/Oracle%20Corp_%20office%20logo-by%20Mesut%20Dogan%20via%20iStock.jpg)

There he is. He has done it again. As the AI infrastructure buildout gets stronger and stronger, one of the sector's most vociferous cheerleaders and popular Wedbush analyst, Dan Ives, has finally given his endorsement for Larry Ellison-led Oracle (ORCL). Initiating coverage on the cloud services provider with an “Overweight” rating and a price target of $225, which is about 35% higher than its current price, Ives and his team make a compelling case to invest in Oracle.

Why Is Ives Bullish on Oracle?

In a note to clients, Ives and his team of analysts reckon that Oracle's partnerships with key AI players like OpenAI and Nvidia (NVDA), its critical role in the much-vaunted Stargate project, and a secret sauce of "superior infrastructure and data integration" are ORCL stock's launchpad to greater heights in the future. Bringing things back to the present, though, with a market cap of about $500 billion, the ORCL stock is down 14% for the year.

However, that has not deterred Ives's faith in Oracle, as he remarked, "We believe Oracle is in the early innings of a significant repositioning as it executes on this generational opportunity. The vision is supported by partnerships with AI leaders like OpenAI and NVIDIA, and endeavors like the Stargate project. As Oracle continues to convert its backlog into revenue, we expect the market narrative to shift from focusing on capex risk to the durable, long-term growth story that is unfolding."

And this brings us to the next and more worrying part of the company, which is its huge debt pile of about $135 billion and its capex guidance of $50 billion in 2026. This, along with the company's negative free cash flow, has capped the upside of the ORCL stock in recent times and has made investors jittery. Yet, Ives is not convinced of it.

Addressing the issue, Ives said, "The downside case against Oracle centers on its capital expenditures and negative free cash flow. However, we argue this view is backward-looking and fails to appreciate the scale of contracted demand underpinning the investment. The most critical metric is the relationship between capex and Remaining Performance Obligations (RPO). Oracle’s RPO has swelled to $553 billion, driving its capex-to-RPO ratio to approximately 9.0%, compared to the group average of ~45.6%. This demonstrates that spending is not speculative but is deployed to service a massive backlog."

Notably, Ives and his team also sound gung-ho about Oracle's multicloud strategy, and with good reason. To this end, a particularly bright spot within Oracle's broader growth story is the arrangement it has established with Microsoft (MSFT), Google (GOOG) (GOOGL), and AWS, which allows customers to run Exadata directly inside Azure and AWS data centers rather than routing workloads through Oracle's own infrastructure. The traction this model has gained is difficult to overlook, with this segment of the business expanding 531% on a year-over-year (YoY) basis in the third quarter alone.

Management also added important context on the earnings call, noting that the operating margins associated with multicloud database deployments fall in the range of 60% to 80%, a meaningfully higher profit profile than what Oracle captures through its OCI infrastructure business. On the expansion front, the company closed out the third quarter with 33 live regions in partnership with Microsoft and 14 alongside Google, while its AWS footprint scaled at a particularly striking pace, going from just 2 regions to 22 between the third and fourth quarters.

And finally, in a virtuous loop, Oracle has moved to extend its reach into the same customer base that is fueling the infrastructure boom, rolling out a fresh set of agentic applications spanning finance, supply chain, and customer relationship management. The strategic intent is straightforward here. The companies investing heavily in AI infrastructure represent a natural and already engaged audience for high-margin software products, and Oracle is positioning itself to capture that revenue opportunity before others can establish a foothold.

Financials Look In Good Shape

Shifting focus to its numbers, Oracle has delivered inconsistent growth over the past decade, with revenue and earnings expanding at compound annual growth rates of 5.6% and 6.25%, respectively. Despite this history, analysts continue to forecast stronger-than-average expansion. They project forward revenue growth of 18.66% and earnings growth of 19.66%, both comfortably above sector medians of roughly 10.48% and 16.11%.

The company’s fiscal third-quarter results exceeded expectations and sparked a 9% increase in ORCL shares. Oracle posted beats on both the top and bottom lines.

Revenue climbed 22% YoY to $17.2 billion. Cloud services, now the largest contributor, surged 44% to $8.9 billion, reflecting accelerating demand tied to the firm’s AI infrastructure push.

Earnings per share rose 21% to $1.79, clearing the consensus forecast of $1.70 and extending the company’s streak of quarterly beats.

Remaining performance obligations, a key indicator of future demand, showed explosive expansion. The figure reached $553 billion, up 325% from the prior year. Management linked the sharp increase to several large-scale AI contracts.

Operating cash flow for the nine months ended Feb. 28 totaled $17.4 billion, compared with $14.7 billion in the same period last year. Oracle ended the quarter with $38.5 billion in cash, significantly exceeding its short-term debt of $9.9 billion. However, long-term debt stood at a sizable $124.7 billion.

Following a recent pullback in the share price, ORCL stock now trades at a more balanced valuation. The forward price-to-earnings ratio sits at 23.22 times, close to the sector median of 24.06 times. Meanwhile, the forward price-to-cash flow multiple of 18.58 times and the forward price-to-sales ratio of 7.41 times remain above their respective sector averages.

Analyst Opinion of ORCL Stock

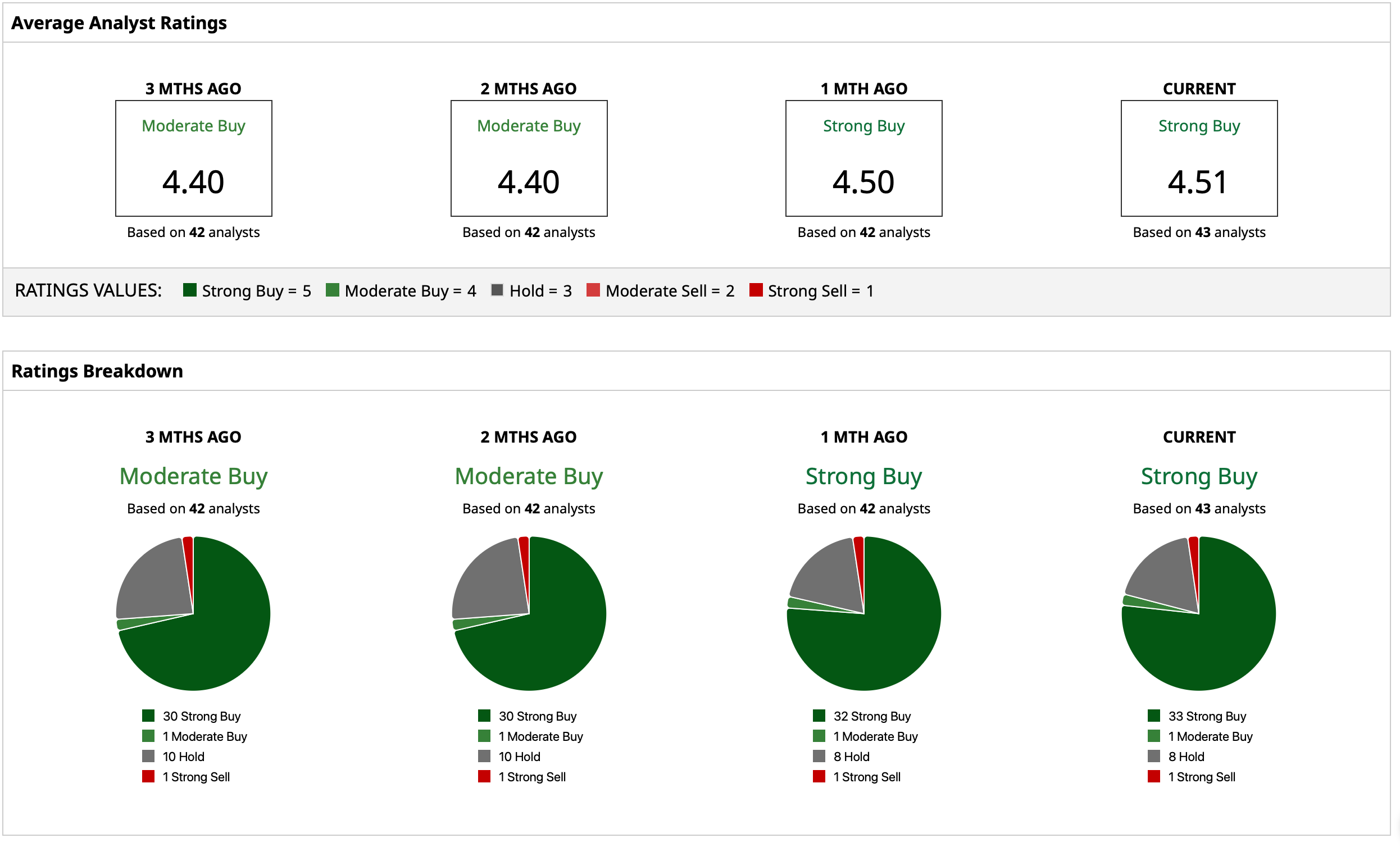

Thus, analysts have assigned ORCL stock a “Strong Buy” consensus rating, with a mean target price of $247.43. This indicates a potential upside of about 48% from current levels. Out of 43 analysts covering the stock, 33 have a “Strong Buy” rating, one has a “Moderate Buy,” eight analysts have a “Hold” rating, and one has a “Strong Sell.”

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20concept%20image%20showing%20a%20lightbulb%20with%20planet%20earth%20in%20a%20mossy%20green%20background%20by%20Capt_Pic%20via%20Shutterstock.jpg)

/The%20CrowdStrike%20logo%20on%20an%20office%20building%20by%20bluestork%20via%20Shutterstock.jpg)

/An%20image%20of%20a%20Tesla%20humanoid%20robot%20in%20front%20of%20the%20company%20logo%20Around%20the%20World%20Photos%20via%20Shutterstock.jpg)