/Electric%20vehicles%20by%20Wulandari%20Wulandari%20via%20Shutterstock.jpg)

Mobileye (MBLY) is not operating in an easy auto-tech environment right now. Electric-vehicle and autonomous-driving names are still being traded on future growth hopes, but concerns about consumer demand, heavy spending, and valuation pressure have kept the group volatile. Now, Mobileye has added a fresh catalyst.

On April 23, the company announced a board-approved plan to repurchase up to $250 million of its Class A shares. The move came alongside strong first-quarter results and a raised full-year outlook. That has left investors with a familiar question. Does the buyback make Mobileye more attractive, or is the stock still too expensive to chase?

Why This Buyback Matters for Mobileye

On one hand, the buyback is a clear signal of confidence from management. Mobileye is choosing to return capital to shareholders while still funding research and development, which suggests the business is generating enough cash to support both priorities.

On the other hand, this is not a transformational event. The company is not suddenly changing its long-term growth story. The repurchase may help offset dilution from stock-based compensation and the Mentee Robotics acquisition, but it does not eliminate the need for Mobileye to keep executing on revenue growth, product wins, and margins.

What Does the Valuation Say About MBLY Stock?

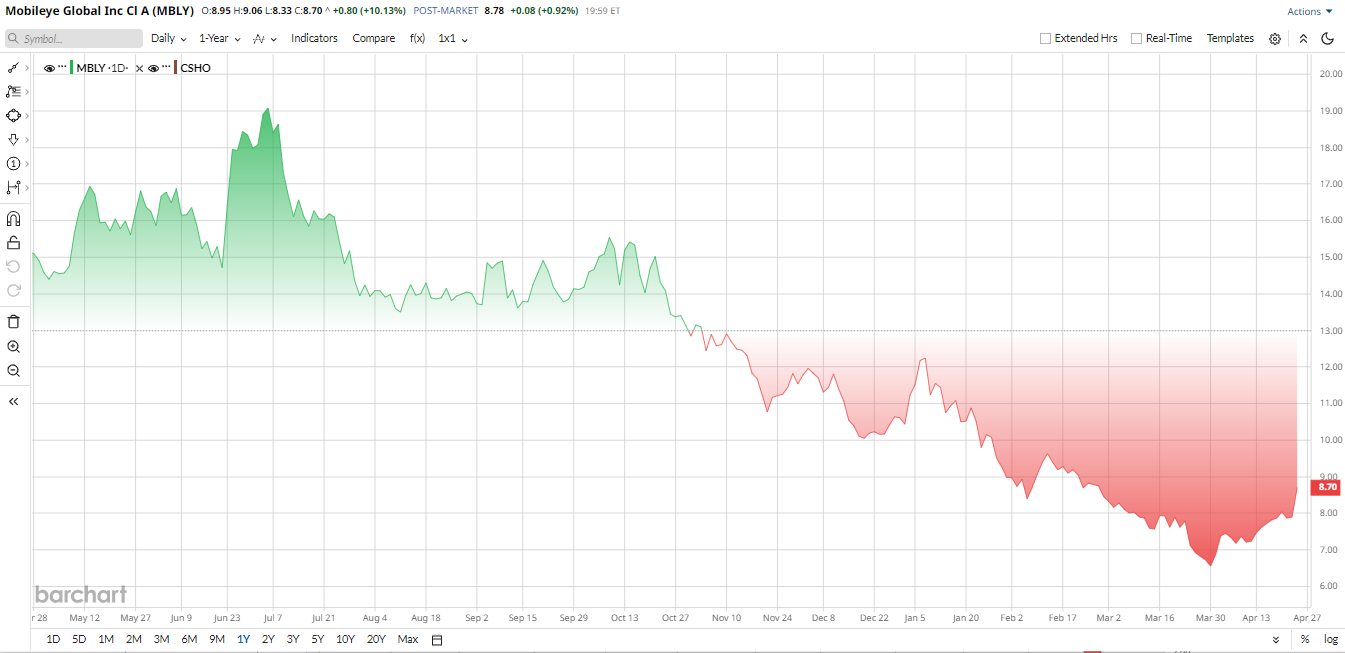

MBLY stock has already had a volatile year. After peaking near $19 in July 2025, the stock has fallen sharply and is now trading around the $8 to $9 range as of late April 2026. That leaves the shares down 12% year-to-date (YTD) and 36% over the past 52 weeks, despite the 10% jump on April 23 after earnings beat.

From a valuation standpoint, the stock still looks expensive relative to many peers. MBLY trades at about 3.5 times trailing sales and roughly 24.7 times forward EV/EBITDA, which is well above sector norms. It also trades at around 21 times forward earnings, suggesting the market is still pricing in meaningful growth.

That means investors are not paying for a mature auto supplier. They are paying for a long-duration technology story. If Mobileye continues to deliver, that can work. If growth slows or execution slips, the multiple could stay under pressure.

Mobileye’s Business Is Still Large, but Growth Is Uneven

Still, it is important not to overstate the risks. Mobileye remains a major player in driver-assist and autonomous-driving technology. Its EyeQ system-on-chip platform is used across a wide range of vehicles, and the company says more than 230 million cars will be fitted with EyeQ tech by 2025.

The first quarter showed that the core business is still growing. Revenue rose 27% year-over-year (YoY) to $558 million, helped by a 28% increase in EyeQ chip shipments. Mobileye also raised the midpoint of its full-year 2026 revenue forecast to about $1.975 billion, which suggests management sees continued momentum.

At the same time, the quarter was weighed down by a large non-cash goodwill impairment charge tied to its Intel-era balance sheet. That drove a reported net loss, even though the underlying business remained profitable on an adjusted basis.

In short, Mobileye is still a business with real scale, strong margins, and meaningful cash generation. But the growth story is no longer as simple as it once was.

Management Is Still Pushing the Long-Term Story

The more interesting part of the story is what Mobileye is building for the future. The company is investing heavily in its “physical AI” platform, which combines hardware and software for advanced driver-assistance systems and autonomous driving.

In the first quarter, Mobileye said it shipped about 20,000 SuperVision units, with more expected in the second quarter and full-year shipments projected at around 150,000. It also highlighted several Surround ADAS design wins, including contracts tied to Volkswagen Group (VWAGY), a U.S. OEM, and Mahindra (MHID.L.EB).

Mobileye has also been expanding beyond traditional driver-assist systems. Its acquisition of Mentee Robotics shows that management is looking at broader robotics and physical-AI opportunities, while the company continues to develop its robotaxi platform with partners such as Volkswagen.

That gives the stock a longer-term growth case, but it also means investors have to wait for those programs to scale.

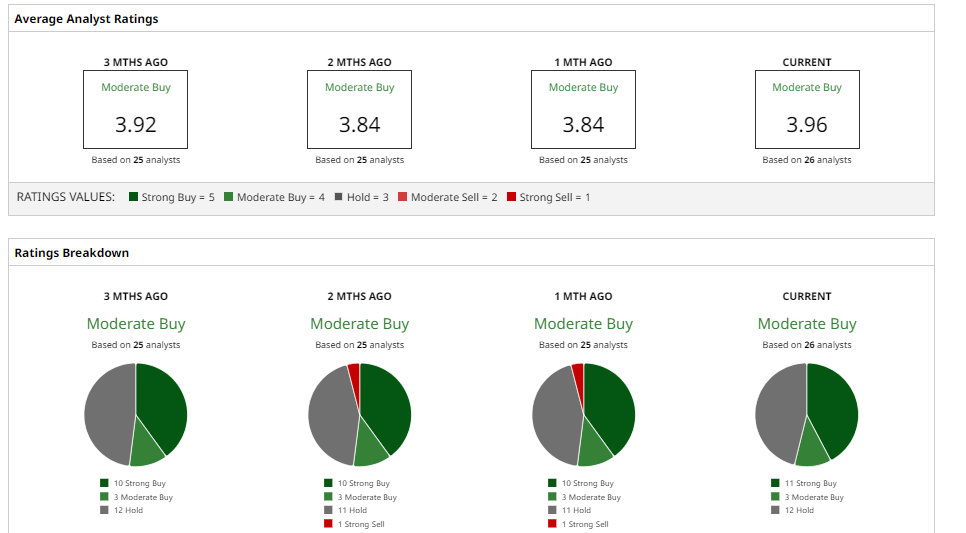

What Do Analysts Think of MBLY Stock?

Wall Street remains mixed on MBLY stock, though the tone is not outright bearish. Some analysts have recently trimmed targets, while others see room for upside if the company keeps executing.

Goldman Sachs recently raised its target to $9 and kept a “Neutral” rating, pointing to the ramp of higher-value products. RBC Capital also cut its target to $9, citing near-term pressure. Morgan Stanley remains cautious, while UBS and Mizuho are still on the sidelines with neutral-type views.

On the more bullish side, Barclays has turned more constructive, and Oppenheimer remains one of the strongest supporters of the stock with a much higher target.

In aggregate, the consensus view still looks like a “Moderate Buy,” with an average target that sits at $13.80, giving room for a 48% run above current levels. The high target of $27 would be 189% higher than current levels.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

/A%20Palantir%20office%20building%20in%20Tokyo_%20Image%20by%20Hiroshi-Mori-Stock%20via%20Shutterstock_.jpg)

/A%20hand%20holding%20a%20phone%20with%20the%20Reddit%20logo_%20Mamun_Sheikh%20via%20Shutterstock_.jpg)

/BlackRock's%20global%20headquarters%20By%20Tada%20Images.jpeg)

/The%20CoreWeave%20logo%20displayed%20on%20a%20smartphone%20screen_%20Image%20by%20Robert%20Way%20via%20Shutterstock_.jpg)

/Apple%20logo%20on%20store%20front%20by%20frantic00%20via%20iStock.jpg)