/A%20concept%20image%20of%20space_%20Image%20by%20Canities%20via%20Shutterstock_.jpg)

Bloom Energy (BE) can no longer be considered a small fry in the fuel cell niche. With its record-breaking Q1 2026 results, it has become even more clear that Bloom Energy should be treated as a pure data center power play against AI data center shortages.

This is important. Today, data centers do not have enough electricity. AI infrastructure does not consist exclusively of GPUs, networking, and memory anymore. To get a reliable electricity supply, data center operators need to wait a lot of time until the grid improves. In this regard, Bloom Energy provides a unique opportunity to obtain electricity in a faster way via on-site fuel cells.

About Bloom Energy Stock

San Jose, California-based Bloom Energy is a clean energy technology company that develops solid oxide fuel-cell systems for on-site electricity generation. It offers its services to data centers, utilities, semiconductor manufacturing, and corporate customers. With a market capitalization of about $63.5 billion, Bloom Energy has become a large-cap stock.

It has been a remarkable ride. Shares of BE rose by 27.2% yesterday and are approaching their all-time highs of $290.50 per share. Year-to-date (YTD), shares of BE gained 223%, which means the stock has outperformed the S&P 500 Index ($SPX) dramatically.

At the same time, it is important to notice that the valuation is rich. Bloom Energy is trading at 32.5 times sales, 235.6 times forward earnings, and 82.9 times the book value. Under normal circumstances, this would mean that there is little room for upside for the stock, but now the market seems to be pricing Bloom more as an AI infrastructure play rather than an industrial power supplier.

Bloom Energy Reports Q1 2026 Beat

Recently, Bloom Energy announced better-than-expected quarterly results. Revenue was up 130.4% year-over-year (YoY) at $751.1 million, while adjusted earnings per share came in at $0.44, far exceeding the analyst consensus estimates of $0.12 per share. Product revenue surged 208.4% YoY to $653.3 million. Thus, we can conclude that the demand for Bloom's products is growing at a very high pace.

Moreover, margins are improving. Gross margin was reported at 30.0%, while non-GAAP gross margin stood at 31.5%. Operating cash flow is another interesting metric that should be mentioned—$73.6 million versus negative cash flows in the corresponding period a year ago. The key point here is that the growth is driven by operating leverage rather than simple top-line growth.

Management guided higher. In Q1 2026, Bloom Energy expects to report revenue of between $3.4 billion and $3.8 billion versus analyst expectations of $3.23 billion. Adjusted earnings per share guidance for the year stands at between $1.85 and $2.25 versus estimates near $1.40 per share. Non-GAAP gross margin is expected to come in near 34%, and non-GAAP operating income should hit between $600 million and $750 million.

All in all, this means that BE is emerging as a key data center power supplier at the exact time when power shortage issues emerge in AI data centers.

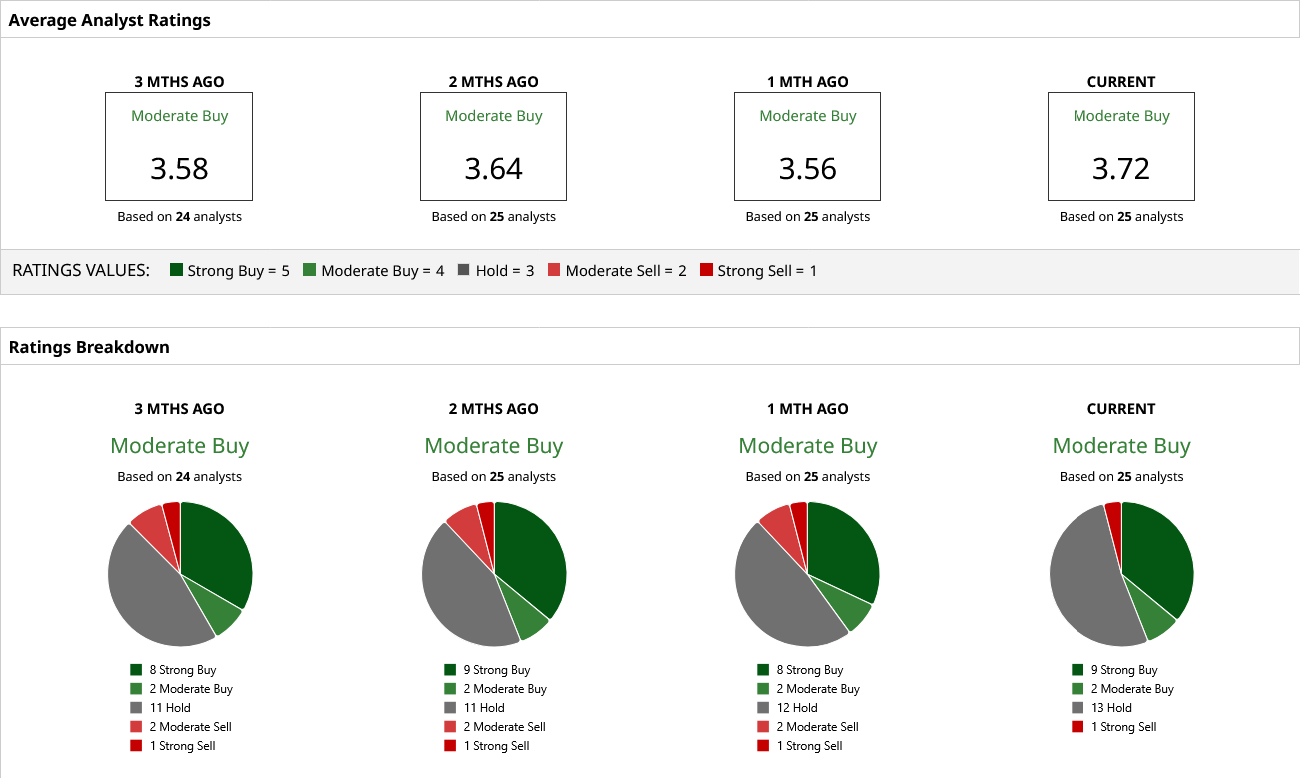

What Do Analysts Expect From BE Stock?

Unfortunately, analysts appear to be significantly less optimistic about BE stock, with a “Moderate Buy” rating consensus. Currently, analysts' consensus price target for BE stock stands at $175.54, implying downside potential of 39% from the recent price of $287.97. Even a relatively optimistic target price of $251 implies significant risk for the investors, while the bearish estimate of $55 could be disastrous.

On the date of publication, Yiannis Zourmpanos did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/AI%20(artificial%20intelligence)/An%20aerial%20view%20of%20a%20data%20center%20cooling%20system%20by%20Sepia100%20via%20Adobe%20Stock.jpeg)