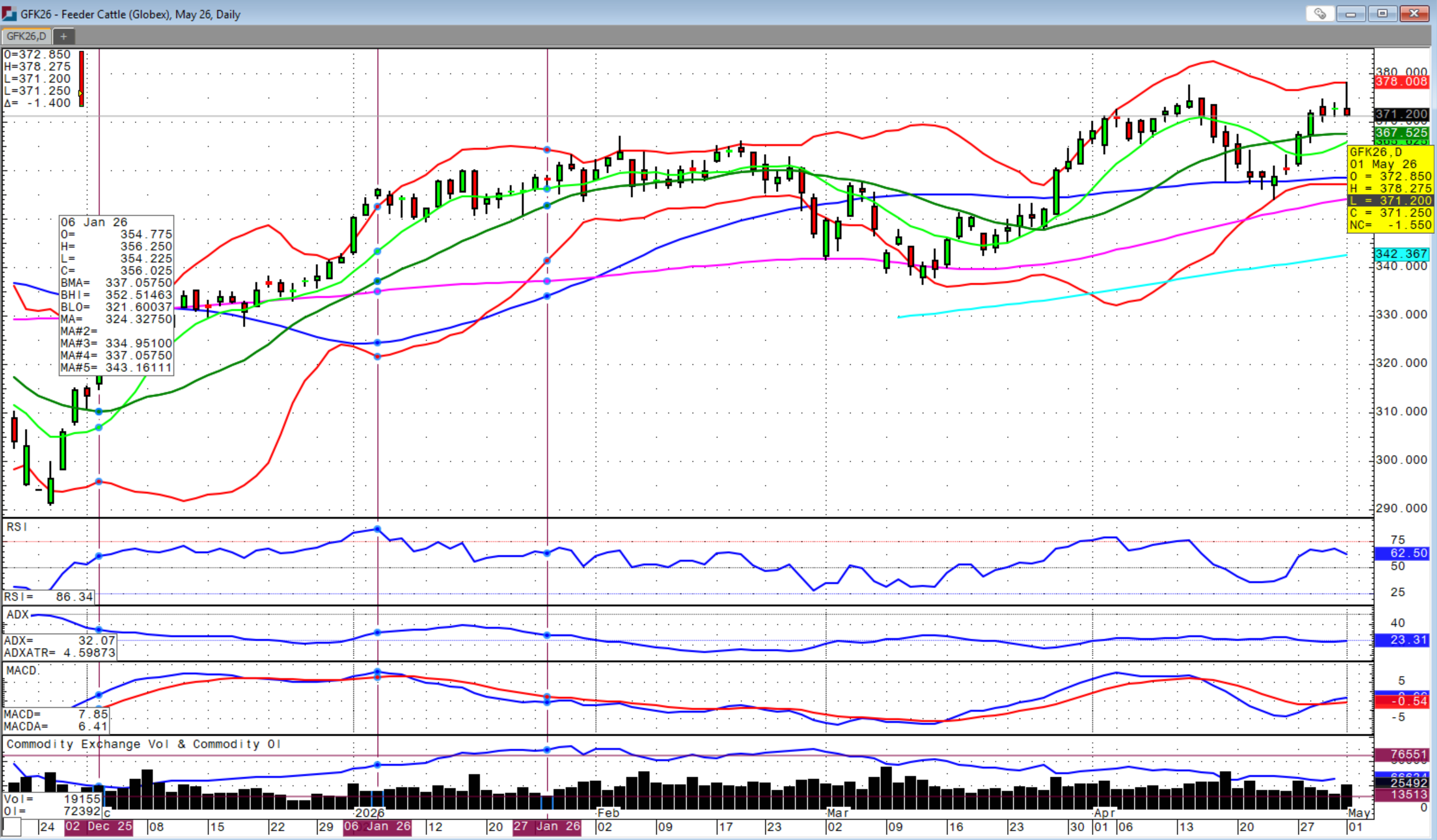

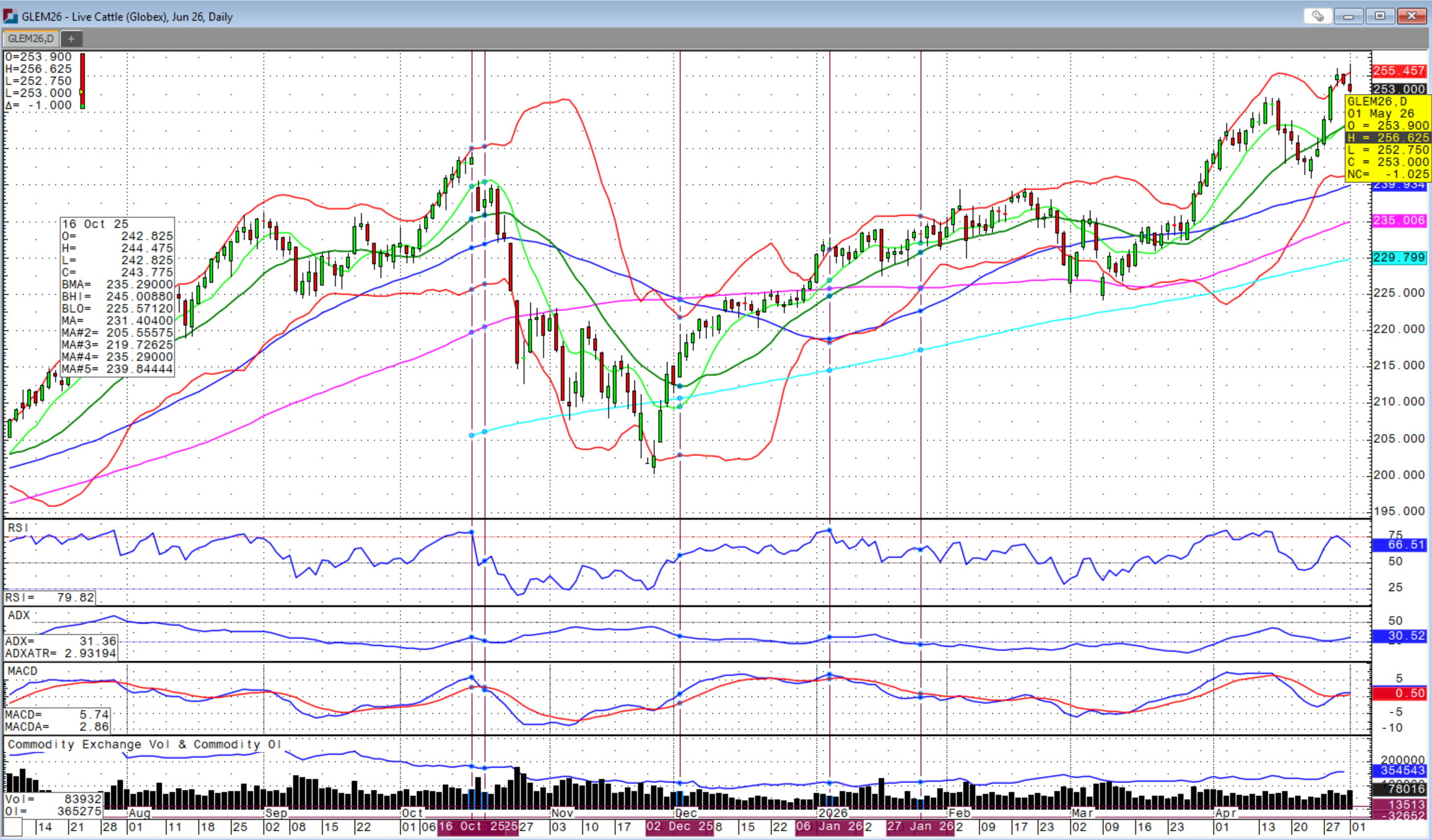

The cattle market was on fire this week, surging from the recent correction after new highs were made on April 14th. Well, new highs were made again on Friday. After Thursday’s inside day on the charts and higher high on Friday, I was feeling confident that we could get continuation higher on Monday, as the textbook would suggest. However, I did not like the close on Friday, but we did not make a low below Friday’s low. Again, it was the first of the month and the day after the expiration of the April feeder futures and options that expired at $373.750.

Fed cattle cash trade developed unusually early this past week on Tuesday and surged to $256 after stubbornly trading below $250. These are new all-time highs in the fed cattle cash market as well as live cattle futures. More cash trade was reported on Wednesday morning at $256, but nothing the rest of the week. All of those purchases should have been processed this week and so, they should be back for more early next week. Expectations are high for continuation on to $260 and perhaps higher. Note the Live cattle chart did put in an outside reversal lower day in Friday's action. We will have to see if this is confirmed at the start of next week's trading.

With affordability top of mind for all consumers, especially with higher fuel prices, there could be more headwinds for the beef market ahead. However, there seems to be little that the politicians can do that will phase this market again. Reopening one of the border crossings with Mexico or changing tariffs or quotas with Brazil or Argentina may have a quick shock, but I think the market now knows that there is nothing that can be done to immediately add supply to the market.

China’s potential FMD issue could result in more beef imports, which only further tightens the supply situation. This by no means suggests that this market is resistant to weakness, but there is meaningful strength if the US consumer continues to spend. In fact, this is the case for the overall equity market as well. It is all interlinked. The rising tide lifts all boats, but that works two ways, of course. Let’s all pray for a soft landing in all respects.

The US House of Representatives passed the Farm Bill in years this past week that now goes to the Senate. More farm aid is being asked for and discussed as the commodity model of US agriculture faces rising input prices and tighter margins from recent years of lower commodity product prices. While such support may help bridge the issues, there are more fundamental challenges underlying the commodity model in US agriculture that will continue to persist as Brazil's lower cost model continues to capture global markets amid trade tensions and structure.

Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall.

If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. He can be reached at (580) 232-2272 or at brady@sidwellstrategies.com. Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at https://www.sidwellstrategies.com/fccp-disclaimer-21951.

/A%20close-up%20of%20a%20SpaceX%20sign%20by%20Sundry%20Photography%20via%20Adobe%20Stock.jpeg)

/AI%20(artificial%20intelligence)/AI%20chip%20by%203Dsss%20via%20Shutterstock.jpg)