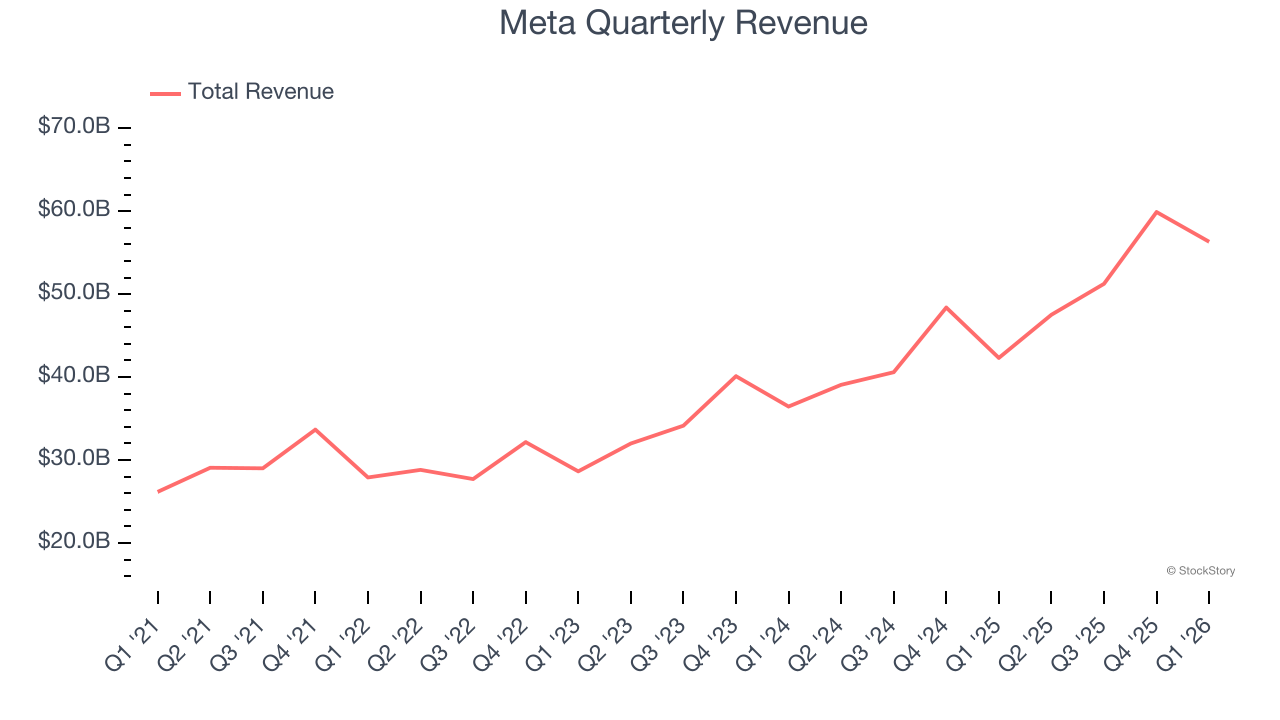

Social network operator Meta Platforms (NASDAQ:META) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 33.1% year on year to $56.31 billion. The company expects next quarter’s revenue to be around $59.5 billion, close to analysts’ estimates. Its GAAP profit of $10.44 per share was 56.8% above analysts’ consensus estimates.

Is now the time to buy Meta? Find out by accessing our full research report, it’s free.

Meta (META) Q1 CY2026 Highlights:

- Revenue: $56.31 billion vs analyst estimates of $55.55 billion (33.1% year-on-year growth, 1.4% beat)

- EPS (GAAP): $10.44 vs analyst estimates of $6.66 (56.8% beat)

- Revenue Guidance for Q2 CY2026 is $59.5 billion at the midpoint, roughly in line with what analysts were expecting

- Full year capex guidance raised to $135 billion, up from $125 billion previously

- Operating Margin: 40.6%, in line with the same quarter last year

- Free Cash Flow Margin: 22%, down from 23.5% in the previous quarter

- Daily Active People: 3.56 billion, up 130 million year on year (miss)

- Market Capitalization: $1.70 trillion

"We had a milestone quarter with strong momentum across our apps and the release of our first model from Meta Superintelligence Labs," said Mark Zuckerberg, Meta founder and CEO.

Company Overview

Famously founded by Mark Zuckerberg in his Harvard dorm, Meta Platforms (NASDAQ:META) operates a collection of the largest social networks in the world - Facebook, Instagram, WhatsApp, and Messenger, along with its metaverse focused Reality Labs.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, Meta’s 22.4% annualized revenue growth over the last three years was excellent. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Meta reported wonderful year-on-year revenue growth of 33.1%, and its $56.31 billion of revenue exceeded Wall Street’s estimates by 1.4%. Company management is currently guiding for a 25.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 21.2% over the next 12 months, similar to its three-year rate. We still think its growth trajectory is attractive given its scale and implies the market is baking in success for its products and services.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Daily Active People

User Growth

As a social network, Meta generates revenue growth by increasing its user base and charging advertisers more for the ads each user is shown.

Meta struggled with new customer acquisition over the last two years as its daily active people have declined by 2.9% annually to 3.56 billion in the latest quarter. This performance isn't ideal because internet usage is secular, meaning there are typically unaddressed market opportunities. If Meta wants to accelerate growth, it likely needs to enhance the appeal of its current offerings or innovate with new products.

Luckily, Meta added 130 million daily active people in Q1, leading to 3.8% year-on-year growth. The quarterly print was higher than its two-year result, suggesting its new initiatives are accelerating user growth.

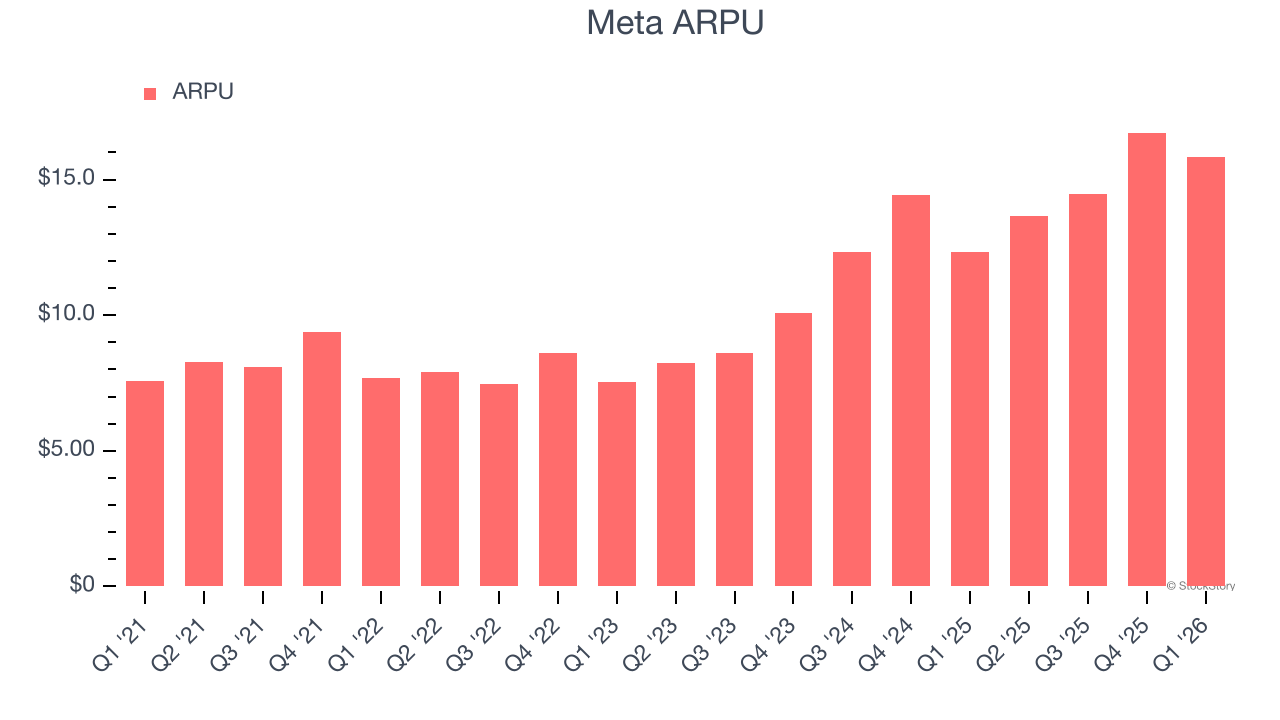

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns from the ads shown to its users. ARPU can also be a proxy for how valuable advertisers find Meta’s audience and its ad-targeting capabilities.

Meta’s ARPU growth has been exceptional over the last two years, averaging 29.6%. Although its daily active people shrank during this time, the company’s ability to successfully increase monetization demonstrates its platform’s value for existing users.

This quarter, Meta’s ARPU clocked in at $15.82. It grew by 28.2% year on year, faster than its daily active people.

Key Takeaways from Meta’s Q1 Results

It was good to see Meta beat expectations for revenue and EPS this quarter. On the other hand, Daily Active People missed and the company raised its full-year capex guidance, implying that cash generation will be lower. The market seemed to focus on the negatives and is reflecting skittishness around huge spending, and the stock traded down 7.1% to $625.87 immediately after reporting.

So do we think Meta is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

/Boston%20Scientific%20Corp_%20phone%20and%20website-by%20T_Schneider%20via%20Shutterstock.jpg)

/A%20photo%20of%20a%20Sandisk%20Solid%20State%20Drive%20by%20Top%20Popular%20Vector%20by%20Shutterstock.jpg)