Amazon’s (AMZN) business is quite complicated. The firm is more than just an online store. It makes money by selling its own products, taking fees from sellers who sell on its platform, providing advertising services, and offering cloud infrastructure. It's the last segment that is not only the most attractive part of the business but also a great growth driver. Amazon derives one-fifth of its revenue from Amazon Web Services (AWS), and that too at an outstanding 30% operating margin. With artificial intelligence as the main focus right now, this segment is gaining traction.

The race to build the strongest large language models (LLMs) has forced companies not just to invest heavily in new infrastructure but also to go to great lengths to gain an advantage over competitors. When it comes to AI, everything revolves around compute. Whoever has the cheapest compute can innovate faster, and that’s why having the best chips matters. For Amazon, this meant designing chips in-house for its AI workloads, and time is proving why that was a great move.

The company built the Trainium chips as alternatives to Nvidia’s (NVDA) GPUs to train its LLMs. As workloads move to CPU, the Graviton custom chip, based on ARM’s architecture, is coming to the fore. For inference, the company has already created and implemented its Inferentia chips, which is where all the margin improvement is coming from. This essentially makes Amazon a chip company, but one that implements chips in its own business rather than selling to others.

The nature of inference is such that it requires low latency at scale at an affordable price. When AI eventually moves to our devices, such as smartphones, smart glasses, or autonomous vehicles, it would need to operate on a real-time basis. Amazon’s own chips will help the company implement AI at scale without having to rely on third-party chips, thus increasing its margins. For this, Jeff Bezos and Andy Jassy had to turn the company into a chipmaker, and thanks to Taiwan Semi (TSM), they're doing exactly that.

About Amazon Stock

Amazon operates across e-commerce, digital content, advertising, and cloud computing. The company operates the AWS, North America, and international segments. Its online and offline stores offer both in-house and third-party products, while AWS runs one of the world’s largest data center networks.

AMZN stock had a poor first quarter, but things turned around pretty quickly as the semiconductor industry experienced a record rally, and Amazon went along for the ride, further proving the company’s worth as an important chipmaker.

The company is set to grow its EPS at 22.1% in 2027 and 27.3% in 2028. The forward P/E multiple of 34.11x might look pricey, but the company’s margins could entirely change if it can further optimize its Inferentia chips. It is all about getting to the cheapest compute, and Amazon is on the path to doing that with its in-house chip designs.

Amazon Beats Revenue Estimates

Amazon posted its fourth-quarter fiscal 2025 results on Feb. 5. AWS generated $35.6 billion in revenue for the quarter, with an increase of $2.6 billion from the previous quarter. Operating income came in at $12.5 billion. Across segments, North America reported revenue of $127.1 billion, and the International segment contributed $50.7 billion.

The company expects first-quarter net sales to range from $173.5 billion to $178.5 billion. This includes a favorable impact of about 180 basis points from foreign exchange. Operating income for the quarter is projected to be between $16.5 billion and $21.5 billion. CFO Brian Olsavsky expects North America costs to increase by around $1 billion year-over-year (YoY) due to Amazon Leo, the company's new satellite constellation. Amazon also plans to continue investing in International stores to improve customer experience.

What Are Analysts Saying About AMZN Stock?

Prior to the company’s earnings report, analyst sentiment toward AMZN stock had already turned positive. On April 24, Oppenheimer analyst Jason Helfstein raised the firm’s price target on the stock from $260 to $275 while maintaining an “Outperform” rating. He pointed to an improving outlook for AWS ahead of first quarter results. The firm sees potential for AWS growth to exceed its base forecast.

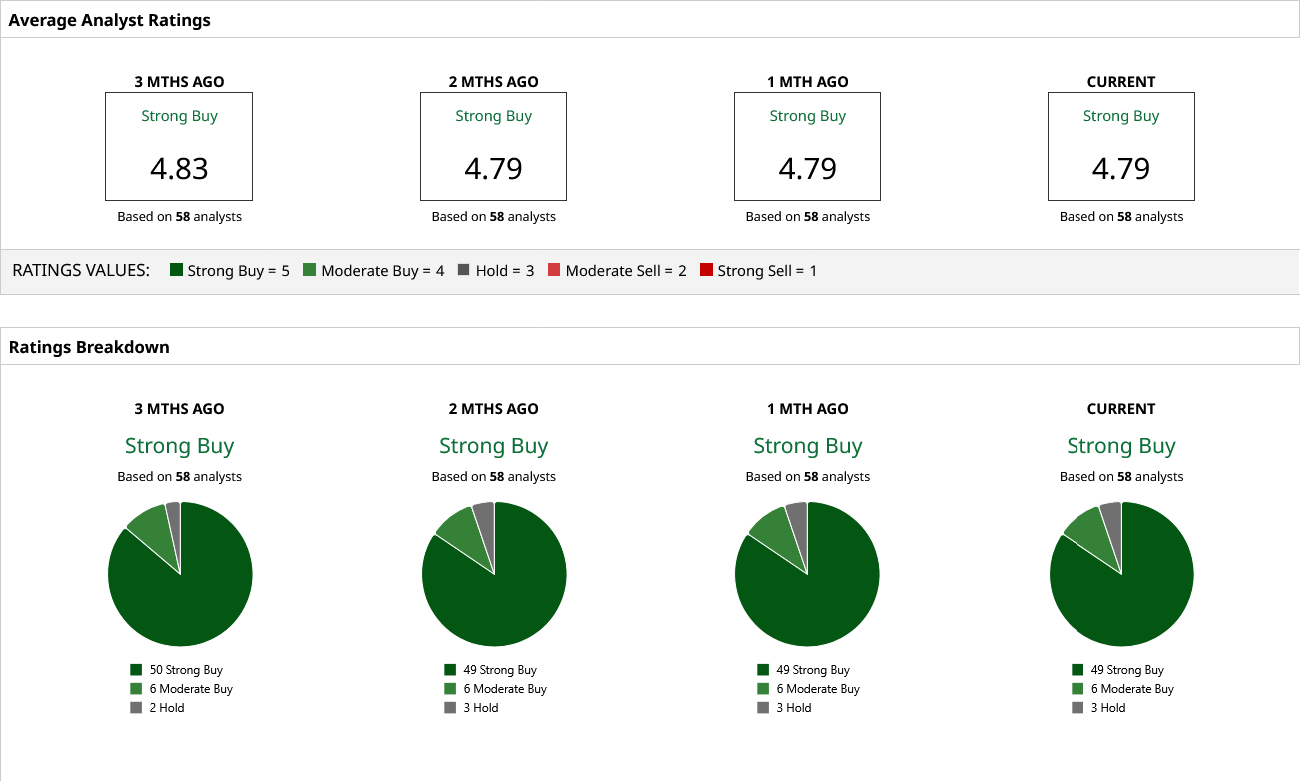

Amazon carries a consensus “Strong Buy” rating from 58 Wall Street analysts covering it. As per their estimates, the stock has a mean price target of $289.20, suggesting 9% upside from the current levels.

On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/Nvidia%20logo%20by%20Konstantin%20Savusia%20via%20Shutterstock.jpg)

/Apple%20products%20on%20desk%20by%20Ake%20Ngiamsanguan%20via%20iStock.jpg)