Comerica, Inc (CMA) a regional bank, now trades in value territory. That makes shorting its deep out-of-the-money put and call options a popular trade to generate income.

For example, the stock closed at $43.59 on March 17, which puts it at just 4.5x earnings for 2023. Analysts project earnings per share (EPS) will be $9.66 per share, compared to $8.47 last year. That implies the bank holding company will report 14% higher income this year. Given

Even if the bank reports 20% lower earnings at $7.73 per share, CMA stock is trading at 5.6x earnings. In fact, even if earnings are 50% lower at $4.83, the stock is still cheap at $7.5x earnings (i.e., $43.59/$4.83).

Meanwhile, as of March 7, 2023, the bank was telling analysts in an RBC presentation they expect 1% quarterly loan growth in Q1. That includes loan growth through to Feb. 28. In other words, the bank has not been marking down its $53.1 billion loan portfolio. That implies the bank could report higher earnings. Moreover, given the statements from the FDIC and Fed this week, there is good reason to believe that the bank's $69 billion in deposits are safe.

Needless to say, this is attracting a lot of value investors to the stock and especially its deep out-of-the-money (OTM) put and call options.

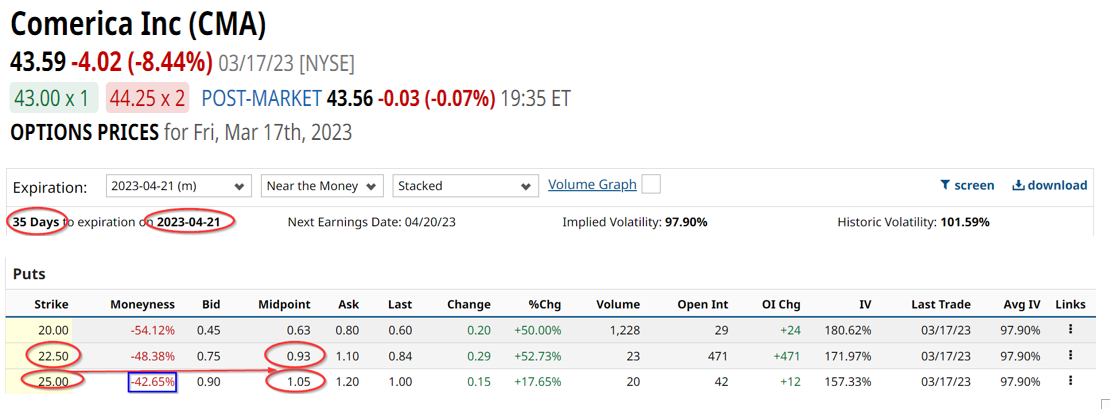

Shorting OTM Puts and Calls in CMA Stock

For example, the $25 strike price put option for the April 19 expiration date has a very high premium. This strike price is 42% below the spot price on March 17 of $43.59. So, in just 35 days, an investor who shorts the $25 strike price put can make $1.05 per put option.

That means the investor can immediately make 4.2% (i.e., $1.05/$25.00) by entering an order to “Sell to Open” a put contract at the $25.00 strike price. That is a very high premium and implies that if it could be repeated each month for a year, the annualized return would be 50.4%.

But, of course, that is not likely to be the case. In fact, to be even more conservative a trader will likely want to go long the $22.50 strike price by paying $0.93 to provide protection on the downside. That still leaves a net 12 cents earned assuming the stock does not fall below 42.65% and 48.38% from today's price on or before April 19.

Over time if it becomes clear that the bank is secure and deposits aren't fleeing, the investor could sell whatever price is left in the long put tranche of this trade. In other words, assuming there are still 20 cents left in the $22.50 long put portion, the investor could sell that in two weeks, etc., providing a net $0.32 credit for the trade. That still works out to a 1.28% yield on the original $25 short put trade.

An even more conservative approach would be to short out-of-the-money calls, either in conjunction with the short put trade or on a covered call basis. This involves more capital, but the put spread risk between $25.00 and $22.50 short-long put trade could be matched by the premium received in the covered call tranche.

For example, the $50 calls for April 19 are now trading for $2.58 at the midpoint. This provides an immediate 5.92% covered call yield (i.e., $2.58/$43.59 spot price). This also means that the $2.50 put spread risk is taken care of, with another 8 cents to spare.

And even if CMA stock rises to $50, the investor would make another 14.71% in capital gains, 5.92% covered call yield, and the 1.28% short put credit spread yield. That works out to a minimum total return of 21.91% and could be higher if the long put tranche is later sold as expiration nears.

The bottom line is regional bank stocks like this and the previous case of Western Alliance Bancorp (WAL), which I wrote about recently, are attracting value investors. They can take advantage of the very high option premiums that this stock presently is offering value-based investors.

More Stock Market News from Barchart

- Will the Turmoil in the Equity Markets Spillover Into the Commodity Markets?

- Stocks Continue Lower on Bank Turmoil

- Bank Turmoil Sparks Flight to Crypto

- Stocks Fall as Bank Concerns Linger

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.